|

Comparison of GSTR-3B vs GSTR-2A : Importance, Reconciliation & Report

GSTR-3B vs GSTR-2A is an important exercise that businesses must not miss out on. It helps businesses claim the full Input tax credit (ITC) and also reverse any excess ITC claimed. In turn, the reconciliation before filing GSTR-3B will help avoid any potential demand notices from the tax authorities. With GSTR-2B introduced in July-August 2020, matching ITC to be claimed in GSTR-3B with GSTR-2A has now moved to a yearly affair, yet important for TDS and TCS credit.

GSTR-3B vs GSTR-2A

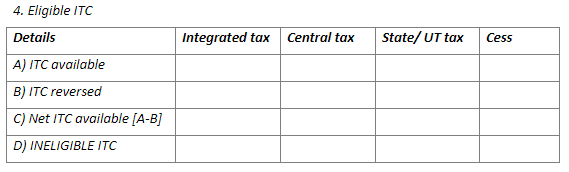

Form GSTR-3B is a monthly summary return filed by the taxpayer by the 20th of the next month or 22nd/24th of month following the quarter. Taxpayers are allowed to take the input tax credit (ITC) based on the details declared by the taxpayer in Table 4 of Form GSTR – 3B:

Form GSTR-2A is an auto-populated form generated in the recipient’s login, covering all the outward supplies (Form GSTR – 1) declared by his suppliers.

When the supplier files GSTR – 1 in any particular month disclosing his sales, the corresponding details are captured in GSTR-2B and GSTR – 2A of the recipient. While the filing of Form GSTR – 2 has been kept in abeyance, it’s still important under the GST framework for the taxpayers to reconcile the ITC claimed in Form GSTR – 3B and Form GSTR – 2A. GSTR – 3B is a summary return. Hence, the amount of ITC available as disclosed in Table 4(a) must match with tax details disclosed in Form GSTR-2B regularly, along with GSTR – 2A.

How to reconcile GSTR-3B and GSTR-2A

Taxpayers must follow certain steps to reconcile GSTR-3B with GSTR-2A.

- Begin by collating the GSTR-2A and ITC data in Table-4 of GSTR-3B for a specific period.

- Choose a suitable method for reconciliation- either manually using the spreadsheet/ by automating some redundant tasks using the SaaS-based software.

- The list of ITC available entries in GSTR-2A could add up to the eligible ITC in Table-4 of GSTR-3B for each component- CGST, SGST and IGST.

- Do reconciliations between these two statements at vendor-level to identify and communicate with vendors where any ITC claimed in earlier returns, now need to be reversed due to underreporting by the vendor for the period.

- Matching the two data sets should give you the following results-

- Matched

- Not matched

- Partially matched ( invoice number not matching, but value matches)

- Suggested match (available on Clear GST, this filter in matching allows one to identify closest matches between GSTR-2A/2B and GSTR-3B through smart fuzzy logics).

- It is essential to keep the GSTR-3B values of a period at par with the GSTR-2B values. For any ITC claims made over and above the GSTR-2A, ensure eligibility criteria as per the CGST Act and Rules is fulfilled.

Importance for GSTR-3B vs GSTR-2A

It is important to reconcile Form GSTR – 3B and Form GSTR – 2A on account of the following reasons:

- GST authorities have issued notices to a large number of taxpayers asking them to reconcile the ITC claimed in a self-declared summary return Form GSTR – 3B with the auto-generated Form GSTR-2B and Form GSTR – 2A. Such notices are issued in Form GST ASMT – 10. The taxpayer would be required to reply to such notices or pay the differential amount.

- Tax evaders claiming ITC on the basis of fake invoices have also been penalised in the past.

- Reconciliation ensures that credit is being claimed for the tax which has been actually paid to the supplier.

- Ensures that no invoices have been missed/recorded more than once, etc.

- In case the supplier has not recorded the outward supplies in Form GSTR – 1, communication can be sent out to the supplier to ensure that the discrepancies are corrected.

- Errors committed while reporting details in GSTR-1 by suppliers or GSTR-3B by recipients can be rectified.

Use the Clear GST software to identify the differences between the GSTR-3B vs GSTR-2A/2B vs books .

Reconciliation at the time of filing of Annual return: Even at the time of filing an Annual return in Form GSTR – 9, reconciliation of ITC as per GSTR – 3B and GSTR – 2A is required to be done in Table 6 and Table 8 across months.

Reasons for non-reconciliation of GSTR-2A vs 3B

The details disclosed in Form GSTR – 2A and Form GSTR – 3B may not reconcile on account of the following reasons:

- The credit of IGST claimed on the import of goods

- IGST Credit on the import of services

- The credit of GST paid on reverse charge mechanism, etc.

- Transitional credit claimed in TRAN – I and TRAN – II.

- ITC for goods and services received in FY 2020-21 but availed in FY 2021-22.

In the cases mentioned above, the figures will not reconcile as no corresponding Form GSTR – 1 is filed by the supplier or the ITC is being claimed at a later date.

After Identifying mismatches by GSTR-2A vs GSTR-3B

After considering the situations mentioned above, if any discrepancies are found in Form GSTR – 2A and GSTR -3B leading to any excess ITC claimed by the recipient, the same must be paid by the taxpayer along with interest. It is, therefore, necessary that this reconcile exercise is done on a regular basis to ensure that only bonafide input tax credit is claimed.

How can Clear GST help you?

Clear GST offers easy import and download of GST data for preparation of GST returns. It provides various options for a user to ingest data to prepare the GSTR-1, GSTR-3B or any other return in under minutes. Options like excel ingestion or direct integration with ERP are available for importing sales or purchase data onto the Clear GST software.

The best part is, you have to import the sales data for GSTR-1 just once. Based on this, the software auto-populates the details into GSTR-3B in a click of a button. Thus, one can avoid errors and ensure 100% accuracy in reporting of data with minimal manual intervention.

Clear GST also provides useful insights under the REPORTS section so you can speed through the journey of GST compliance in a hassle-free way! The report of ‘GSTR-3B vs GSTR-2A ITC Comparison Report’ helps you compare GSTR-2A with GSTR-3B.

This report helps you compare the ITC reported in GSTR-3B by you with the ITC reflected on the GSTR-2A. Further, you can compare the data month-wise or for every financial year. You can also compare data at GSTIN level or cumulatively at PAN level.

Advantages of GSTR-3B vs 2A report

- Download GSTR-2A anytime across months from the GST portal to start comparing with GSTR-3B data. Verify GST login once using OTP, and continue to easily update data in a click, anytime and anywhere.

- Check the difference for every field such as B2B other than reverse charge to compare ITC between GSTR-2A and GSTR-3B.

- ITC comparison at PAN and GSTIN level is available.

- Know the differences instantly at a monthly level or at a quarterly level, to take further action.

How to get GSTR-3B vs GSTR-2A Report?

– Health check Report gives a complete picture of GSTR-3B vs GSTR-2A both at a summary and monthly or yearly levels. Follow these simple steps to get a complete GSTR-3B vs GSTR-2A ITC comparison report.

You can alternatively download the ‘GSTR-3B vs GSTR-2A ITC Comparison Report’ from the report dashboard to get a comparison of data at a glance.

Follow the steps as mentioned below:

Step 1: Login to Clear GST and on the dashboard, click on ‘Reports’ tab.

Step 2: Click on the ‘GSTR-3B vs GSTR-2A report tile and choose the business for which you want to compare the two returns.

Step 3: Choose Financial Year Select the financial year for which you want the report to be generated.

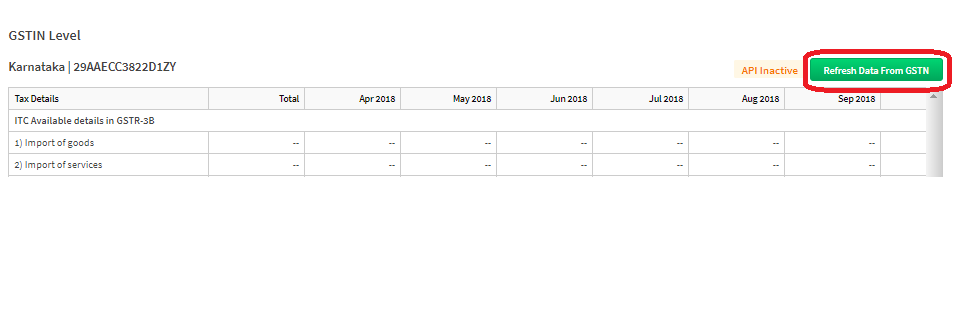

Step 4: Generate Report If the GSTR-1 and GSTR-3B are both filed using Clear GST, then the report is displayed for your use. But if you have not used the software before, just click on the button ‘Refresh Data from GSTN’ appearing on the right-hand side of the report section ‘GSTIN level’. The yearly return data from GSTN will be fetched after verification via an OTP based on login credentials. 2

Step 5: View/Download Report Notice the difference displayed in the reports section. Click on link ‘Download report as excel’ to use and share the report offline in excel form.

Frequently Asked Questions

About the Author

Annapoorna

I preach the words, “Learning never exhausts the mind.” An aspiring CA and a passionate content writer having 8+ years of hands-on experience in deciphering jargon in Indian GST, Income Tax, off late also into the much larger Indian finance ecosystem, I love curating content in various forms to the interest of tax professionals, and enterprises, both big and small. While not writing, you can catch me singing Shāstriya Sangeetha and tuning my violin ;). Read more

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption