Filing for AY 2024-25 is coming soon

Filing for AY 2024-25 is coming soon

Filing for AY 2024-25 is coming soon

Keep calm and sign up for early access to our super filing

platform

Index

How to file ITR-1 (SAHAJ) Online? | ITR Filing FY 2023-24 (AY 2024-25)

Latest Update:

The CBDT has released ITR-1 and ITR-4 forms, for the Financial Year 2023-24. These forms will be applicable for filing income tax returns for the assessment year 2024-25 and its deadline is set for July 31, 2024, unless an extension is granted. In an effort to streamline the filing process and discourage delays, the Income Tax department has introduced these two ITR forms early. If you are wondering what has changed in ITR-1 and ITR-4, here's a summary of the changes done to ITR-1 and ITR-4:

- Applicability of ITR forms remains unchanged.

- Now, the New tax regime is the default tax regime; taxpayers will have to opt-out if they wish to choose the old regime

- A new column has been added to claim deductions under section 80CCH

- The ITR-4 form now includes a "Receipts in Cash" column for claiming an enhanced turnover limit

ITR-1, also known as Sahaj Form, is for a person with an income of up to Rs.50 lakh.

Who is eligible to file ITR-1 for FY 2023-24 (AY 2024-25)?

ITR-1 is a simplified one-page form for individuals receiving income of up to Rs 50 lakh from the following sources :

- Income from salary/pension (from one or multiple employers)

- Income from one house property (excluding cases where loss is brought forward from previous years)

- Income from other sources (excluding winning from the lottery and income from race horses)

- In the case of clubbed Income Tax Returns, where a spouse or a minor is included, this can be done only if their income is limited to the above specifications.

Aadhaar Card is mandatory for income tax return filing: The income tax department has made it mandatory for all taxpayers to link their Aadhaar card with their PAN on the income tax department website.

Who cannot file ITR-1 for AY 2023-24?

- An individual with an income above Rs 50 lakh.

- An individual who is either a director of a company or has held any unlisted equity shares at any time during the financial year.

- Residents not ordinarily resident (RNOR) and non-residents.

- Individuals who have earned income through the following means:

- More than one house property

- Lottery, racehorses, legal gambling, etc.

- Taxable capital gains (short-term and long-term)

- Agricultural income exceeding Rs 5,000

- Business and profession

- A resident that has assets (including financial interest in any entity) outside India or is a signing authority in any account located outside India

- Individuals claiming relief of foreign tax paid or double taxation relief under section 90/90A/91

- Deferred income tax on ESOP received from an eligible start-up

- Gains from Virtual Digital Assets (Crypto currency)

- Individuals for whom TDS is deducted under section 194N

Major changes made in the ITR-1 Form for AY 2024-25

- Individuals filing ITR 1 need to indicate their preferred tax regime in the return of income.

The New Tax Regime is the default tax regime from this year, as per the amendments introduced by the Finance Act 2023 in Section 115BAC. For individuals, HUFs, AOPs, BOIs, and AJPs, the new tax regime will apply by default. However, those who prefer the old tax regime, they must explicitly choose to opt-out of Section 115BAC(6) - For individuals with income (excluding income from a business or profession) need to specify their preferred tax regime in the income tax return filed for the relevant assessment year under Section 139(1)

For individuals with income from a business or profession, the option to opt out of the new tax regime and revert to the old tax regime is available. To exercise this choice, they must submit Form No. 10-IEA on or before the due date for filing the income tax return under Section 139(1). - An additional section, Section 80CCH, has been introduced by the Finance Act 2023. This section specifies that individuals who enroll in the Agnipath Scheme and subscribe to the Agniveer Corpus Fund on or after 01-11-2022 are entitled to a tax deduction for the entire amount deposited in the Agniveer Corpus Fund.

To accommodate this change, ITR forms 1 has been updated to incorporate a new column which allows taxpayers to provide the relevant details regarding the amount eligible for deduction under Section 80CCH.

What are the documents needed to file ITR?

Documents which you need to file the ITR-1 form are:

- Form 16: Issued by all your employers for the given financial year

- Form 26AS: Remember to verify that the TDS mentioned in Form 16 matches the TDS in Part A of your Form 26AS

- Receipts: If you have not been able to submit proof of certain exemptions or deductions (such as HRA allowance or Section 80C or 80D deductions) to your employer on time, keep these receipts handy to claim them on your income tax return directly.

- PAN card

- Bank investment certificates: Interest from bank account details – bank passbook or FD certificate

How to file ITR-1 (SAHAJ) Online on Income Tax Portal?

Step 1 - Visit the Income Tax e-filing portal

Step 2 - Register or Log in to your account

Step 4 - Select e-file > Income Tax Returns > File Income Tax Return

Step 5 - Select the Assessment Year as 2024-25 and the mode of filing as ‘Online’

Step 6 - Click on ‘Start New Filing’

Step 7 - Select the applicable status

Step 8 - Select ITR-1 as the form type

Step 9 - Click on ‘Let’s Get Started’

Step 10 - Select the appropriate reason and ‘continue’

Step 11 - Now you will have to fill up 5 sections here

- Personal Information - This section requires you to provide basic details such as your full name, PAN and Aadhar number, contact information, and bank account details.

- Gross Total Income -

- Total Deductions - The Income Tax Act 1961 allows for various deductions under different sections, which you should claim accordingly. Commonly known sections for deductions include 80C, 80D, 80TTA, 80TTB, and others.

- Tax Paid - This section displays your tax payments from all sources, including TDS, TCS, Advance Tax, and Self-Assessment Tax.

- Total Tax Liability - In this section, you will find the computed tax liability based on the information provided in the previous sections. To clarify, the tax payable on the Total Income is calculated as (Income - deductions claimed - Tax paid till date). If the resulting amount is negative, it can be claimed as a refund. If it is positive, it needs to be paid as tax.

Step 12 - Double-check to ensure the summary of tax computation is correct

Step 13 - Rectify the errors, if any and complete the validation

Step 14 - E-verify the ITR

How do I file my ITR-1 on Cleartax?

Step 1: Log in or sign up on the Cleartax portal.

Step 2: If you are filing with us for the first time, enter your PAN, Date of Birth, and the OTP received on your registered mobile number. Linking your PAN will help us file your return with the income tax department.

For us to pre-fill the details for you, you will have to complete another OTP verification. If you have filed with us before, you will directly see this step.

Once you enter the OTP and click on ‘Proceed’, you will see 95% of your information, like your name and income details, will all be pre-filled. You can review and edit these details if required.

Step 3: Now let’s fill up your income details. First up is your salary, your salary details will be pre-filled here, but you also have the option to upload your Form 16. And if you have switched jobs during the year, you may upload multiple Form 16s to file your ITR.

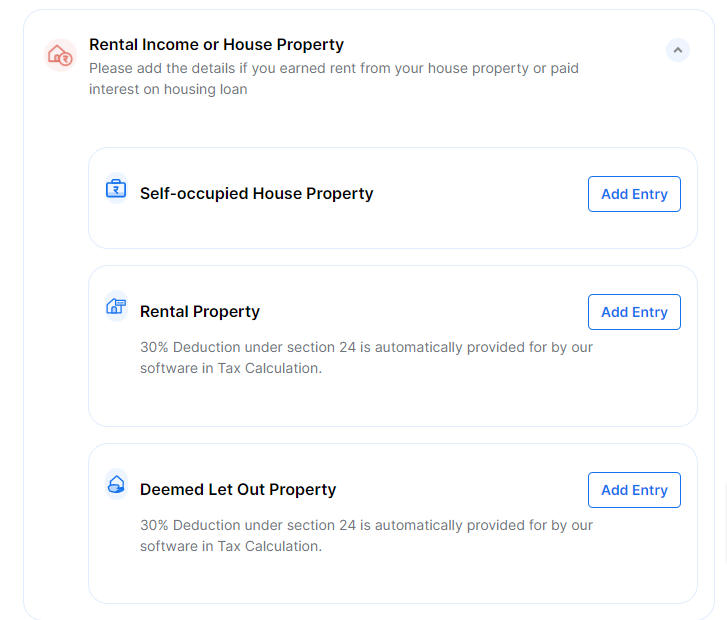

Step 4: Now, if you have a property, you’d need to fill in the details of the income you make from it. Depending on whether you occupy the house or have rented it out, you can enter all the details.

Step 5: Go to the other income section and enter the interest income you may have earned in your savings bank account or from your fixed deposit or any other source.

Step 6: Now comes the capital gains section! If you have invested in shares or mutual funds, select your stockbroker from the list and log in to your investment account. Your capital gains will be computed. You may skip this step if you do not have any investments.

Step 7: If you have any business/professional income, then add it in the next section.

Step 8: Now, it’s time to claim all the ‘Deductions’. If you have declared your investments to your employer, then most of your data would be pre-filled here. You can review these details and add the other deduction details that may be missing.

Step 9: If you scroll down, you will find the ‘tax-paid’ section. All the details of TDS and advance tax that you’ve paid will appear here. You can also add these details by uploading Form 26AS.

Step 10: Now scroll down, and you’ll see the other disclosures tab. If any of these conditions apply to you, then enter those details.

Step 11: Click on ‘Go to next’, and you will see a tax summary. Based on all the details you’ve added, we have auto-selected the ITR Form for you.

Also, the default tax regime for this year, according to the income tax department, is the New regime. However, the best part about filing your ITR with ClearTax is that it files your taxes under the regime that saves you maximum taxes by analysing your income and tax amount. You also have the option to compare your tax payable under both regimes and even switch to the other tax regime.

Once you are done reviewing all the details in the summary report, click on ‘File Tax’.

Step 12: Here, you will be asked to submit a self-declaration. Only once you submit this will your ITR be filed.

Step 13: Once this step is completed, you may add your coupon code and proceed to make the payment.

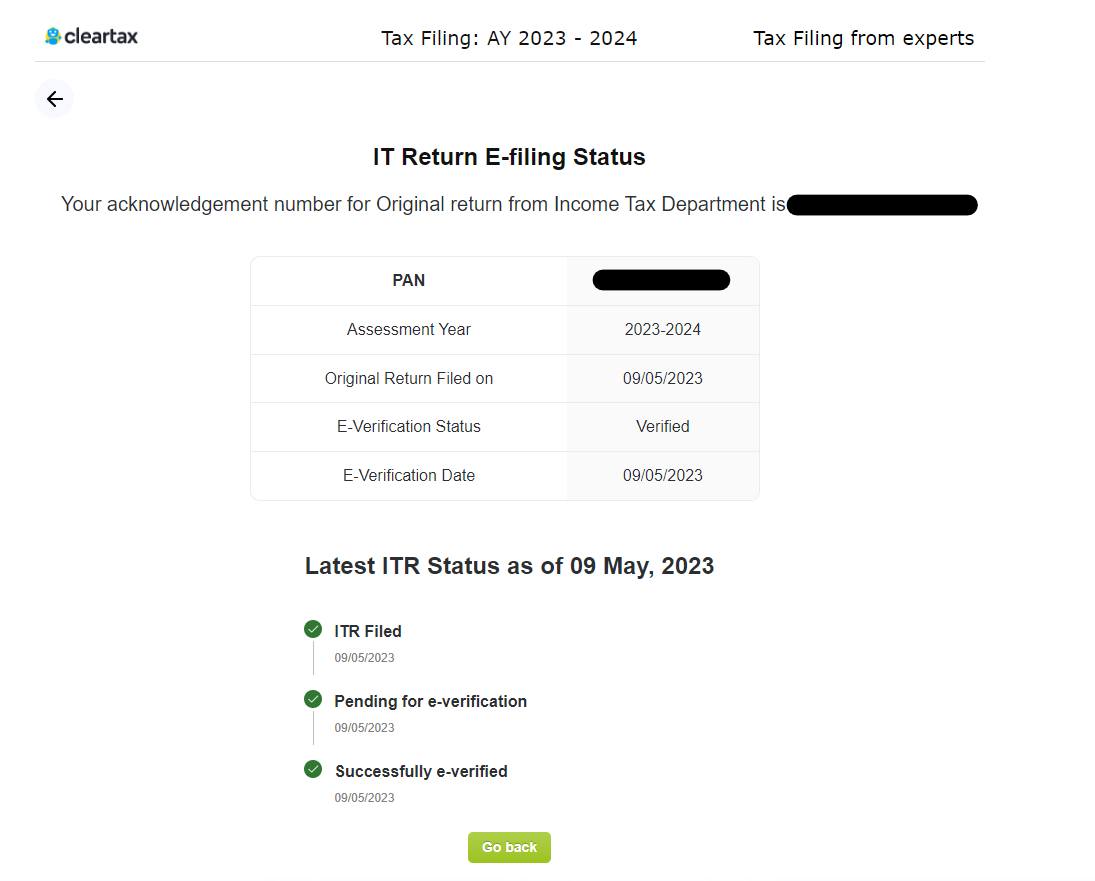

Step 14: After making the payment, your return will be submitted, and you will receive an acknowledgement number from the income tax department. Keep it handy for future reference. You will also receive an SMS and e-mail from the income tax department immediately.

Step 15: Now, THIS is the final step. Click on the ‘e-verify now’ button. e-Verifying your return is important for completing the ITR filing process. Else, the return will not be accepted by the income tax department.

Step 16: That’s it, and you are done with your ITR filing! But before you leave, don’t forget to collect these exciting rewards, cashback offers, and discounts. You have more than 20+ brands to choose from.

Step 17: You can log in to Cleartax and track the status of your ITR - you’ll be able to view whether your ITR has been processed, and if you are eligible for a tax refund, you will also be able to check the status of your refund.

Significant changes made in the ITR-1 Form for AY 2022-23 and AY 2023-24

Some changes have been incorporated into the ITR-1 form for AY 2022-23 and continue to be applicable for AY 2023-24 as well:

- Under the schedule ‘Salary’, you can disclose income from retirement benefit accounts maintained in the notified country under Section 89A, and claim relief for the same.

- Pensioners must now select the ‘Nature of employment’ (Central government, state government, public sector unit and others).

- You can now claim relief for the taxes paid on the income from the retirement benefit account maintained in a notified country at the time of withdrawal or redemption, as prescribed under Section 89A

Not sure which ITR form to use? Click here

What is the structure of the ITR-1 Form?

- Part A – General Information

- Part B – Gross total Income

- Part C – Deductions and taxable total income

- Part D – Computation of tax payable

- Part E – Other information (Bank account details)

- Schedule IT (Details of advance tax and self-assessment tax payments)

- Schedule-TDS (TDS/TCS details)

- Verification

Not sure which ITR form to use? Click here

Major changes in the ITR-1 Form for the AY 2021-22

The following changes have been incorporated into the ITR form:

- The taxpayer cannot file ITR-1 if TDS is deducted under section 194N. As per section 194N, tax shall be deducted at the source if non-filers of Income Tax Return withdraw cash exceeding Rs. 20 lakh. In other cases, tax shall be deducted when the cash withdrawals exceed Rs. 1 crore in a financial year.

- There is no option to carry forward TDS under section 194N. The credit of TDS under section 194N shall be allowed only during the year in which TDS was deducted.

- Individuals or HUFs are given the option to select an old or new tax regime. If the taxpayer selects a new tax regime under section 115BAC, he must file Form 10IE before filing ITR under section 139(1).

- The ITR forms for the assessment year 2020-21 had a new schedule DI. It allowed taxpayers to avail the deduction made during the extended period for the AY 2020-21. The schedule DI is removed from AY 2021-22.

Major changes in the ITR-1 Form for the AY 2020-21

- Individual taxpayers who meet the criteria of (a) making cash deposits above Rs. 1 crore with a bank or (b) incurring expenses above Rs. 2 lakh on foreign travel, or (c) expenditure above Rs. 1 lakh on electricity should also file ITR-1. The taxpayer should indicate the amount of the deposit or expenditure.

- Resident individuals who own a single property in joint ownership can also file ITR-1, where the total income is up to Rs. 50 lakh.

- Taxpayers should separately disclose the amount of the investment or deposits or payments towards tax-saving made from 1 April 2020 until 30 June 2020.

Major changes in the ITR-1 Form for the AY 2019-20

- ITR-1 Form for FY 2018-19 does not apply to an individual who is either a director of a company or has invested in unlisted equity shares.

- Under Part A, the ‘Pensioners’ checkbox has been introduced under the ‘Nature of employment’ section.

- Return filed under section 139(9) has been segregated between normal filing and filed in response to notices.

- Deductions under salary will be bifurcated into standard deduction, entertainment allowance, and professional tax.

- The taxpayers will be required to provide detailed income-wise information under the heading ‘Income from other sources’.

- A separate column is introduced under ‘Income from other sources’ for deduction u/s 57(iia) – in the case of family pension income.

- ‘Deemed to be let out property’ option is now available under ‘Income from house property’.

- Section 80TTB column is included for senior citizens.

Major changes in the ITR-1 for the AY 2018-19

- Earlier ITR-1 was applicable for residents, Residents Not Ordinarily Resident (RNOR), and also non-residents. Now, this form applies only to resident individuals.

- Under the TDS schedule, there is an additional field for furnishing details of TDS as per Form 26QC for TDS made on rent. Also a provision for quoting the PAN of the Tenant for such rent cases has also been provided.

- There is a requirement to furnish a break-up of salary. Until now, these details would appear only in Form 16, and the requirement to disclose them in the return had never arisen.

- There is also a requirement to furnish a break up of Income under house property which was earlier mandatory only for ITR-2 and other forms.

Major changes in the ITR-1 Form for the AY 2017-18:

- Quoting of Aadhar number is mandatory – If any person does not possess the Aadhaar number, but has applied for the Aadhaar card, they can quote the Enrolment ID of Aadhaar application form in the ITR.

- Disclosure of cash deposits during demonetisation – A new column has been introduced in all ITR Forms to report on cash deposited by taxpayers in their bank accounts during the demonetisation period, i.e., from November 9, 2016, to December 30, 2016. However, taxpayers are required to fill this column only if they have deposited Rs. 2 lakh or more during the period.

- Disclosure of all Bank Accounts – The details of all the savings and current accounts held at any time during the previous year must be provided. However, it is not mandatory to provide details of dormant accounts which are not operational for more than three years. The account number should be as per the Core Banking Solution (CBS) system of the bank.

- Simplified one-page ITR Form for Salaried class taxpayers (ITR-1 Sahaj) – Now, the Govt. has notified simplified one-page form ‘ITR-1 Sahaj’ for individuals having income up to Rs. 50 lakh from salary, pension, one house property, and income from other sources. It has removed columns which are not frequently used by the taxpayers, such as:

- New ‘ITR-1 Sahaj’ has retained those deductions which are most frequently used by the taxpayers under Section 80C, 80D, 80G and 80TTA. If any taxpayer wants to claim deductions under any other provision of chapter VI-A he can specify the relevant Section in the column titled ‘Any other’.

- Schedules of TDS and TCS have merged into one to make ITR-1 shorter and simpler.

- New columns have been inserted to report dividend income and long-term capital gains exempt under Section 10(34) and Section 10(38), respectively. It is mandatory to e-file tax returns for those with long-term capital of Rs. 2.5 lakh or more, even though their taxable income may be below Rs. 2.5 lakh.

How to file ITR on the government portal?

- Go to the Income Tax e-Filing portal, https://www.incometax.gov.in/iec/foportal/

- Log in to the e-filing portal by entering your user ID (PAN), Password, and Captcha code and click 'Login'.

- Click on the 'e-File' menu and click the 'Income Tax Return' link.

- Click on ‘Continue’.

- Read the instructions carefully and fill in all the applicable and mandatory fields of the online ITR form.

- Choose the appropriate Verification option in the 'Taxes Paid and Verification' tab.

- Choose any one of the following options to verify the income tax return:

- I would like to e-verify

- I would like to e-verify later within 120 days from the date of filing.

- I don't want to e-verify and would like to send a signed ITR-V through normal or speed post to "Centralised Processing Center, Income Tax Department, Bengaluru - 560 500" within 120 days from the date of filing.

- Click on the 'Preview and Submit' button, Verify all the data entered in the ITR.

- 'Submit' the ITR.

- On Choosing the 'I would like to e-Verify' option, e-Verification can be done through any of the following methods by entering the EVC/OTP when asked for.

- The EVC/OTP should be entered within 60 seconds else, the Income Tax Return (ITR) will be auto-submitted. The submitted ITR should be verified later by using the 'My Account > e-Verify Return' option or by sending a signed ITR-V to CPC.

Also read about:

1. Which ITR Should I File

2. How to file ITR Online

3. What is ITR 2 Form & How to File ITR-2

4. What is ITR 3 Form & How to File ITR-3

5. Who and How to File ITR 4

6. What is ITR-5 Form, Structure & How to File ITR 5

7. ITR 6

8. How to File and Download ITR-7 Form

9. ITR 3 vs ITR 4

10. ITR 1 vs ITR 4

11. How to File ITR-2 for Income from Capital Gains FY 2022-23

Frequently Asked Questions

Quick Summary

The CBDT released ITR-1 and ITR-4 forms for FY 2023-24. Changes include new default tax regime, Section 80CCH, 'Receipts in Cash' column in ITR-4. Mandatory to link Aadhaar with PAN. Filing eligibility criteria and steps are outlined for ITR-1. Document requirements and a step-by-step guide on how to file ITR-1 are provided. Major changes in ITR forms for previous assessment years are also highlighted.

Was this summary helpful?

BROWSE BY TOPICS

RELATED ARTICLES

Products

Individuals

ClearServices

Resources & Guides

GST Resources

ITR Resources

Mutual Fund Resources

Tools

TRENDING MUTUAL FUNDS

ICICI Prudential Technology Fund Direct Plan Growth

Tata Digital India Fund Direct Growth

Axis Bluechip Fund Growth

ICICI Prudential Technology Fund Growth

Aditya Birla Sun Life Tax Relief 96 Growth

Aditya Birla Sun Life Digital India Fund Direct Plan Growth

Quant Tax Plan Growth Option Direct Plan

SBI Technology Opportunities Fund Direct Growth

Axis Long Term Equity Fund Growth

TOP AMCS

STOCK MARKETS

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Cleartax is a product by Defmacro Software Pvt. Ltd.

Company PolicyTerms of use

ISO 27001

Data Center

SSL Certified Site

128-bit encryption