Sukanya Samriddhi Yojana 2026: Latest Interest Rates, Tax Benefits, and How to Calculate Returns?

Sukanya Samriddhi Yojana (SSY) is a government-backed savings scheme for the girl child. Parents or legal guardians can invest under this scheme to secure their daughter’s future. Minimum and maximum investment of SSY scheme is Rs. 250 and Rs. 1.5 Lakh respectively, per financial year.

Such contributions qualify for section 80C deduction up to Rs 1.5 Lakh. While the interest rate is 8.2% per annum for Q4 (Jan-Mar) FY 2025-26, the interest and maturity proceeds are tax-free.

Sukanya Samriddhi Yojana Interest Rate 2026

- For January-March 2026 (Q4 - FY 2025-26), the interest rate is 8.2% per annum (compounded yearly).

- This is higher than many fixed deposits and other government schemes, making SSY highly attractive for conservative investors.

- The interest for the SSY account is calculated on the lowest balance for the calendar month, and is credited once, at the end of each financial year.

Historical Interest Rates (SSY)

| Year | Apr-Jun (Q1) | Jul-Sep (Q2) | Oct-Dec (Q3) | Jan-Mar (Q4) |

| 2025-2026 | 8.2% | 8.2% | 8.2% | 8.2% |

| 2024-2025 | 8.2% | 8.2% | 8.2% | 8.2% |

| 2023-2024 | 8.0% | 8.0% | 8.0% | 8.2% |

| 2022-2023 | 7.6% | 7.6% | 7.6% | 7.6% |

| 2021-2022 | 7.6% | 7.6% | 7.6% | 7.6% |

| 2020-2021 | 7.6% | 7.6% | 7.6% | 7.6% |

| 2019-2020 | 8.5% | 8.4% | 8.4% | 8.4% |

| 2018-2019 | 8.1% | 8.1% | 8.5% | 8.5% |

| 2017-2018 | 8.4% | 8.3% | 8.3% | 8.1% |

Sukanya Samriddhi Yojana Calculator 2026

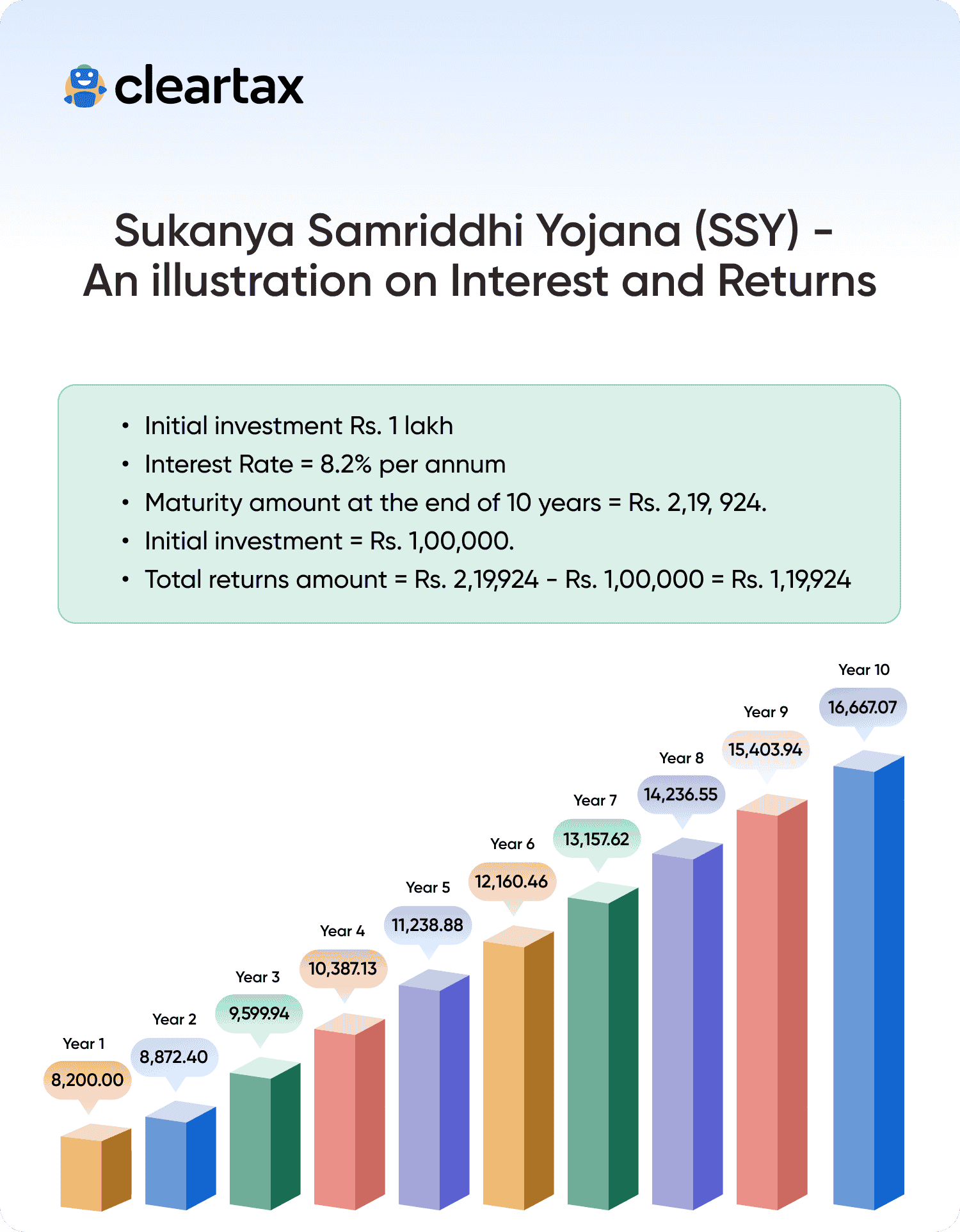

SSY Scheme- An Illustration

If you deposit Rs. 1 lakh in a particular financial year, the accumulation of interest on that fund over a span of 10 years is represented in the bar chart below. Please be informed that the below illustration is to demonstrate the returns of amount invested in SSY scheme over a period, though the annual investment requirements and the duration of the investment may vary.

Sukanya Samriddhi Yojana 2026 - Features & Eligibility

Opening Account Rules & Age Limit

- Account opening: Must be done before the girl turns 10 years old.

- SSY Account Eligibility: Only for resident Indian girl children.

- Account holders: Parents or legal guardians can open an SSY account.

- Family limit: Up to two SSY accounts per family (one for each girl).

- If the family has twins/triplets in the first or second birth, more than two accounts can be opened.

- If the first birth results in multiple girl children, no additional SSY account will be allowed for subsequent girls in the same birth.

Deposit Rules

- Minimum deposit: Rs 250 per year.

- Maximum deposit: Rs 1.5 lakh per year.

- Maturity period: 21 years from the date of account opening.

- Deposit methods: Cash, cheque, DD, or online transfer.

- Guardian role: Guardian can deposit and operate the account until the girl turns 18 years old.

Beneficiary

- Any girl child who is a resident Indian can be a beneficiary under SSY from the time of opening the account till the time of maturity/closure.

- The SSY account should be operated by the girl child after she attains the age of 18 years.

Interest Rate

- Current interest rate: 8.2% per annum (for the 3rd quarter of FY 2026-2026).

- Interest calculation: Calculated on the minimum balance between the last day of the month and the 5th day of the following month.

- Tax status: Interest is tax-free under section 10 of Income Tax Act.

Maturity Period

- The maturity period of SSY is 21 years from the date of account opening.

- But closure of account permitted before 21 years in case of fund required for girl child marriage expenses only after girl child turned 18 years old or more.

- On maturity Interest and principal will be paid to the girl child on submission of an application and proof of identity, residence,age proof, and citizenship documents.

Premature Closure of SSY Account

Sukanya Samriddhi Yojana (SSY) can be prematurely closed only in the following situations:

- Marriage: After the girl turns 18, an application for closure can be submitted between 1 month before marriage and 3 months after marriage, along with age proof.

- Death: If the girl child dies, the balance will be paid to the guardian upon submission of the death certificate.

- Medical emergencies: Premature closure allowed in case of life-threatening diseases of the account holder or death of the guardian.

- General premature closure: If closure is made for reasons other than the above, the account will earn interest at post-office savings account rate (lower than SSY interest rate).

Pre- Maturity Withdrawal Rules

- Withdrawal limit: 50% of the account balance as of the previous financial year’s end.

- Purpose: Can only be used for educational or marriage expenses.

- Age limit: This withdrawal is allowed only when the child has crossed 18 years or passed 10th Standard, whichever is earlier

- Installments: Withdrawal can be made in lump-sum or in 5 equal installments.

- Documentation required: Form-3, along with proof of educational or marriage expenses (e.g., admission fee slip, bills, and SSY passbook).

- Withdrawal cap: The withdrawal amount cannot exceed the fees for admission or other fees to higher education (as mentioned in the fee slip).

Default Rules

- If the minimum amount is not deposited for the financial year, the account will be categorised as 'Account under Default'.

- Accounts under default can be regularised within 15 years of account opening, by depositing the missed minimum deposits and penalty of Rs. 50 per year.

- Though the account is categorised as an “Account under Default” the interest amount will be earned for the amount already deposited.

No Interest Payable

- After the completion of the tenure of the SSY, i.e., after 21 years from account opening.

- After the girl child becomes a non-citizen or a non-resident of India.

- Any deposit made above the maximum cap, i.e., Rs.1.5 lakh per year will not earn any interest and will not be allowed as a deduction. Excess deposits will be immediately refunded.

Sukanya Samriddhi Yojana Tax Benefits

Sukanya Samriddhi Yojana enjoys the Exempt-Exempt-Exempt (EEE) tax status, which is the most favorable in tax-saving schemes.

- Deduction on Deposits: SSY deposit amount per month or per annum, eligible for Section 80C deduction up to ₹1.5 lakh per year.

- Tax-free interest: Interest earned on the SSY account balance annually is fully exempt under section 10 of the Income Tax Act.

- Tax-free maturity: Final proceeds, including interest and principal amount, are exempt from income tax.

Comparison of Sukanya Samriddhi Yojana, PPF and NSC

Feature | Sukanya Samriddhi Yojana (SSY) | Public Provident Fund (PPF) | National Savings Certificate (NSC) |

| Minimum Investment | ₹250 per financial year | ₹500 per financial year | ₹ 1,000 |

| Maximum Investment | ₹1.5 lakh per financial year | ₹1.5 lakh per financial year | No maximum limit |

| Eligible Age | Girl child below 10 years at account opening | Any Indian resident individual | Any Indian resident individual |

| Maturity Period | 21 years from account opening (or marriage after age 18) | 15 years (extendable in blocks of 5 years) | 5 years |

| Interest Rate (FY 2025–26, Q4) | 8.2% p.a., compounded annually | 7.1% p.a., compounded annually | 7.7% p.a., compounded annually |

Documents Required for Sukanya Samriddhi Yojana

You have to walk down to the post office or a bank branch where you have submitted the SSY application to submit the documents and proofs. You need to submit a physical copy of the following documents:

- Birth certificate of the girl child

- Identity and address proof of the guardian

- Medical certificate for proof of birth of multiple girl children on a single order of birth

- Other KYC documents, such as Aadhaar card, Voters ID, etc.

- Any other documents as required by the post office or banks

How to Open a Sukanya Samriddhi Yojana Account in a Post Office?

Sukanya Samriddhi Yojana (SSY) account can be opened with a participating bank (designated bank) or a Post Office branch. You need to follow the below procedure to open the account:

- Visit the bank or post office branch where you would like to open the account.

- Fill up the application form (Form-1) with relevant details and provide supporting documents.

- Pay the first deposit in the form of cash, cheque, or demand draft. The amount can be anything from Rs. 250 up to Rs.1.5 lakh.

- The bank or post office will process your application and payment.

- Upon processing, your SSY account will be opened. A passbook will be issued for this account marking the initiation of the account.

It is recommended to open a Sukanya Samriddhi Yojana account as early as possible, to secure the financial needs of your daughter's future.

Download Important Forms For Sukanya Samriddhi Yojana

Important forms under the Sukanya Samriddhi Yojana (SSY) Scheme are given below:

| Form No | Form Type |

| Form 1 | Application for account opening |

| Form 2 | Pay-in-slip |

| Form 3 | Application for Loan/Withdrawal |

| Form 4 | Pass Book |

| Form 5 | Application for transfer of account |

| Form 6 | Application for extension of account |

| Form 7 | Application for pledging of account |

| Form 8 | Application for premature closure of account |

| Form 9 | Application for closure of account |

| Form 10 | Application for cancellation or variation of nomination in an account |

| Form 11 | Application for settlement of an account of the deceased depositor |

| Form 12 | Letter of authority to open or operate an account on behalf of depositor |

| Form 13 | Affidavit |

| Form 14 | Letter of disclaimer |

| Form 15 | Letter of indemnity |

How to Open a Sukanya Samriddhi Yojana Account through Banks?

- You can open a Sukanya Samriddhi Yojana account either with a participating bank or a post office branch.

- However, it is more convenient for you to open an SSY account with the bank where you already hold a savings account if it is one of the participating banks.

- You can visit the respective banks’ websites to download the SSY Account Opening Application Form.

- You need to fill the form and submit it to the participating bank to open the SSY account. The participating banks are:

List of Designated Banks | ||

| State Bank of India | Allahabad Bank | Andhra Bank |

| Punjab and Sind Bank | Bank of Baroda | Canara Bank |

| Bank of India | Bank of Maharashtra | Corporation Bank |

| Central Bank of India | Indian Overseas Bank | Dena Bank |

| UCO Bank | Punjab National Bank | Union Bank of India |

| Syndicate Bank | Oriental Bank of Commerce | IDBI Bank |

| United Bank of India | Axis Bank | ICICI Bank |

The form and procedure will remain same as above.

Sukanya Samriddhi Yojana Online Payment

You have to download the IPPB app on your smartphone to make online payments towards your SSY account. Through this app, you can set standing instructions so that a specified amount will be transferred online to your SSY account. Here is the step-by-step procedure:

Step 1: Transfer money from your bank account to the IPPB account.

Step 2: On the IPPB app, go to DOP Products / Services tab and choose the Sukanya Samriddhi Yojana account.

Step 3: Enter your SSY account number and the customer ID.

Step 4: Choose the amount you would like to pay and the installment duration.

Step 5: IPPB will notify you of the success of setting up the payment routine.

Each time the app makes the money transfer, you will be notified of the same.

How to Transfer a Sukanya Samriddhi Account from the Post Office to a Bank?

To transfer the SSY account from a post office to a bank, follow these instructions:

- Visit the PO branch where the account is held. The girl child need not visit the PO branch as the guardian can complete the process.

- Inform the PO executive about your intent to transfer the SSY account.

- Submit the duly filled account transfer form and KYC documents. The executive will verify the details and transfer the account on your request.

- Now, visit the bank branch where you would like to maintain the SSY account.

- Submit the self-attested KYC documents and any other paperwork provided to you by the PO executive while requesting to maintain the account with them.

- Once the bank executive processes your request, a new passbook will be provided.

The balance in the SSY can be transferred anywhere in India – from or to post offices, from or to banks, and between post offices and banks free of cost. This can be done upon furnishing proof of a change of residence of either the guardian or the girl child. Under any other circumstance, such a transfer can be made by paying a fee of Rs 100.

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption