IND AS 19 - Employee Benefits

The Indian Accounting Standard (Ind AS) 19 aims to prescribe accounting and disclosure for employee benefits. It requires recognition of the liability by an entity when an employee provides services for employee benefits to be paid in the future, and recognition of expenses when the entity utilises the economic benefit arising from service given by an employee in exchange for employee benefits.

What are employee benefits and what is its accounting treatment under IND AS 19?

Employee benefits refer to all forms of compensation (cash/non-cash) paid by an employer to employee apart from salary/wages for the service provided to the employer. Offering employee benefits are essential to attract and retain the talent for the company. IND AS 19 prescribes the accounting treatment and disclosure w.r.t. employee benefits. Employee benefits provided by the employer during an accounting period has to be recognized as either:

- Liability – when will the employee benefits be paid – in the future (or)

- Expense – when the employer consumes the benefit arising from the employee’s service

What are the different employee benefits under AS 19?

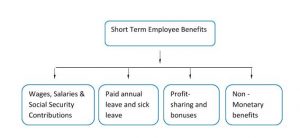

- Short-term employee benefits – There are those which are expected to be fully paid before 12 months after the end of the accounting period in which the employee rendered service.

- Other long-term employee benefits – There are those which are not expected to be fully paid within 12 months after the end of the accounting period.

- Termination benefits -These are those which are paid to an employee who is terminated from service due to the employer’s decision.

- Post Employment benefits – These are those employee benefits which are paid after the completion of employment.

Everything about short-term benefits

Short-term employee benefit includes the following:

Recognition & Measurement

Once the employee renders service to an employer, the expected amount of short-term employee benefits to be paid for such service has to be recognized as a liability or as an expense. It is considered a revenue expenditure generally except when any other standard requires it to be capitalized.

Types of short-term benefits

Short-term employee benefits are of two types:

- Paid absences and

- Profit sharing and bonus plan

Paid Absences

These are compensated absences and can be classified as accumulating paid absences and non-accumulating paid absences. Examples of such absences are holidays, sickness, maternity, etc and their related cost are recognized as follows:

| Description | Cost Recognition |

| Accumulating paid absence | When services rendered increases the employees right to future paid absence |

| Non-accumulating paid absences | When such absences occur |

Profit-Sharing and Bonus Plan

‘Profit sharing’ and ‘Bonus Plan’ are benefits such as employee’s annual incentive, managing director’s commission etc. These costs are recognized when the employer:

- Has a present obligation to make such payment on account of past events; and

- Has the reliable estimate of expected payment that can be made.

All about Post Employment Benefits

Post-employment benefits include the following:

- Retirement benefits (pension)

- Other post-employment benefits (life insurance, medical care)

These benefits can be classified as either defined contribution plan or defined benefit plan depending upon the nature of the plan.

Defined Contribution Plans

Under this plan, employer’s liability to pay the entire employee’s right is limited to the amount the entity agrees to contribute and there is no legal or constructive obligation on the entity to pay beyond such funds. Consequently, the actuarial and investment risk fall, in substance on the employee. Examples are the provident fund, superannuation fund etc Note: Actuarial risk is that if benefits will be less than expected (cost is more); Investment risk is that if assets invested will be insufficient to meet expected benefits.

Defined Benefit Plans

Employer’s obligation is to provide the agreed benefits to current and former employees and the actuarial and investment risk fall, in substance is on the employer. Examples are pension, gratuity, post-employment medical benefit, etc. Contribution and benefit plans can be varied like State plans, Multi-Employer plans or Insured plans and they require separate disclosures in the financial statement.

Recognition of defined benefit cost

| Component | Recognition |

| Recognizing current and past periods service cost | P&L |

| Recognize the net interest on the net defined benefit liability or asset arrived using discount rate (beginning of an accounting period) | P&L |

| Remeasurement of defined benefit liability or asset consisting of:Actuarial gains/lossesReturn on plan assetsChanges in the asset ceiling effect | Other comprehensive income (should not be reclassified to P&L in subsequent period) |

Accounting treatment for defined benefit plan by an employer

- Make reliable estimate of the employee benefit amount using actuarial techniques

- Discount such benefit using PUCM* to determine the present value of the benefit obligation and also the current service cost

- Determine the fair value of any plan assets

- Determine the total actuarial gain/losses** to be recognized in other comprehensive income

- On introduction or change of a plan, determine the past service cost***

- On curtailment or settlement of a plan, determine the resulting gain/loss

*Under PUCM, each period of employee service gives rise to an additional unit of benefit and such units are measured separately and added to the final obligation. It is applying the present value concept and recognizing a future value as on the balance sheet date **Actuarial gain/losses can result in an increase or decrease in either present value of a defined benefit obligation or the fair value of plan assets. ***Past service cost is the change in the present value of defined benefit obligations caused by employee service in prior periods.

Actuarial Valuation and Assumptions

Actuarial valuation for employee benefits aims to calculate the present value of benefit payment that will be paid to an employee in future as part of a benefit plan. Calculation of defined benefit obligation is the first step in this valuation. For the above valuation, actuaries will make assumptions to determine how likely an employee is to resign or die prior to the retirement age, how the employee salaries are expected to increase, etc.

In order to arrive at these, actuaries use probabilities for various events which are termed as actuaries assumptions. Actuarial assumptions should be unbiased and mutually compatible and cover both financial & demographic assumptions. Financial assumptions should be based on market expectations and also include:

| Financial Assumptions | Demographic Assumptions |

| Discount rate* | Probable mortality rate |

| Employee salary escalation | Employee Attrition rate |

| Medical cost escalation | Probable disability |

All about Other Long-Term Employee Benefits

Other Long – Term Employee Benefits include the following:

This standard stipulates simplified accounting method for other long-term benefits and does not require re-measurements in other comprehensive income

Recognition & Measurement

The net total of the following should be recognized in P&L, except to the extent that another IND AS permits or requires their inclusion in the asset cost:

- Service cost

- Net interest on the net defined benefit liability (asset)

- Re-measurements of the net defined benefit liability (asset)

PUCM is used to actuarially value the other long-term benefits.

All about Termination Benefits

It does not cover an employee’s voluntary termination or mandatory retirement. It is generally a lump sum payment and also includes:

- Enhancement of post-employment benefits (through benefit plan)

- Salary to be paid until the end of a specified notice period

Recognition

An employer should recognize termination benefits as a liability and as an expense at the earlier of the following dates:

- The employer can no longer withdraw the offer for those benefits The employer recognizes restructuring cost per Ind AS 37 and involves payment of termination benefits

Measurement

- Measure the termination benefits on initial recognition and recognize subsequent changes with the nature of employee benefit.

- Analyze if the benefits are an enhancement of post-employment benefits or short-term employee benefits or long-term employee benefits.

Disclosure

This standard does not stipulate any specific disclosure but when any other IND AS requires certain disclosures regarding employee benefits they will be needed to be done. For example, IND AS 24 requires disclosures about the key management personnel’s employee benefits, IND AS 1 requires the disclosure of employee benefit expense.

Comparison with AS 15

Some of the key differences between IND AS 19 and AS 15 are given below:

| Sl.No | IND AS 19 | AS 15 |

| 1 | Employees refer to whole time directors only | All types of directors |

| 2 | Employee benefits arising from constructive obligations (an obligation to pay out of conduct and intent of the employee not out of employment contract) are covered | Does not deal with this |

| 3 | Actuarial gains and losses are to be recognized as a part of other comprehensive income and then immediately recognized in retained earnings. Such gain/loss should not be reclassified in P&L of the subsequent period | Actuarial gains and losses are to be recognized immediately in P&L |

| 4 | Requires the use of market yield on government bond for discount rates. | Requires the use of market yield on government bonds for calculating post-employment benefits |

| 5 | Allows, but does not mandate a qualified actuary for post-employment benefit obligation measurement | Neither require nor allows the entity to involve a qualified actuary |

| 6 | Financial assumptions used should be based on market expectations when the obligations are settled. | Does not deal with this |

| 7 | Participates in a defined benefit plan (thereby risk is shared by group entities) This fact has to be disclosed in the financial statements of such entities. | No such provisions |

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption