|

What is e-Invoicing Under GST? Applicability, Limit, Rules & Process

Switch Language

E invoicing refers to Electronic Invoicing. It is the process of reporting your B2B transactions to the GST authority through the Invoice Registration Portal (IRP) and obtaining a unique Invoice Reference Number (IRN) to finally issue to customers.

Key Takeaways

- E-Invoice is mandatorily applicable for businesses with an annual turnover above Rs. 5 crores, effective from August 1, 2023

- E invoice is required that businesses with an annual turnover of over 10 crores must report their B2B invoices to the IRP within 30 days from the date of invoice generation.

- Validation of E-invoice: An invoice issued by a notified taxpayer without generating a valid IRN from IRP is treated as an invalid tax invoice under Rule 48(4), liable for penalties and leaves recipients without ITC.

- Implementing e invoicing can be challenging due to ERP integration issues, strict reporting and cancellation timelines, and frequent data validation errors.

What is e-Invoicing under GST?

E invoicing is the process of reporting B2B invoices to the IRP for the generation of an IRN. It does not mean the government generates invoices; rather, it verifies and authenticates them to prevent duplication, tax evasion, and fake ITC claims.

E-invoicing Applicability

Any registered person whose aggregate turnover exceeds Rs.5 crore or more has been notified as a person who shall prepare e-invoice in respect of Business-to-Business (B2B) supplies and for exports.

If the turnover in the last financial year was below the threshold limit, but it increased beyond the threshold limit in the current year, then e-Invoicing would apply from the beginning of the next financial year.

Watch the video below to understand about e-invoicing implementation for your enterprise-

Exclusions from E-Invoicing

Below is a list of exclusions from the scope of e invoicing in India:

Notified Businesses | Documents | Transactions |

1)An insurer, a banking company or a financial institution, including an NBFC 2) A Goods Transport Agency (GTA) 3) A registered person supplying passenger transportation services 4) A registered person supplying services by way of admission to the exhibition of cinematographic films in multiplex services 5) An SEZ unit (excluded via CBIC Notification No. 61/2020 – Central Tax) 6) A government department and Local authority (excluded via CBIC Notification No. 23/2021 – Central Tax) 7) Persons registered in terms of Rule 14 of CGST Rules (OIDAR) | Delivery challans, Bill of supply, financial or commercial credit note or debit note, bill of entry, and ISD invoices. | Any Business-to-Consumers (B2C) sales, Nil-rated or non-taxable or exempt B2B sale of goods or services, nil-rated or non-taxable or exempt B2G sale of goods or services, imports, high sea sales and bonded warehouse sales, Free Trade & Warehousing Zones (FTWZ), and supplies under reverse charge covered by Section 9(4) of the CGST Act. |

Documents and Invoices under E-Invoicing

The following documents are presently covered under E-Invoicing:

- Tax Invoices

- Debit Notes

- Credit Notes

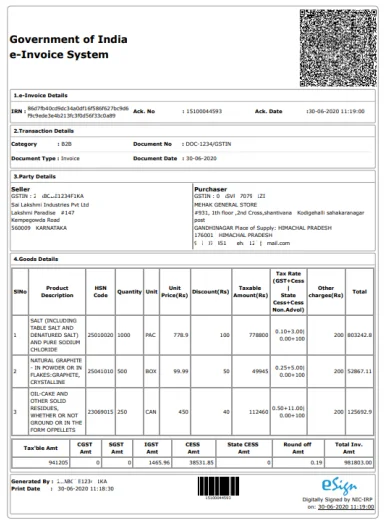

Components of an E-invoice

- Invoice Reference Number (IRN) – A 64-character unique hash string generated by IRP for every B2B invoice reported, to authenticate the invoice and prevent duplication.

It is different from the invoice number. GST invoice will be only valid with a valid IRN.

- QR (Quick Response) Code – IRN is embedded with a QR code containing the supplier and recipient GSTIN, invoice number, date, invoice value, HSN, and IRN details for offline verification. QR code consists of the following parameters:

- GSTIN of the supplier and the recipient

- Invoice Number

- Date of generation of invoice

- Invoice Value include taxable value and tax

- No. of line items, HSN of the items

- IRN and date of IRN generation

- Digital Signature – An e-invoice is authenticated by the digital signature in IRP, authenticating the sender’s details, verifying that the contents of the invoice remain unchanged from the moment it was signed, etc.

- JSON Format – Invoice details to be in prescribed schema (GST INV – 01) have to be reported in IRP in JSON (Java Script Object Notation), which is to be uploaded to generate IRN.

E-Invoice Mandatory Fields

50 fields in e-invoice are mandatory. To ensure proper tax validation and invoice authentication, the following mandatory fields have to be reported in IRP to generate IRN:

- Supplier details – GSTIN, legal name and address, etc

- Invoice details – Invoice number, Invoice date, type, invoice value, taxable value, etc.

- Buyer Details- GSTIN, legal name and address, etc

- Item Details – Number of items, HSN, quantity, unit value, etc.

- Place of Supply – State code.

- IRN with signed QR code

Format of Sample E-invoice

How Does the GST e-Invoice System Work?

- Generation of Invoice by Accounting/ERP system: The invoices must be prepared by the taxpayers in a standardised format as prescribed in e-invoice schema in Form GST-INV 1.

- Upload the invoices to IRP: Invoice data is uploaded in the prescribed JSON schema (GST INV-01) to the IRP.

- Validation by IRP: IRP generates an IRN, which is a unique 64-character hash number based on supplier GSTIN, invoice number, financial year, document type, etc. IRN is generated after validation of the invoices.

- QR Code and Digital Sign: After IRN is generated, IRP digitally signs the invoice and a QR code is generated, which is used to authenticate the invoice.

- Data Flow to GST and E-way Bill Portal: The valid invoices automatically get reflected in the draft GSTR-1, and Part A of the e way bill is also automatically fetched. This reduces manual errors and reconciliation issues.

E-Invoice Time Limit

As per the 5th November 2024 advisory issued by GSTN (Goods and Services Tax Network), effective from April 1, 2025, it was mandated that e-invoices have to be reported in the IRP by the taxpayer within 30 days from the date of generating the invoice.

Compliance Requirements under e-Invoicing

Rule 48(4) stipulates that the e-invoice shall be prepared by the notified class of registered persons, by uploading the particulars as required by Form GST-INV 01 on the IRP and obtain IRN.

Penalties for Non-Compliance

Rule 48 attracts severe penalties under section 122 of the CGST Act, 2017:

Non-compliance may attract penalties up to ₹10,000 or 100% of tax (WIH), ₹25,000 per incorrect invoice, and detention of goods. An invoice without a valid IRN is invalid for ITC claims.

Benefits of e-Invoicing to Businesses

- E-invoicing helps in auto-reporting of invoices into the GST return and auto-generation of E-way bill (wherever required);automatic fetching of data into the portal without requiring manual efforts.

- This will reduce the transcription errors as the same data is reported to the tax department as well as to the buyer to prepare his inward supplies (purchase).

- A complete trail of B2B invoices is being kept with the GST department, enabling system-level matching of ITC and output tax, thereby reducing tax evasion.

- Through the system of e-invoices, businesses can track their invoices in real-time, allowing for better monitoring and control.

Challenges in Implementing e-Invoicing

There are quite a few challenges a business faces, including several operational and compliance challenges:

- Accounting System/ERP Integration issues – The usual accounting software is not compatible with the e-invoicing schema. Especially, small and mid-size businesses face the issue of JSON validation errors, failure to integrate API, HSN mismatches and incorrect tax mapping, etc.

- Time Limit – Businesses are required to report the invoices in the IRP within 30 days from the date of generating the invoice. A taxpayer cannot create a backend IRN that means an invoice cannot be validated after issuing the invoice.

- Data Accuracy and Validation Errors – Even small clerical mismatches like wrong GSTIN of the recipient, duplicate invoice number, place of supply errors, etc., can lead to IRN rejections.

- Invoice Cancellation Limitation – An e-invoice can be cancelled only within 24 hours on the IRP; no partial cancellation of an invoice is allowed, thus creating difficulties in price revisions, goods rejections, etc.

- Operational Dependency on Internet and GST Portal – Businesses dealing in high volume invoices face quite the challenges during peak filing seasons due to multiple issues like IRP downtime, API slowness and connectivity issues in remote branches.

How can e-Invoicing Curb Tax Evasion?

E-invoicing will eliminate fake invoices. Claiming fictitious ITC by raising fake invoices is also one of the biggest challenges currently faced by tax authorities. The e-invoice system will help to curb the actions of unscrupulous taxpayers and reduce the number of fraud cases, as the tax authorities will have access to data in real-time.

How does Clear e-Invoicing Help?

Team Clear provides the best-in-class e-invoicing solution for businesses.

Clear is officially a GSTN-approved IRP. More than 3,000 large enterprises trust the Clear e-Invoicing solution for a unified e-invoicing and e-way bill compliance journey. We provide the best-in-class e-invoicing solution for businesses of any scale and industry. Do not miss exploring the Clear e-Invoicing solution! Team Clear ensures a safe migration to an upgraded UI with no changes to your historical data.

Team Clear also offers various modes through which e-invoices can be generated by the taxpayers, such as seamless API integrations, Excel mode, FTP, SFTP or Tally connector. The user can enjoy numerous value additions such as-

- Seamless generation of 5,000 e-invoices per minute

- Integration with a high-fidelity solution with 99.99% uptime

- 100+ data validations to ensure an error-free smooth e-invoicing experience

- Auto-retry of failed EWBs (with distance error) to improve the success rate of EWB generation

- Automatic generation of the e-way bill after IRN generation without any ingestion of data

- Faster loading of ‘e-invoices’ and ‘e-way bills’ on the screen for as many as 1 lakh documents

- Reconciliation vis-a-vis e-way bill and GSTR-1 data, insightful reports, customised print template for e-invoice, data archiving, etc.

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption