|

GSTR-5: For Non Resident Taxable Persons - Return Filing, Format, Eligibility & Rules

Updated on: Aug 22nd, 2025

|

3 min read

Non-Resident Taxable Persons (NRTPs) should obtain registration to do business in India. They can get registration from the GST portal for a temporary period of 90 days or less. Further, NRTPs must file the GSTR-5 return reporting on their business.

You have gone through the basic GST returns such as GSTR-1, GSTR-2B & GSTR-3B. This article explains all about GSTR-5 including what it is, why is it important, due date and format.

Latest Update

7th June 2025

GSTN via advisory implemented the restriction of not allowing the taxpayers to file their GSTR-3B after the expiry of a period of three years from the due date of furnishing the said return. The said change will be made effective on the GST portal from July 2025 tax period.

What is GSTR-5?

Every registered non-resident taxable person is required to furnish a return in GSTR-5 in GST Portal.

Who is a Non-Resident Foreign Taxpayer?

Non-Resident foreign taxpayers are those suppliers who do not have a business establishment in India and have come for a short period to make supplies in India. Such a person is required to furnish details of all taxable supplies in GSTR-5.

Why is GSTR-5 Important?

It will contain all business details for non-residents (NR) including the details of sales & purchases. Information from GSTR-5 will flow into GSTR-2A/2B of buyers.

GSTR 5 Due Date

GSTR-5 filing for a month is due on 13th of the following month.. For example, the GSTR-5 for July 2025 must be filed on or before 13th August 2025 to avoid late fees and penalties.

Here are the GSTR-5 due dates for FY 2025-26:

Month | GSTR-5 due date |

| March 2025 | 13th April 2025 |

| April 2025 | 13th May 2025 |

| May 2025 | 13th June 2025 |

| June 2025 | 13th July 2025 |

| July 2025 | 13th August 2025 |

| August 2025 | 13th September 2025 |

| September 2025 | 13th October 2025 |

| October 2025 | 13th November 2025 |

| November 2024 | 13th December 2025 |

| December 2025 | 13th January 2026 |

| January 2026 | 13th February 2026 |

| February 2026 | 13th March 2026 |

| March 2026 | 13th April 2026 |

If the non-resident is registered u/s 27

This is a special certificate of registration issued to a casual taxable person or a non-resident taxable person. The registration is of a temporary nature and is valid for the period specified in the application or 90 days from the effective date of registration, whichever is earlier. Such a person can make taxable supplies only after the issuance of the certificate of registration In such a case, the NR must file GSTR-5 within 7 days after the last day of the period of registration.

Let's look at an example:

Date of registration | Date of expiry of registration | Tax periods for which return(s) to be filed | Due date |

| 27th January 2024 | 23rd March 2024 | 27th January 2024 to 31st January 2024 | 13th February 2024 |

| 1st February 2024 to 29th February 2024 | 13th March 2024 | ||

| 1st March 2024 to 23rd March 2024 | 30th March 2024 |

What Happens if GSTR-5 is Not F?

If the GSTR-5 return is not filed then the next month’s return cannot be filed. Hence, late filing of GST returns will have a cascading effect leading to heavy fines and penalties.

What Happens if GSTR-5 is Filed Late?

If you delay in filing, you will be liable to pay interest and a late fee. Interest is 18% per annum. It has to be calculated by the taxpayer on the amount of outstanding tax to be paid. The time period will be from the next day of filing (21st of the month) to the date of payment. A late fee is Rs. 50 per day and Rs. 20 per day if a nil return. The maximum late fees is Rs. 5,000.

Details to be Provided in GSTR-5

There are 14 headings in the GSTR-5 format prescribed by the government. We have explained each heading along with the details required to be reported under GSTR-5.

- GSTIN

Provide your GSTIN. Provisional ID can also be used as GSTIN if you do not have

- Name of the Taxpayer

Name of the taxpayer including legal and trade name (will be auto-populated)

Validity period of registration – The validity period will also be auto-populated.

Month, Year –Mention the relevant month and year for which GSTR-5 is being filed.

- Inputs/Capital goods received from Overseas (Import of goods)

The NR must report inputs and capital goods imported into India.Details of the Bill of entry along with the rate of tax, IGST, cess paid and amount of ITC available. Note: A NR will only have to import inward supplies (purchases).

- Amendment in the details furnished in any earlier return

In this section, the NR can change any details in imports furnished in earlier returns. Changes can be made in-

- Bill of entry

- Rate of IGST

- Taxable value

- Amount of IGST & Cess

- Amount of ITC now available

- Differential amount of ITC (if excess will be reversed and vice versa)

Note: Both Original & Revised Details of Bill of Entry must be given

- Taxable outward supplies made to registered persons (including UIN holders)

This heading will contain invoice wise details of B2B sales in India including sales to UIN holders. Details of IGST/CGST & SGST & Cess along with State must be given.

- Taxable outward inter-State supplies to un-registered persons where invoice value is more than Rs 2.5 lakh

This heading will contain all details of B2C Large sales, i.e., inter-state sales (where invoice value is greater than Rs.2.5 lakhs) to unregistered persons.

- Taxable supplies (net of debit notes and credit notes) to unregistered persons other than the supplies mentioned at Table 6

This will contain details of sales to unregistered dealers (B2C Others). Both intra-state and inter-State sales less than 2.5 lakhs must be mentioned. Intra-state sales can be mentioned in a consolidated summary. Inter-state sales must be mentioned state-wise.

- Amendments to taxable outward supply details furnished in returns for earlier tax periods in Table 5 and 6 [including debit note/credit notes and amendments thereof]

This heading will contain any changes in details of B2B and B2C Large of previous months. Original debit notes and credit notes issued during the month will be furnished here. Amendments to invoices and debit & credit notes issued will also appear here. In case of revisions, original details have to mentioned.

- Amendments to taxable outward supplies to unregistered persons furnished in returns for Earlier tax periods in Table 7

This heading will contain changes in details of B2C sales of previous months (originally disclosed in Table 7). Intra-state sales can be mentioned in a consolidated summary. Interstate sales must be mentioned state-wise.

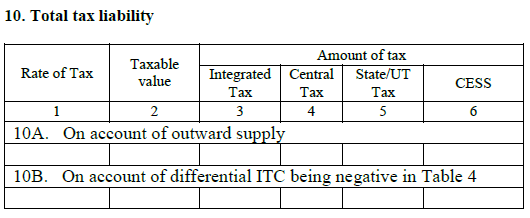

- Total Tax Liability

This heading will show the total tax liability.

- On account of outward supply:

This subheading will show details of tax liability for outward supplies for the current month. - On account of differential ITC being negative in Table 4:

This will contain the additional tax to be paid due to the reversal of ITC (i.e., differential ITC being negative) on making changes in any imports of earlier months (Table 4).

- Tax payable and paid

This heading will have the details of the tax you are actually paying during the month. The breakup of IGST, CGST, SGST & Cess will be shown. The taxpayer can opt to pay through cash or use ITC.

- Interest, late fee and any other amount payable and paid

This heading will contain details of interest and late fee due and actually paid on account of late filing of the return.

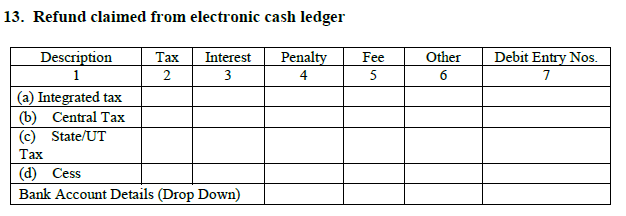

- Refund claimed from electronic cash ledger

This heading will contain the details of all refunds received in the electronic cash ledger. There is a dropdown to select in which bank account the NR wants to receive the refund.

- Debit entries in electronic cash/credit ledger for tax/interest payment [to be populated after payment of tax and submissions of return]

This will show the debit entries in the electronic cash ledger, i.e., cash outflow for payment of tax/interest/late fee. It is populated after payment of tax and submission of return.

Finally, the return is verified by the authorized signatory. The authorized signatory is a representative of the NR and must be a person resident in India with a valid PAN.

To know more about the different types of returns, deadlines and the frequency of filing, read our article on GST Returns.

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption