Call Now

Call Now

ITR U – What is ITR-U Form and How to File ITR-U?

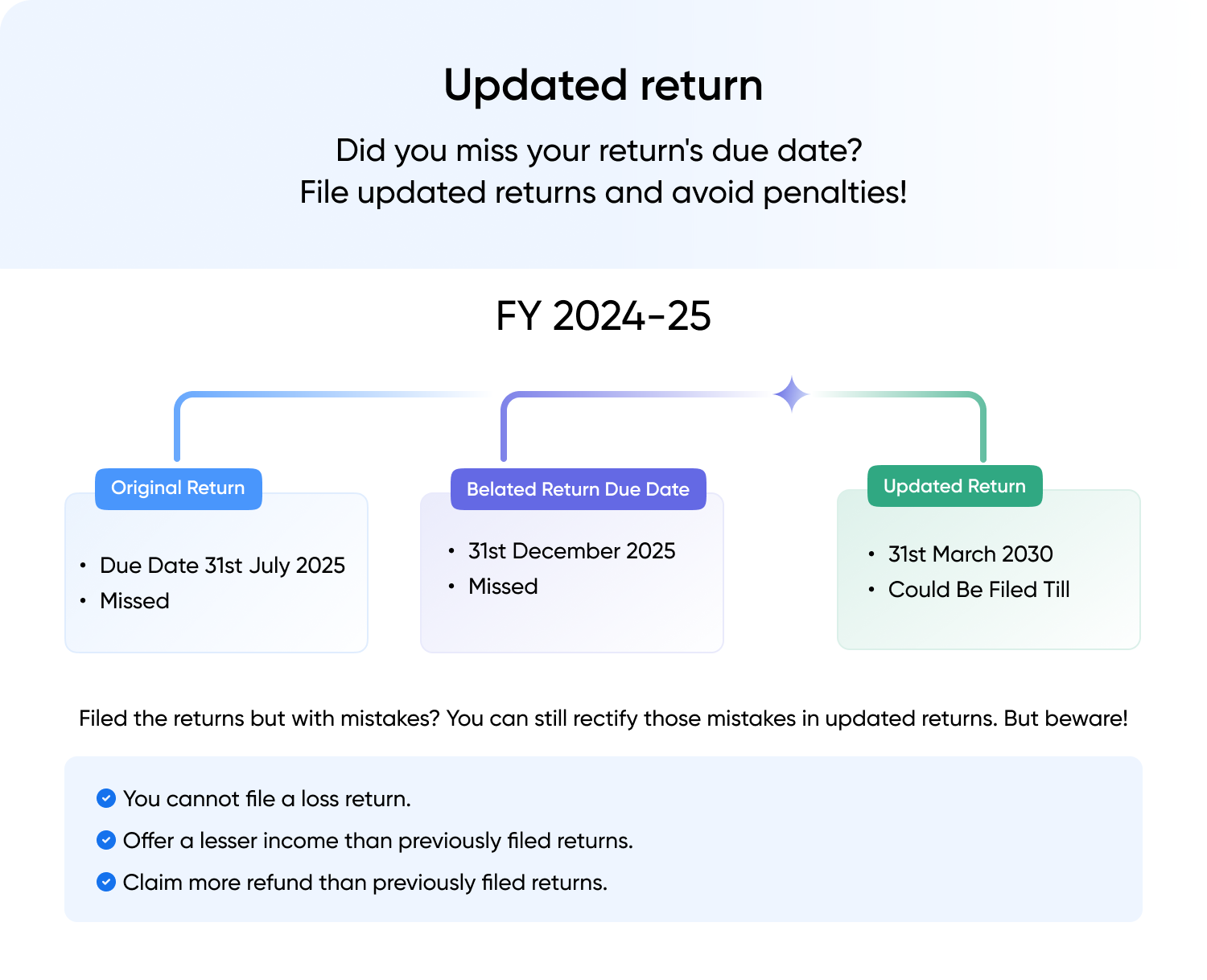

Updated Income Tax Return or ITR-U means a form that allows you to rectify errors or omissions and update your previous ITR. It can be filed within four years from the end of the relevant assessment year. You can file ITR-U for preceding 4 assessment years (48 months). For FY 2024-25, ITR-U can be filed between 1st April 2026 to 31st March 2030. In this article, we explain ITR-U in detail, including when it can be filed, the conditions under which it is allowed, and how additional tax liabilities are calculated.

Budget 2026 Update

As per the budget 2026 proposals, updated return can be filed even after the beginning of re-assessment proceedings, with a 10% additional tax, apart from the existing additional taxes applicable for filing updated return. This amendment is proposed to reduce the litigations. In the re-assessment proceedings, the assessing officer can only refer to updated returns.

Also, with effect from 01st March 2026, updated return can be filed for reduction of losses.

What is ITR-U?

- The provisions of ITR-U are covered under section 139(8A) of the Income Tax Act.

- ITR-U can be filed even if the taxpayer has missed the due date of original return, revised return and belated returns.

- It allows taxpayers to update their ITRs by correcting errors or omissions.

- It can be filed within 4 years from the end of relevant assessment year.

- For example, if you filed an ITR for AY 2025-26 and missed the revised/belated return filing window, you can file an ITR-U after the end of the assessment year, i.e. 31 March 2026 but within four years from there, i.e. 31 March 2030.

Who can File ITR-U under Section 139(8A)?

Any person who has made an error or omitted certain income details in any of the following returns is eligible to file an updated return:

- Original return of income, or

- Belated return, or

- Revised return

An Updated Return can be filed in the following cases:

- Did not file the return. Missed return filing deadline and the belated return deadline

- Income is not declared correctly

- Chose wrong head of income

- Paid tax at the wrong rate

- To reduce the carried forward loss

- To reduce the unabsorbed depreciation

- To reduce the tax credit u/s 115JB/115JC

A taxpayer can file only one updated return for each assessment year(AY).

Who is Not Eligible to File ITR-U u/s 139(8A)?

ITR-U cannot be filed in the following cases:

- Updated return is already filed.

- For filing nil return/loss return.

- For claiming/enhancing the refund amount.

- When updated return results in lower tax liability

- Search proceeding u/s 132 has been initiated against you

- A survey is conducted u/s 133A

- Books, documents or assets are seized or called for by the Income Tax authorities u/s 132A.

- If assessment/reassessment/revision/re-computation is pending or completed.

Note: If the loss or any part thereof carried forward or unabsorbed depreciation carried forward or tax credit carried forward is to be reduced for any subsequent previous year as a result of furnishing an updated return of income for a previous year, an updated return is required to be furnished for each of the affected subsequent years as well.

ITR-U Form Download

What is the Time Limit to File ITR-U?

The time limit for filing ITR-U is 48 months from the end of the relevant assessment year. You should note that for the AY 2025-26, the last date to file ITR-U is 31st March 2030. However, for the return that your file for AY 2024-25, the last date to file ITR-U is 31st March 2029.

The table for the previous four years have been shown in the table;

| Financial & Assessment Year | Last date to file ITR-U |

| FY 20-21 (AY 2021-22) | 31st March 2026 |

| FY 21-22 (AY 2022-23) | 31st March 2027 |

| FY 22-23 (AY 2023-24) | 31st March 2028 |

| FY 23-24 (AY 2024-25) | 31st March 2029 |

| FY 24-25 (AY 2025-26) | 31st March 2030 |

Should you Pay Additional Tax when Filing ITR-U?

- The deadline for taxpayers to file updated income tax returns has been extended from 2 years to 4 years from the end of the relevant assessment year.

- This will make compliance with tax provisions voluntary by giving more time for tax filing and rectifying tax returns with ease, consequently ensuring a clean and efficient taxing process.

- The additional tax has to be paid while filing the ITR-U. The amount of additional tax that has to be paid is as follows:

| ITR-U Filed Within | Additional Tax |

| 12 months from the end of the relevant AY | 25% of additional tax (tax + interest ) |

| 24 months from the end of the relevant AY | 50% of additional tax (tax + interest ) |

| 36 months from the end of the relevant AY | 60% of additional tax (tax + interest ) |

| 48 months from the end of the relevant AY | 70% of additional tax (tax + interest ) |

How to File Form ITR-U?

As per the Income tax rules, the updated return (ITR-U) has to be furnished along with an updated version of the applicable ITR form (ITR 1 – 7).

There are two parts to the form- Part A & B. Follow the below-mentioned instructions for filling up the form:

Part A: General information

A1 PAN

A2 Name

A3 Aadhhar Card Number

A4 Assessment Year

A5 Select yes if you filed the return previously for the assessment year.

A6 If yes, look at the ITR acknowledgement (“Filed u/s”) to figure out if it was filed u/s 139(1) or others

A7 Next, enter the form no., acknowledgement no. or receipt no. and date of filing the original return (DD/MM/YYYY). You will find all these details in the ITR acknowledgement.

A8 Check the eligibility conditions mentioned above and select the appropriate option.

A9 Select the ITR form number.

A10 You must now select at least one reason for updating the ITR-U. (multiple selections are allowed)

A11 Depending on the months elapsed, choose whether return is filed within 12 to 48 months.

A12 In case the updated return reduces the balance of carried forward loss or unabsorbed depreciation, enter the assessment year in which they were affected because of the updated return. Also, mention if a revised or updated return was filed earlier.

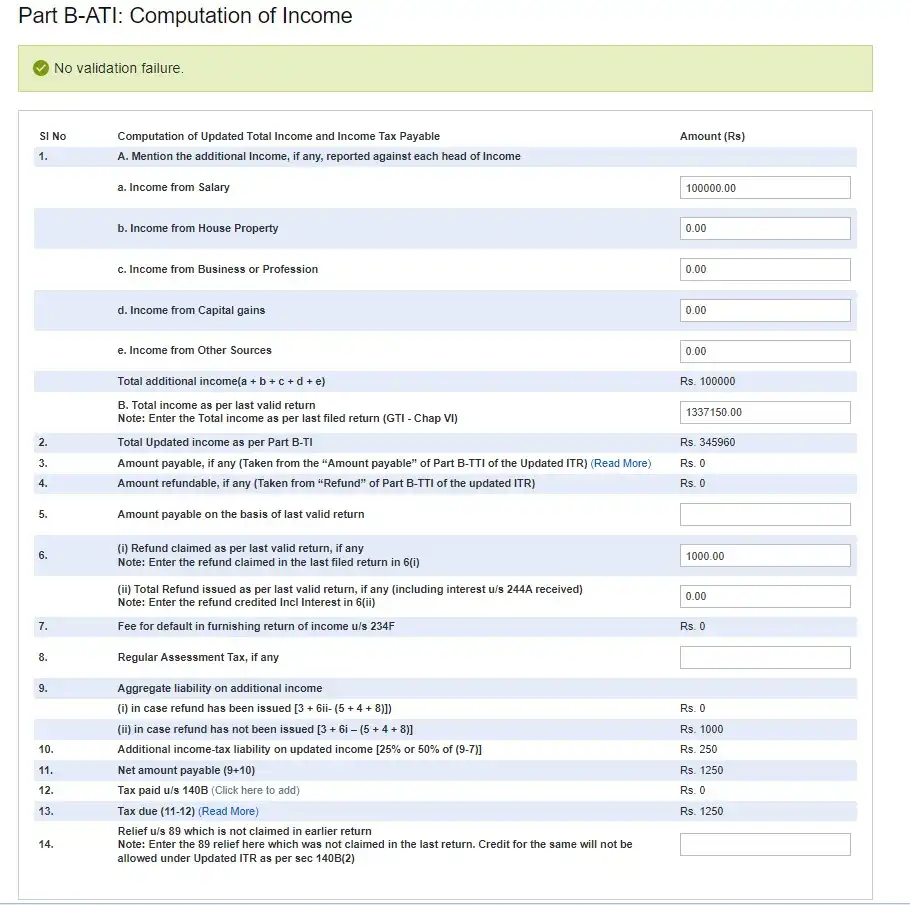

Part B: ATI Computation Of Total Updated Income And Tax Payable

- Enter the additional income figures in each head of Income. A detailed break-up of each head is not required.

- Enter the income declared as per the last return

- Enter the Total Income amount. You can find this from ‘Part B-TI’ of the ITR form (1-7) filled by you.

- The amount payable, if any (You can take it from the – ‘Amount payable’ section of Part B-TT of the ITR form)

- Amount refundable, if any (You can take it from the – ‘Refund’ section of Part B-TT of the ITR form)

- Enter the tax payable amount as per the last return.

- However, if a refund was claimed in the last return, then enter the claim amount or If you have received the refund, enter the amount of refund received, including the interest amount on such refund.

- If the last return was filed late, enter the fee paid for late filing.

- Enter the regular assessment tax paid in the last return

- Aggregate liability on the additional income

- Additional tax liability on updated income [25% or 50% of (9-7)]

- Net tax amount payable (9+10)

- Tax already paid u/s 140B: If updated ITR results in a tax payable amount, the same must be paid as a Self-Assessment Tax. Make the payment and enter the challan details.

How to Verify ITR-U?

ITR-U can be verified in the following manner:

- Aadhaar OTP

- Electronic Verification Code (EVC)

- Digital Signature Certificate (DSC)

- For tax audit cases - Only Digital Signature Certificate (DSC)

How to Compute the Tax Payable for an Updated Return (ITR-U)?

Your total income tax liability while filing ITR-U would be as under:

Total Income Tax Liability = Tax Payable + Interest + Late-filing fees + Additional Tax

Net Tax Liability = Total Income Tax Liability (as above) – TDS/TCS/Advance Tax/Tax Relief

| Sr. No. | Particulars | Match figure from | Amount (in Rs) |

| A | Tax payable on additional income as per modified ITR (as per Part B-TTI of modified ITR) | Modified ITR (submitted along with ITR-U) | XXXX |

| B | Interest levied, if any, on additional income under Section 234A/234B/234C (as per Part B-TTI of modified ITR) | Modified ITR (submitted along with ITR-U) | XXXX |

| C | Late fee, if any, under Section 234F (as per Part B-TTI of modified ITR) | Modified ITR (submitted along with ITR-U) | XXXX |

| D | Taxes paid or relief TDS/TCS/Advance Tax/regular assessment tax/Relief | XXXX | |

| E | Aggregate tax liability on additional income | A+B+C-D | XXXX |

| F | Additional tax 25% or 50% or 60% or 70% on (E-C) | XXXX | |

| G | Net Amount Payable | F+G | XXXX |

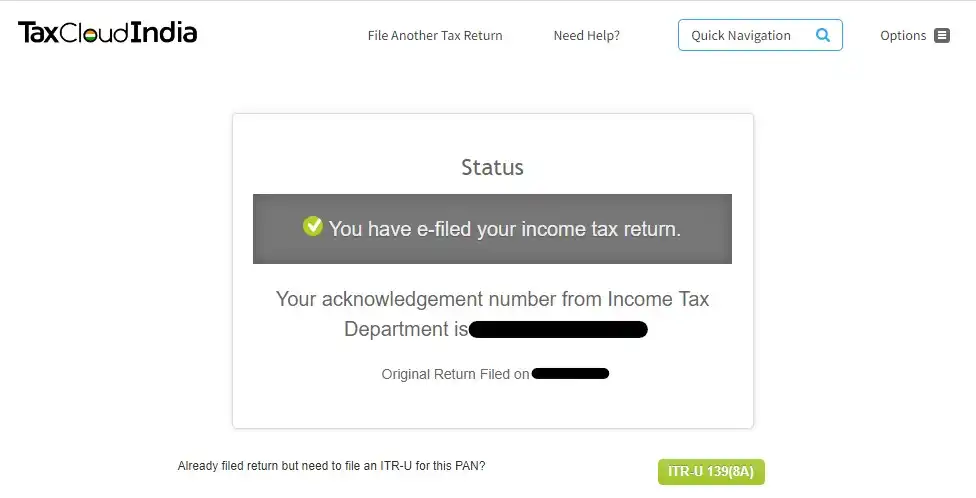

Try the fastest Tax Filing Software for ITR-U: TaxCloudIndia.

How to Prepare ITR-U on TaxCloudIndia?

Before we dive into the step-by-step guide, here’s a quick overview of the entire process:

To prepare an ITR-U on TaxCloudIndia, follow the below-mentioned steps:

Step 1: Select the Client/Add the Client

If you have used TaxCloud for filing the ITR, select the return from the home page and then click on the ‘work on client’ button.

If you have filed the ITR through any other platform, click on the ‘import client button’ and upload the JSON file used for filing the ITR. This will recreate the return and help autofill the ITR-U on TaxCloud.

Step 2: Enable ITR-U

Once the return is selected or recreated, please ensure the return is marked as ‘Filed’. If not, go to the ‘Advanced Options’ and mark the return as ‘filed’.

On the next screen, you will see the status message. Click the ‘ITR-U 139(8A)’ button at the bottom right to enable ITR-U.

If your client has not filed an ITR for the selected period, go to the ‘Tax Filing’ tab > Click on the ‘Special Options’ tab > ITR-U Enabled.

Step 3: Instructions for filling out the ITR-U Schedules

- General Information- All your general information will be pre-filled based on the return selected or recreated by you.

- Follow the instructions on ‘How to file Form ITR-U?’ mentioned above. However, majority of the fields will be pre-filled for you. You won’t need to look up the numbers in the ITR acknowledgement.

Related Articles

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption