Complete GST lifecycle on one platform

Complete GST lifecycle on one platform

Hyper-automation

Hyper-automation

Smart reports & recon

Smart reports & recon

Accurate filing

Accurate filing

Index

Input Tax Credit (ITC) under GST

One of the fundamental features of GST is the seamless flow of input credit across the chain (from the manufacture of goods till it is consumed) and across the country.

Latest Updates

1st February 2022

Budget 2022 updates-

1. ITC cannot be claimed if it is restricted in GSTR-2B available under Section 38.

2. Time limit to claim ITC on invoices or debit notes of a financial year is revised to earlier of two dates. Firstly, 30th November of the following year or secondly, the date of filing annual returns.

3. Section 38 is completely revamped as ‘Communication of details of inward supplies and input tax credit’ in line with the Form GSTR-2B. It lays down the manner, time, conditions and restrictions for ITC claims and has removed the two-way communication process in GST return filing on the suspended return in Form GSTR-2. It also states that taxpayers will be provided information of eligible and ineligible ITC for claims.

4. Section 41 is also revamped to remove the references to provisional ITC claims and prescribes self-assessed ITC claims with conditions.

5. Sections 42, 43 and 43A on provisional ITC claim process, matching and reversal are eliminated.

29th December 2021

CGST Rule 36(4) is amended to remove 5% additional ITC over and above ITC appearing in GSTR-2B. From 1st January 2022, businesses can avail ITC only if it is reported by the supplier in GSTR-1/ IFF and it appears in their GSTR-2B.

21st December 2021

From 1st January 2022, ITC claims will be allowed only if it appears in GSTR-2B. So, the taxpayers can no longer claim 5% provisional ITC under the CGST Rule 36(4) and ensure every ITC value claimed was reflected in GSTR-2B.

What is input tax credit?

Input tax credit means at the time of paying tax on output, you can reduce the tax you have already paid on inputs and pay the balance amount.

Here’s how:

When you buy a product/service from a registered dealer you pay taxes on the purchase. On selling, you collect the tax. You adjust the taxes paid at the time of purchase with the amount of output tax (tax on sales) and balance liability of tax (tax on sales minus tax on purchase) has to be paid to the government. This mechanism is called utilization of input tax credit.

For example- you are a manufacturer:

- Tax payable on output (final product) is Rs 450

- Tax paid on input (purchases) is Rs 300

- You can claim input credit of Rs 300 and deposit only Rs 150 in taxes

Who can claim ITC?

ITC can be claimed by a person registered under GST only if he fulfils ALL the conditions as prescribed.

- The dealer should be in possession of tax invoice

- The said goods/services have been received

- Returns have been filed.

- The tax charged has been paid to the government by the supplier.

- When goods are received in installments ITC can be claimed only when the last lot is received.

- No ITC will be allowed if depreciation has been claimed on tax component of a capital good

A person registered under composition scheme in GST cannot claim ITC.

What can be claimed as ITC?

ITC can be claimed only for business purposes. ITC will not be available for goods or services exclusively used for:

- Personal us

- Exempt supplies

- Supplies for which ITC is specifically not available

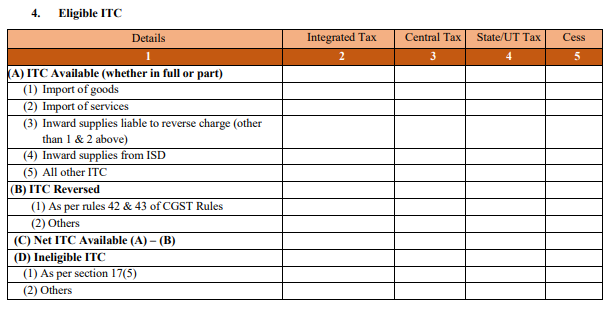

How to claim ITC?

All regular taxpayers must report the amount of input tax credit(ITC) in their monthly GST returns of Form GSTR-3B. The table 4 requires the summary figure of eligible ITC, ineligible ITC and ITC reversed during the tax period.

The format of the Table 4 is given below:

A taxpayer could have claimed any amount of provisional ITC until 9 October 2019. Later on, the government restricted the provisional ITC as below:

| Applicable date | % of provisional ITC |

| Upto 09.10.2019 | No limit |

| 09.10.2019 to 31.12.2019 | 20% |

| 01.01.2020 to 31.12.2020 | 10% |

| 01.01.2021 to 31.12.2021 | 5% |

| From 01.01.2022 onwards | Nil |

Accordingly, a taxpayer can claim ITC only if the same appears appears in their GSTR-2B. Hence, no provisional ITC can be claimed from 1st January 2022 onwards. Hence, matching of the purchase register with the GSTR-2B is crucial for ITC claims.

Reversal of Input Tax Credit

ITC can be availed only on goods and services for business purposes. If they are used for non-business (personal) purposes, or for making exempt supplies ITC cannot be claimed . Apart from these, there are certain other situations where ITC will be reversed.

ITC will be reversed in the following cases-

1) Non-payment of invoices in 180 days– ITC will be reversed for invoices which were not paid within 180 days of issue.

2) Credit note issued to ISD by seller– This is for ISD. If a credit note was issued by the seller to the HO then the ITC subsequently reduced will be reversed.

3) Inputs partly for business purpose and partly for exempted supplies or for personal use – This is for businesses which use inputs for both business and non-business (personal) purpose. ITC used in the portion of input goods/services used for the personal purpose must be reversed proportionately.

4) Capital goods partly for business and partly for exempted supplies or for personal use – This is similar to above except that it concerns capital goods.

5) ITC reversed is less than required- This is calculated after the annual return is furnished. If total ITC on inputs of exempted/non-business purpose is more than the ITC actually reversed during the year then the difference amount will be added to output liability. Interest will be applicable.

The details of reversal of ITC will be furnished in GSTR-3B. Read our article to understand more about the segregation of ITC into business and personal use and subsequent calculations.

ITC Reconciliation

ITC claimed by the person has to match with the details specified by his supplier in his GST return. In case of any mismatch, the supplier and recipient would be communicated regarding discrepancies after the filling of GSTR-3B. Learn how to go about reconciliation through our article on GSTR-2A Reconciliation. Please read our article on the detailed explanation of the reasons for mismatch of ITC and procedure to be followed to apply for re-claim of ITC.

Documents Required for Claiming ITC

The following documents are required for claiming ITC:

- Invoice issued by the supplier of goods/services

- The debit note issued by the supplier to the recipient (if any)

- Bill of entry

- An invoice issued under certain circumstances like the bill of supply issued instead of tax invoice if the amount is less than Rs 200 or in situations where the reverse charge is applicable as per GST law.

- An invoice or credit note issued by the Input Service Distributor(ISD) as per the invoice rules under GST.

- A bill of supply issued by the supplier of goods and services or both.

Special Cases of ITC

ITC for Capital Goods

ITC is available for capital goods under GST. However, ITC is not available for-

i. Capital Goods used exclusively for making exempted goods

ii. Capital Goods used exclusively for non-business (personal) purposes

Note: No ITC will be allowed if depreciation has been claimed on tax component of capital goods.

ITC on Job Work

A principal manufacturer may send goods for further processing to a job worker. For example, a shoe manufacturing company sends half-made shoes (upper part) to job workers who will fit the soles. In such a situation the principal manufacturer will be allowed to take credit of tax paid on the purchase of such goods sent on job work.

ITC will be allowed when goods are sent to job worker in both the cases:

- From principal’s place of business

- Directly from the place of supply of the supplier of such goods

However, to enjoy ITC, the goods sent must be received back by the principal within 1 year (3 years for capital goods).

ITC Provided by Input Service Distributor (ISD)

An input service distributor (ISD) can be the head office (mostly) or a branch office or registered office of the registered person under GST. ISD collects the input tax credit on all the purchases made and distribute it to all the recipients (branches) under different heads like CGST, SGST/UTGST, IGST or cess.

ITC on Transfer of Business

This applies in cases of amalgamations/mergers/transfer of business. The transferor will have available ITC which will be passed to the transferee at the time of transfer of business.

Quick Summary

GST allows for seamless flow of input credit, with recent updates tightening regulations around ITC claims. ITC allows for adjusting taxes paid on inputs against output tax. Conditions apply for claiming ITC, and it must be for business purposes. Reversal situations include non-payment of invoices and use for non-business purposes. Documentation, reconciliation, and special cases like ITC on capital goods, job work, ISD, and business transfers are detailed.

Was this summary helpful?

BROWSE BY TOPICS

Products

Individuals

ClearServices

Resources & Guides

GST Resources

ITR Resources

Mutual Fund Resources

Tools

TRENDING MUTUAL FUNDS

ICICI Prudential Technology Fund Direct Plan Growth

Tata Digital India Fund Direct Growth

Axis Bluechip Fund Growth

ICICI Prudential Technology Fund Growth

Aditya Birla Sun Life Tax Relief 96 Growth

Aditya Birla Sun Life Digital India Fund Direct Plan Growth

Quant Tax Plan Growth Option Direct Plan

SBI Technology Opportunities Fund Direct Growth

Axis Long Term Equity Fund Growth

TOP AMCS

STOCK MARKETS

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Cleartax is a product by Defmacro Software Pvt. Ltd.

Company PolicyTerms of use

ISO 27001

Data Center

SSL Certified Site

128-bit encryption