Salaried Professionals

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Active Investors & Traders

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Everything in Basic +

Global Wealth Builders

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Everything in Premium +

Year-Round Peace of mind

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Everything in Elite +

Salaried Professionals

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Active Investors & Traders

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Everything in Basic +

Global Wealth Builders

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Everything in Premium +

Year-Round Peace of mind

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Everything in Elite +

Salaried Professionals

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Active Investors & Traders

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Everything in Basic +

Global Wealth Builders

Covers Income From

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits

Everything in Premium +

Year-Round Peace of mind

Income sources:

Capital Gains :

- Mutual Funds

- Stocks

- Crypto

- Property Sale

ClearTax Benefits:

Everything in Elite +

Confused about the plans?

Drop your phone number and we will get in touch with you in no time.

no spam calls, we will help you get the best plan possible

Confused about the plans?

Drop your phone number and we will get in touch with you in no time.

Confused about the plans?

Drop your phone number and we will get in touch with you in no time.

+91 8068865688100% Accurate ITR Filed or

Your Money Back

Your return is filed right, or we make it right. 100% refund, no questions asked

Trusted Experts, Verified by ClearTax

Every expert vetted through 50+ quality checks

ICAI Credentials Verified

Every expert's license and track record is checked against official ICAI registries.

Experienced Across Every Tax Scenario

From capital gains to ESOPs to HUF — every expert proves they can handle complex portfolios before they ever handle yours.

Complex Taxes, Clearly Explained

We make sure experts are able to explain complex tax matters clearly — so you always feel informed, never overwhelmed.

Matched to Your Income Profile

Your expert is chosen based on your income type, your complexity, and their track record — so the fit is always right.

ICAI Credentials Verified

Every expert's license and track record is checked against official ICAI registries.

Experienced Across Every Tax Scenario

From capital gains to ESOPs to HUF — every expert proves they can handle complex portfolios before they ever handle yours.

Complex Taxes, Clearly Explained

We make sure experts are able to explain complex tax matters clearly — so you always feel informed, never overwhelmed.

Matched to Your Income Profile

Your expert is chosen based on your income type, your complexity, and their track record — so the fit is always right.

Loved by over 8M+ tax payers

You were really helpful while filing my ITR, as my case got complicated due to the previous person’s mistakes. Thanks again for all the help.

As usual a very seamless process for ITR filing, we have been using ClearTax for several years now!

Akshay was very helpful and flexible. He understood my requirements and filed my returns. I appreciate his service.

I just wanted to express my heartfelt thanks for all your help with the ESOPs. Your expertise and guidance were invaluable, and I really appreciate the time you took to walk me through the process.

This was my first time filing with you guys and had an awesome experience. I will be a permanent customer and will start referring others to your portal.

Was worried about tax filing with increasing complexity and additional income and Form 16, all taken care of by ClearTax.

The tax expert answered all my questions and ensured I claimed every eligible exemption.

Tax expert caught an LTCG exemption I missed last year. Refund ₹18k bigger. Done in 40 minutes.

I recently filed my IT Return with ClearTax Premium Service. The service provided by CA Kiran Kumar was good. Filing was a hassle-free process.

I had a smooth, hassle-free experience. The customer care executives were very helpful and guided me through the entire document upload process with patience and clarity.

Anamika is an absolutely brilliant Chartered Accountant! She made the daunting task of filing my tax return incredibly simple and stress-free.

You were really helpful while filing my ITR, as my case got complicated due to the previous person’s mistakes. Thanks again for all the help.

As usual a very seamless process for ITR filing, we have been using ClearTax for several years now!

Akshay was very helpful and flexible. He understood my requirements and filed my returns. I appreciate his service.

I just wanted to express my heartfelt thanks for all your help with the ESOPs. Your expertise and guidance were invaluable, and I really appreciate the time you took to walk me through the process.

This was my first time filing with you guys and had an awesome experience. I will be a permanent customer and will start referring others to your portal.

Was worried about tax filing with increasing complexity and additional income and Form 16, all taken care of by ClearTax.

The tax expert answered all my questions and ensured I claimed every eligible exemption.

Tax expert caught an LTCG exemption I missed last year. Refund ₹18k bigger. Done in 40 minutes.

I recently filed my IT Return with ClearTax Premium Service. The service provided by CA Kiran Kumar was good. Filing was a hassle-free process.

I had a smooth, hassle-free experience. The customer care executives were very helpful and guided me through the entire document upload process with patience and clarity.

Anamika is an absolutely brilliant Chartered Accountant! She made the daunting task of filing my tax return incredibly simple and stress-free.

Tax expert caught an LTCG exemption I missed last year. Refund ₹18k bigger. Done in 40 minutes.

I recently filed my IT Return with ClearTax Premium Service. The service provided by CA Kiran Kumar was good. Filing was a hassle-free process.

I had a smooth, hassle-free experience. The customer care executives were very helpful and guided me through the entire document upload process with patience and clarity.

Anamika is an absolutely brilliant Chartered Accountant! She made the daunting task of filing my tax return incredibly simple and stress-free.

For the last 2 years I’m filing my tax with ClearTax expert-assisted filing. Their service and timely updates about tax filing and dates made my tax filing process easy and stress-free.

I took an Elite plan from ClearTax. CA Yogesh Kumar Singhania helped me file my income tax. Found the tax expert extremely knowledgeable and he coordinated very well throughout the filing.

ClearTax is a platform that is just too good. This year I had opted for luxury filing where I met 2 amazing personalities. They don’t just help me with the filing but also with my financial planning any time I want for 1 year.

ClearTax has consistently provided the best, most reliable, and highly professional service over the years. Their approach is always efficient, transparent, and trustworthy, making complex processes feel seamless.

They guided me through every step, ensured all deductions were captured, and helped me with smooth ITR filing. Their attention to detail and prompt responses made the experience stress-free.

CA Preety Agarwal patiently walked me through the computation multiple times on my request and ensured everything was double-checked against AIS, TIS, and 26AS.

I would recommend everyone looking for ITR filing to connect with the ClearTax team — well organised team and no discrepancy in process. My tax expert Subham helped me with every step.

Tax expert caught an LTCG exemption I missed last year. Refund ₹18k bigger. Done in 40 minutes.

I recently filed my IT Return with ClearTax Premium Service. The service provided by CA Kiran Kumar was good. Filing was a hassle-free process.

I had a smooth, hassle-free experience. The customer care executives were very helpful and guided me through the entire document upload process with patience and clarity.

Anamika is an absolutely brilliant Chartered Accountant! She made the daunting task of filing my tax return incredibly simple and stress-free.

For the last 2 years I’m filing my tax with ClearTax expert-assisted filing. Their service and timely updates about tax filing and dates made my tax filing process easy and stress-free.

I took an Elite plan from ClearTax. CA Yogesh Kumar Singhania helped me file my income tax. Found the tax expert extremely knowledgeable and he coordinated very well throughout the filing.

ClearTax is a platform that is just too good. This year I had opted for luxury filing where I met 2 amazing personalities. They don’t just help me with the filing but also with my financial planning any time I want for 1 year.

ClearTax has consistently provided the best, most reliable, and highly professional service over the years. Their approach is always efficient, transparent, and trustworthy, making complex processes feel seamless.

They guided me through every step, ensured all deductions were captured, and helped me with smooth ITR filing. Their attention to detail and prompt responses made the experience stress-free.

CA Preety Agarwal patiently walked me through the computation multiple times on my request and ensured everything was double-checked against AIS, TIS, and 26AS.

I would recommend everyone looking for ITR filing to connect with the ClearTax team — well organised team and no discrepancy in process. My tax expert Subham helped me with every step.

Loved by over 8M+ tax payers

4.9/5 stars (2,847 reviews) from various platforms

You were really helpful while filing my ITR, as my case got complicated due to the previous person’s mistakes. Thanks again for all the help.

As usual a very seamless process for ITR filing, we have been using ClearTax for several years now!

Akshay was very helpful and flexible. He understood my requirements and filed my returns. I appreciate his service.

I just wanted to express my heartfelt thanks for all your help with the ESOPs. Your expertise and guidance were invaluable, and I really appreciate the time you took to walk me through the process.

This was my first time filing with you guys and had an awesome experience. I will be a permanent customer and will start referring others to your portal.

Was worried about tax filing with increasing complexity and additional income and Form 16, all taken care of by ClearTax.

The tax expert answered all my questions and ensured I claimed every eligible exemption.

Tax expert caught an LTCG exemption I missed last year. Refund ₹18k bigger. Done in 40 minutes.

I recently filed my IT Return with ClearTax Premium Service. The service provided by CA Kiran Kumar was good. Filing was a hassle-free process.

You were really helpful while filing my ITR, as my case got complicated due to the previous person’s mistakes. Thanks again for all the help.

As usual a very seamless process for ITR filing, we have been using ClearTax for several years now!

Akshay was very helpful and flexible. He understood my requirements and filed my returns. I appreciate his service.

I just wanted to express my heartfelt thanks for all your help with the ESOPs. Your expertise and guidance were invaluable, and I really appreciate the time you took to walk me through the process.

This was my first time filing with you guys and had an awesome experience. I will be a permanent customer and will start referring others to your portal.

Was worried about tax filing with increasing complexity and additional income and Form 16, all taken care of by ClearTax.

The tax expert answered all my questions and ensured I claimed every eligible exemption.

Tax expert caught an LTCG exemption I missed last year. Refund ₹18k bigger. Done in 40 minutes.

I recently filed my IT Return with ClearTax Premium Service. The service provided by CA Kiran Kumar was good. Filing was a hassle-free process.

I had a smooth, hassle-free experience. The customer care executives were very helpful and guided me through the entire document upload process with patience and clarity.

Anamika is an absolutely brilliant Chartered Accountant! She made the daunting task of filing my tax return incredibly simple and stress-free.

For the last 2 years I’m filing my tax with ClearTax expert-assisted filing. Their service and timely updates about tax filing and dates made my tax filing process easy and stress-free.

I took an Elite plan from ClearTax. CA Yogesh Kumar Singhania helped me file my income tax. Found the tax expert extremely knowledgeable and he coordinated very well throughout the filing.

ClearTax is a platform that is just too good. This year I had opted for luxury filing where I met 2 amazing personalities. They don’t just help me with the filing but also with my financial planning any time I want for 1 year.

ClearTax has consistently provided the best, most reliable, and highly professional service over the years. Their approach is always efficient, transparent, and trustworthy, making complex processes feel seamless.

They guided me through every step, ensured all deductions were captured, and helped me with smooth ITR filing. Their attention to detail and prompt responses made the experience stress-free.

CA Preety Agarwal patiently walked me through the computation multiple times on my request and ensured everything was double-checked against AIS, TIS, and 26AS.

I would recommend everyone looking for ITR filing to connect with the ClearTax team — well organised team and no discrepancy in process. My tax expert Subham helped me with every step.

I had a smooth, hassle-free experience. The customer care executives were very helpful and guided me through the entire document upload process with patience and clarity.

Anamika is an absolutely brilliant Chartered Accountant! She made the daunting task of filing my tax return incredibly simple and stress-free.

For the last 2 years I’m filing my tax with ClearTax expert-assisted filing. Their service and timely updates about tax filing and dates made my tax filing process easy and stress-free.

I took an Elite plan from ClearTax. CA Yogesh Kumar Singhania helped me file my income tax. Found the tax expert extremely knowledgeable and he coordinated very well throughout the filing.

ClearTax is a platform that is just too good. This year I had opted for luxury filing where I met 2 amazing personalities. They don’t just help me with the filing but also with my financial planning any time I want for 1 year.

ClearTax has consistently provided the best, most reliable, and highly professional service over the years. Their approach is always efficient, transparent, and trustworthy, making complex processes feel seamless.

They guided me through every step, ensured all deductions were captured, and helped me with smooth ITR filing. Their attention to detail and prompt responses made the experience stress-free.

CA Preety Agarwal patiently walked me through the computation multiple times on my request and ensured everything was double-checked against AIS, TIS, and 26AS.

I would recommend everyone looking for ITR filing to connect with the ClearTax team — well organised team and no discrepancy in process. My tax expert Subham helped me with every step.

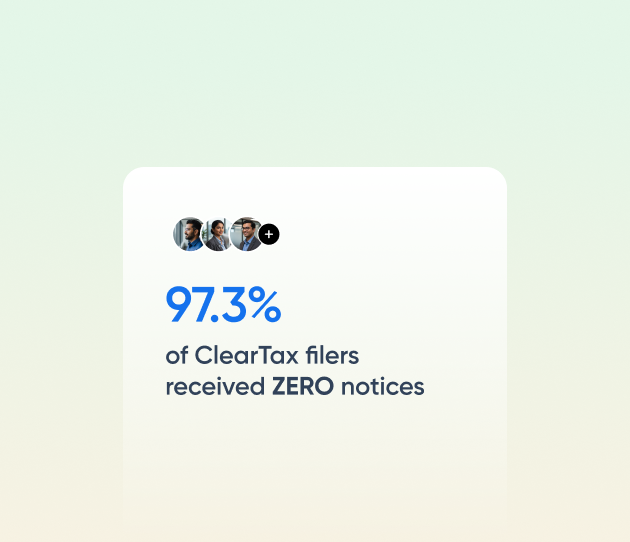

Maximum Tax Refund. No Exceptions.

Every tax-saving

opportunity, found for you

We scan 100+ tax sections so every saving is applied and nothing is left behind.

Getting Indians their

maximum refund, since 2012

₹5,346 Cr refunded to millions of Indians — and the number keeps growing

Getting Indians their

maximum refund, since 2012

₹5,346 Cr refunded to millions of Indians — and the number keeps growing

Every tax-saving opportunity, found for you

We scan 100+ tax sections so every saving is applied and nothing is left behind.

Every tax-saving

opportunity, found for you

We scan 100+ tax sections so every saving is applied and nothing is left behind.

Getting Indians their

maximum refund, since 2012

₹5,346 Cr refunded to millions of Indians — and the number keeps growing

ITR Filed In 24 hours. Guaranteed.

Instant Expert Match

Senior tax expert assigned within the hour. No queues.

Average filing time: 12 hours.

Expert assigned, documents verified, and ITR filed, all done before the day even ends

Zero manual entry. Zero delays.

Form 16, AIS, 26AS — pulled and pre-filled in minutes

Zero Manual Entry.

Zero Delays.

Form 16, AIS, 26AS — pulled and

pre-filled in minutes

ITR Filed In 24 hours. Guaranteed.

Instant expert match

Senior tax expert assigned within the hour. No queues.

Average filing time: 12 hours.

Expert assigned, documents verified, and ITR filed, all done before the day even ends

Zero manual entry. Zero delays.

Form 16, AIS, 26AS — pulled and pre-filled in minutes

Zero Manual Entry.

Zero Delays.

Form 16, AIS, 26AS — pulled and

pre-filled in minutes

ITR Filed In 24 hours. Guaranteed.

Instant expert match

Senior tax expert assigned within the hour. No queues.

Average filing time: 12 hours.

Expert assigned, documents verified, and ITR filed, all done before the day even ends

Zero manual entry. Zero delays.

Form 16, AIS, 26AS — pulled and pre-filled in minutes

Zero Manual Entry.

Zero Delays.

Form 16, AIS, 26AS — pulled and

pre-filled in minutes

File with confidence

Every form, every deduction, handled right

Trusted by employees from

India's biggest brands

Frequently Asked Questions

Can't find your question? Email us.

There are 3 kinds of filing plans available at ClearTax - DIY filing plans, CA-assisted plans, and LIVE ITR filing plans. With the DIY filing plans, you can file your ITR in just 3 mins and 3 simple steps. The CA-assisted plans give you a dedicated tax expert to help you file your taxes. With the LIVE filing plan, a Relationship manager will help schedule LIVE meetings via Google Meet, Zoom, Microsoft Team, Skype, etc. (as per your convenient date & time).

Yes, we offer CA-assisted plans for all kinds of incomes. Our CA-assisted plans for salary and house rent income start from Rs 1299. If you have capital gains income, the plan starts from Rs 3999. We also have CA-assisted plans for self-employed and professionals starting from 3999. Crypto traders can also use our expert-assisted plans, starting from Rs 2999.

- We pre-fill all your details with just one click. Just upload your PAN, and voila! You’re done.

- No need to visit a tax consultant to track your returns. You can do it on ClearTax.

- Our experts will assist you with tax-saving investments based on your tax records.

All we need is your PAN, Form 16, and Form 26AS. If we require any other documents, we will notify you.

Yes, you can file your ITR without a CA via our DIY plans. Click here to check out the plans.

Get an expert to do your taxes for an individual with all kinds of income. No hassle. 100% digital.

- Upload your documents

- Review the computation sheet

- Get ITR verification after e-filing

ITR-1 to ITR-4 applies to individuals and HUFs with income from salary, rent, capital gains, fixed deposit interests, etc. You can choose the appropriate ITR form based on the income earned and source of income. If you are e-filing with ClearTax, we automatically decide on the correct income tax return form.

- Purchase the relevant tax filing plan on our website

- Upload the required documents to your ClearTax account

- We assign a tax expert to you who would file returns for you

- Income tax return is prepared & filed by an expert

Yes, you can file your taxes using ClearTax. Check out our plans here.

Drop your email ID and phone no. here and we will notify you as soon as the ITR filing services start on ClearTax.

Note: In cases where an audit is required as per applicable regulations, the audit fee is not included in this plan price and will be payable separately to the auditor.

*In case of Elite and Luxe plan it can take upto 72 hours because of complex income sources.

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption