Call Now

Call Now

Golden Rules of Accounting: Overview, Types, and Examples

Every economic entity must present its financial information to all its stakeholders. The information provided in the financials must be accurate and present a true picture of the entity. For this presentation, it must account for all its transactions. Since economic entities are compared to understand their financial status, there has to be uniformity in accounting.

To bring about uniformity and to account for the transactions correctly there are three Golden Rules of Accounting. These rules form the very basis of passing journal entries which in turn form the basis of accounting and bookkeeping.

So, it is very important to know the three accounting golden rules that simplify the complicated task of recording financial transactions. In this article, we have tried to explain the three golden rules of accounting is simple words with examples.

What are the Golden Rules of Accounting?

To put it in simple terms, the golden rules of accounting are a set of guidelines that accountants can follow for the systematic recording of financial transactions. They revolve around the system of dual entry i.e., debit and credit. You have to know which accounts have to be debited and which needs to be credited.

These rules will assist in identifying which account to credit and which one to debit. The accounting golden rules are a set of principles that allow one in simplifying the complex rules of bookkeeping.

According to these rules, you must determine the type of account for each transaction. Now, each account type has its own set of principles that needs to be applied for every single transaction.

To get a better idea, let’s take a look at the types of accounts.

Types of Accounts

In financial accounting, every debit or credit transaction entry will belong to one of the three types of accounts:

1. Nominal account

A nominal account is a general ledger containing the temporary transactions of a business, namely – expenses, incomes, profits and losses for a specific period. It contains all the transactions that occur in one fiscal year. Furthermore, it resets to zero and starts afresh when the next fiscal year begins.

Examples of nominal accounts are Commission Received, Salary Account, Rent Account and Interest Account.

2. Personal account

You can think of a personal account as a general ledger that relates to people, associations and companies.

It can be divided into three subcategories:

- Artificial personal account

An artificial personal account represents bodies which are not human beings but act as separate legal entities according to the law. For example, government bodies, hospitals, banks, companies, cooperatives, partnerships, etc.

- Natural personal account

Accounts which relate to individuals—for example, a Capital account, a Drawings account, Creditors, Debtors, etc.

- Representative personal account

This type of personal account represents a particular person or group of persons. However, the transactions in this type of account either belong to the previous or the coming year.

For example, a representative personal account can contain information on an employee’s due salary from last year. Also, it can represent the amount of rent a company paid in advance for the coming year.

3. Real account

Like the other two, a real account is also a general ledger, but it contains transactions related to the liabilities and assets of a company. The assets, in this case, can be further subdivided into tangible and intangible assets.

Tangible assets include land, buildings, machinery, furniture, etc. Alternatively, intangible assets include goodwill, patents, copyrights, etc.

Unlike a nominal account, a real account does not close when a financial year completes. Rather, it is carried forward to the following year. In addition, a real account also appears in the company’s balance sheet.

Now that you have a clear idea of the types of accounts, let’s take a look at how they relate to the golden rules of accounting.

Golden Rules of Accounting

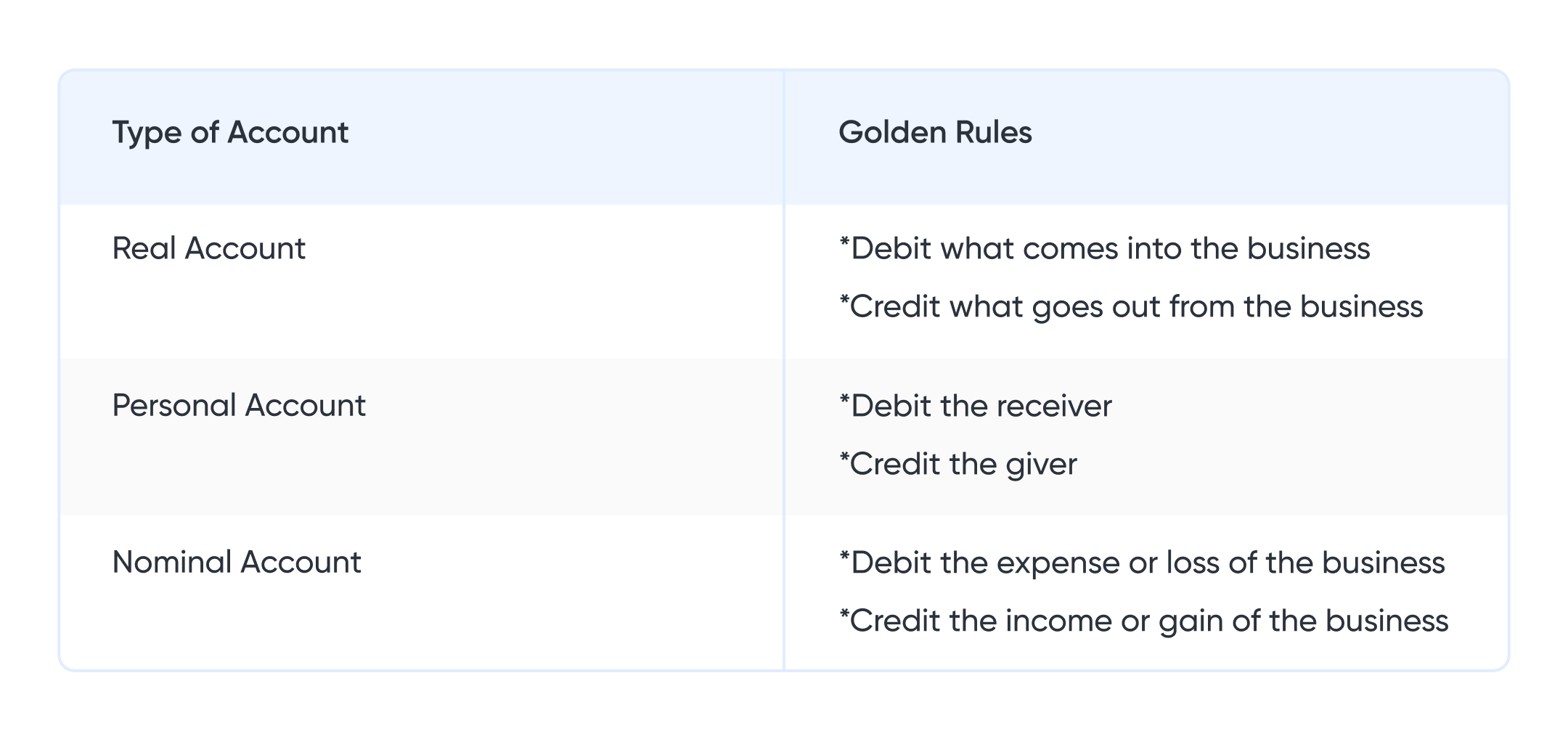

Rule 1: Debit all expenses and losses, credit all incomes and gains

This golden accounting rule is applicable to nominal accounts. It considers a company’s capital as a liability and thus has a credit balance. As a result, the capital will increase when gains and income get credited. Inversely, this capital gets reduced when losses and expenses are debited from it.

| Date | Account | Debit | Credit |

| xx/xx/xxxx | Rent Account | Rs.28,000 | – |

| xx/xx/xxxx | Cash Account | – | Rs.28,000 |

Rule 2: Debit the receiver, credit the giver

The “Debit the receiver, Credit the giver” rule is applicable for personal accounts. When a natural or artificial entity makes a payment to a company, it becomes an inflow. Thus, the receiver must be debited, and the company receiving the payment must be credited in the books.

| Date | Account | Debit | Credit |

| xx/xx/xxxx | Purchase | Rs.19,000 | – |

| xx/xx/xxxx | Present Shop | – | Rs.19,000 |

Rule 3: Debit what comes in, credit what goes out

This rule is applicable for real accounts where tangible assets like machinery, buildings, land, furniture, etc., are taken into account. They have a debiting balance by default and debit everything that comes in, adding them to the existing account balance.

In a similar way, the account balance needs to be credited when a tangible asset leaves the company.

| Date | Account | Debit | Credit |

| xx/xx/xxxx | Machinery Account | Rs.1,90,000 | – |

| xx/xx/xxxx | Cash Account | – | Rs. 1,90,000 |

These three accounting rules form the basis of bookkeeping. Let’s take an example to put things into perspective.

Take a look at the following transactions:

- Suppose a company named Bhattacharya Tiles starts its business with a capital of Rs.2,00,000.

- It rents property worth Rs.50,000

- The firm buys goods worth Rs.1,00,000 from Mahadev Stone Works, on Credit

- It sells goods worth Rs.1,50,000

- Then, it pays Mahadev Stone Works in cash for the purchased goods

- Furthermore, the company pays Rs.1,00,000 worth of salary to its employees

Now, let’s take a look at the different accounts that will be involved and also the types of accounts for each case:

| Transactions | Involved Accounts | Accounts Types |

| Initial capital of Rs. 2,00,000 | Capital Account, Cash Account | Personal Account, Real Account |

| Rents worth Rs.50,000 | Cash Account, Rent Account | Real Account, Nominal Account |

| Purchase of goods worth Rs.1,00,000 from Mahadev Stone Works | Mahadev Stone Works Account, Purchases Account | Personal Account, Nominal Account |

| Sale of goods worth Rs.1,50,000 | Sales Account, Cash Account | Nominal Account, Real Account |

| Cash payment to Mahadev Stone Works for goods purchased | Cash Account, Mahadev Stone Works Account | Real Account, Personal Account |

| Salary payment to employees worth Rs.1,00,000 | Cash Account, Salary Account | Real Account, Nominal Account |

Applying the golden rules of accounting, your journal entries will be in the following ways:

- Bhattacharya Tiles starts its business with a capital of Rs.2,00,000.

As cash is a tangible asset, it will be a part of the company’s real account. Also, capital belongs to the personal account.

Therefore, applying the golden rules, you have to debit what comes in and credit the giver.

| Account Type | Debit | Credit |

| Cash Account | Rs.2,00,000 | – |

| Capital Account | – | Rs.2,00,000 |

- Rents property worth Rs.50,000

Rent is considered as an expense and thus falls under the nominal account. Additionally, cash falls under the real account. So, according to the golden rules, you have to credit what goes out and debit all losses and expenses.

| Account Type | Debit | Credit |

| Rent Account | Rs.50,000 | – |

| Cash Account | – | Rs.50,000 |

- Buys goods worth Rs.1,00,000 from Mahadev Stone Works on Credit

When a firm purchases something, it falls under its expenses, and so it falls under the nominal account. Moreover, Mahadev Stone Works will be a part of the personal account. Hence, you have to credit the giver and debit all expenses and losses.

| Account Type | Debit | Credit |

| Purchases Account | Rs.1,00,000 | – |

| Mahadev Stone Works Account | – | Rs.1,00,000 |

- Sells goods worth Rs.1,50,000

Income generated from the selling of goods falls under the nominal account. Furthermore, cash forms a part of the real account. Therefore, you have to credit all incomes and gains and debit what comes in.

| Account Type | Debit | Credit |

| Cash Account | Rs.1,50,000 | – |

| Sales Account | – | Rs.1,50,000 |

- Pays Mahadev Stone Works in cash for the purchased goods

As Mahadev Stone Works falls under the personal account and cash forms a part of the real account, you have to credit what goes out and debit the receiver.

| Account Type | Debit | Credit |

| Mahadev Stone Works Account | Rs.1,00,000 | – |

| Cash Account | – | Rs.1,00,000 |

- The company pays Rs.1,00,000 worth of salary to its employees

Salary is considered as an expense to a business and thus falls under the nominal account. In addition, cash forms a part of the real account. So, according to the accounting golden rules, you have to credit what goes out and debit all expenses and losses.

| Account Type | Debit | Credit |

| Salary Account | Rs.1,00,000 | – |

| Cash Account | – | Rs.1,00,000 |

Benefits of the Golden Rules of Accounting

Following the golden rules of accounting has these benefits:

- Proper maintenance of business records

For a company’s success, the proper maintenance of its records is critical. Doing so will make sure that the company’s records are stored in a safe, and systematic manner.

- Comparing financial results

The golden rules ensure that financial records are properly recorded. So, businesses can compare their year-over-year financial results in an easier and more efficient way.

- Calculating the valuation of a business

When a firm properly calculates its financial statements, it assists in proper business valuation. Furthermore, it helps in getting more investments and thereby expanding the business.

- Helps in budgeting as well as future projections

If a business has a sound budget based on proper accounting practices, it can act as a strong foundation for growth. In addition, it assists in more accurate future projections.

- Evidence during legal cases

For quick reference during lawsuits, companies need to record their financial data in a systematic manner. Using accounting golden rules comes in handy in this regard.

- Assists in tax-related matters

Properly accounting a firm’s financial statements helps avoid shortfalls in taxes. Improper accounting practices attract huge penalties. It can also impact the firm’s brand value and image.

- Helps comply with regulatory authorities

Proper accounting is of utmost importance when it comes to complying with regulatory authorities. Without proper accounting discipline, it will be difficult for any business to achieve regulatory compliance.

Now that you have a clear idea of the golden rules of accounting, you know which type of transaction belongs under which specific account. So, the journal entries on financial transactions shall be accurate and appropriate.

Conclusion

All transactions of an entity must be accounted for. To account these transactions the entity must pass journal entries which will then summarise into ledgers. The journal entries are passed on the basis of the Golden Rules of accounting. To apply these rules one must first ascertain the type of account and then apply these rules.

These lay the foundation of accounting and hence are called the Golden Rules of accounting. They are like the letters of the English alphabet. If one does not know the letters he cannot put words and hence, will not be able to use the language. Similarly for accounting, if one does not know the golden rules, he cannot pass journal entries and hence won’t be able to accurately account for the transactions.

Related Articles

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption