What is a Nil Return and when should you file one?

When the income of an individual taxpayer is below the basic exemption limit in a financial year, the tax liability is zero; thus, such individuals do not have to file any income tax return as per provision of Section 139(1) under the Income-tax Act, 1961. But if they file ITRs even when their income is below the basic exemption limit, it is termed ‘Nil Return’.

What is a Nil Return?

A nil income tax return is filed to show the Income Tax Department that you fall below the taxable income and therefore did not pay taxes during the year. Nil returns can be filed only when the income is below the exemption limit. As per the Income Tax Act, it is not mandatory for individuals earning less than the basic exemption limit to file an ITR.

Thus, individuals filing nil returns file it in their interest.

When Should I File a Nil Return?

To show income tax return as proof of income

- There are several instances where income tax serves as proof, say when you are applying for a visa or while getting your passport made.

- This is to continue maintaining a record and also preventative measures in the event of scrutiny from the Income Tax Department.

To claim a refund

Your total income without taking deductions into account could be above the taxable limit, but deductions might be below the minimum exemption limit. If you paid more in taxes than you needed to in the form of TDS, you must file an income tax return to claim a refund.

How to File a Nil Return Online?

Filing a nil return is no different from filing a regular income tax return.

- Enter your income details and deductions. Income tax is computed, and you will be shown that you have no tax due.

- Submit your return to the Income Tax Department. E Verify your ITR to complete the e-filing process.

Benefits of Filing Nil Returns

- ITR may be required for applying for a visa.

- Passport applications accept Nil ITR as valid proof of address.

- ITR is required for loan applications as supporting evidence to ascertain eligibility.

- Banks may deduct TDS on interest on deposits. The TDS refund can be claimed by filing nil ITR.

- A few organizations may deduct the TDS of people working as consultants or freelancers while disbursing their payment. They need to file nil ITR to claim a TDS refund when they don’t fall in the tax bracket.

- Filing ITR is mandatory for individuals who own a foreign asset even when their income is below the threshold.

- It is possible to carry forward losses incurred in the stock market by filing nil ITR when the income is below the threshold.

- It is mandatory to file ITR for the following categories -

- If you have deposited an amount or aggregate of the amounts exceeding one crore rupees in one or more current accounts maintained with a banking company or a cooperative bank; or

- If you have incurred expenditure of an amount or aggregate of the amounts exceeding two lakh rupees for himself or any other person for travel to a foreign country; or

- If you have incurred expenditure of an amount or aggregate of the amounts exceeding one lakh rupees towards consumption of electricity

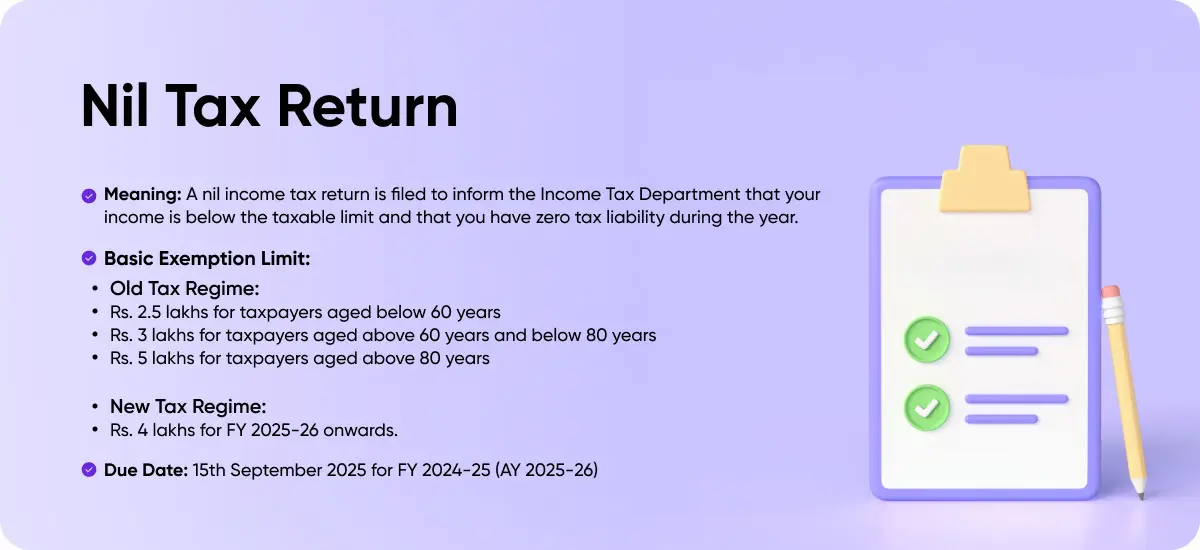

Due Date to File Nil Income Tax Return

Individuals must file a nil return before 31st July of the subsequent Tax Year. The due date for filing a nil ITR is the same as a regular return. However, if the nil return is filed after the due date, it will be considered a belated return. In case of belated filing of nil returns, no late filing fees will be charged.

Nil Tax Return - Summary

The following image summarises the key information related to nil ITR.

Frequently Asked Questions

About the Author

Ektha Surana

Multitasking between pouring myself coffees and poring over the ever-changing tax laws. Here, I've authored 100+ blogs on income tax and simplified complex income tax topics like the intimidating crypto tax rules, old vs new tax regime debate, changes in debt funds taxation, budget analysis and more. Some combinations I like- tax and content, finance & startups, technology & psychology, fitness & neuroscience. Read more

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption