Integration

across all ERPs Integration across all ERPs

Index

B2B vs B2C e-Invoicing: Key Differences Explained

After successful implementation of e-Invoicing in the B2B sector in a phased manner, the GST Council, in its 54th meeting held on 9th September 2024, recommended a pilot programme on e-invoicing for the B2C sector. The intention behind recommending e-invoicing for B2C transactions is to reduce tax evasion and improve compliance. B2C e-invoicing is essential since it ensures businesses record all B2C transactions accurately and report them in the GST returns to duly cover these under the tax net.

This article discusses the difference between the existing structure of B2B e-Invoicing and B2C e-invoicing in GST and other important facts to make you better prepared when B2C e-Invoicing starts to roll out.

What is B2B e-Invoicing?

B2B or Business-to-Business e-Invoicing is the practice of electronic authentication of an invoice along with a few supportive documents by GSTN for further use in the GST portal.

Requirements of B2B e-Invoice

For GST compliance, e-Invoicing is mandatory for any business with a yearly aggregate turnover of more than ₹5 crore. For mandatory e-Invoicing, companies need to submit invoice-specific information, along with GSTIN details of the seller and the buyer, to the GST portal or an approved invoice registration portal (IRP) for authentication.

After authentication, the portal generates the e-Invoice electronically, which a seller finally issues to the other parties involved in the transaction.

- e-Invoice must contain GSTIN, UIN, name and address of the purchaser (customer)

- The business customer has to be GST-registered as a business to claim input tax credits.

- The e-Invoice data must be submitted in GST return for intra and interstate sales.

Considering the benefits of B2B e-Invoicing, companies and individual GSTIN holders with less than threshold aggregate turnover can also voluntarily enable B2B e-Invoicing through their login in the GST portal.

What is B2C E-Invoicing?

Currently, businesses are not required to issue e-invoices to end consumers except to generate and print a dynamic QR code for B2C invoices. Considering the expansion, B2C e-invoicing will imply the electronic invoicing requirement under GST for certain taxpayers who make a taxable supply of goods and services to end-consumers and raise tax invoices.

Businesses that will raise such B2C GST invoices will be required to report these to the Invoice Registration Portal (IRP) authorised by the GST Network. In turn, their invoices will be verified and authenticated by the IRP (on behalf of the GSTN). Each e-invoice generated will get a unique Invoice Reference Number (IRN) and a QR code containing details of such authentication.

Requirements of B2C E-Invoice

Currently, there are no particular requirements set out by the government for B2C e-Invoicing. We can expect an update through a CBIC notification and circular in due course of time.

Comparison: Key differences between B2B and B2C e-Invoicing

Particulars | B2B e-Invoicing | B2C e-Invoicing |

| Meaning | It is about issuing, receiving and processing tax invoices in electronic or digital formats for sales transactions between two registered taxpayers. Such invoices are authenticated by the GSTN. | It concerns issuing, receiving, and processing tax invoices in electronic or digital formats for transactions between a merchant and an individual consumer or an unregistered person. Such invoices are authenticated by the GSTN. |

| Applicability | B2B e-Invoicing for GST is mandatory for companies with aggregate turnover exceeding ₹5 crore in any preceding financial year. | The GST Council and GSTN are planning a pilot programme on B2C e-invoicing with voluntary participant users. Based on the pilot programme's outcome, the Council will decide when and how to mandate B2C e-invoicing. |

| Voluntary e-Invoicing | The GST portal allows voluntary e-invoicing for B2B sales. To use this facility, a company or business needs to enable the 'voluntary e-Invoicing' feature inside the portal. | In the 54th GST Council Meeting, the Council recommended conducting a pilot e-Invoicing programme for B2C sales. |

| Impact on buyers | B2B e-invoices are essential for claiming input tax credit by registered users. | B2C e-invoicing is expected to bring greater transparency to consumer-facing businesses. |

| Reporting | Invoices are reported invoice-wise, and the GST portal auto-populates GSTR-1 with invoice data.

| Currently, invoices are reported at the summary level, mainly for B2CS and invoice-wise for B2CL. However, with e-invoicing being introduced to B2C, the B2C e-invoices will most likely be auto-populated to GSTR-1. |

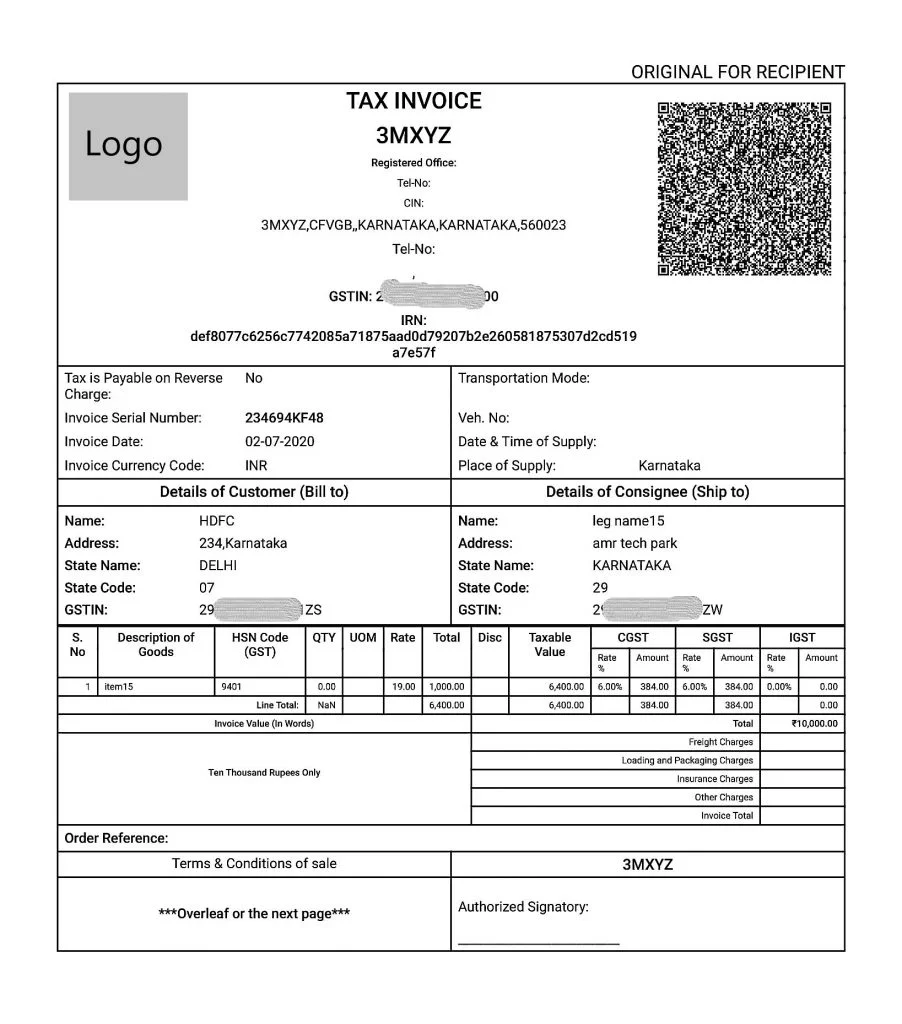

Examples of B2B and B2C E-Invoicing

An example of B2B e-Invoice for GST purpose

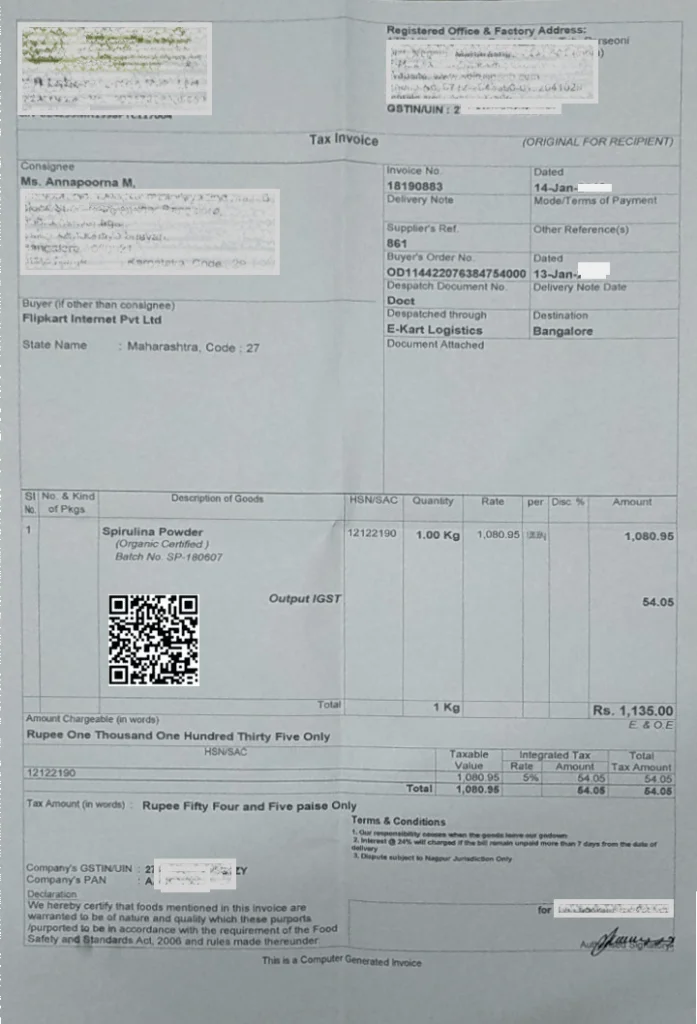

An example of B2C E-Invoicing

The B2C e-Invoicing is yet to get implemented. However, the dynamic QR code requirement for B2C invoices already exists. Below is a sample B2C invoice with the dynamic QR code.

The Government of India is considering making e-invoicing mandatory for all taxable transactions within a few years. This will help achieve greater automation of the GST collection, transfer, and compliance processes and remove hassles in GST return submission. Digitising the sales process will also allow companies to leverage data science technologies for holistic business intelligence.

Frequently Asked Questions

What is the main difference between B2B and B2C e-invoicing?

How to identify B2B and B2C in GST?

What is the GST limit for B2B and B2C invoices?

What is the difference between B2B and B2C payments?

How do I transfer a B2C invoice to B2B?

Are tax reporting and compliance different for B2B and B2C e-invoicing?

What are the latest updates on e-invoicing regulations in India?

Products

Resources & Guides

GST Resources

ITR Resources

Mutual Fund Resources

Tools

TRENDING MUTUAL FUNDS

ICICI Prudential Technology Fund Direct Plan Growth

Tata Digital India Fund Direct Growth

Axis Bluechip Fund Growth

ICICI Prudential Technology Fund Growth

Aditya Birla Sun Life Tax Relief 96 Growth

Aditya Birla Sun Life Digital India Fund Direct Plan Growth

Quant Tax Plan Growth Option Direct Plan

SBI Technology Opportunities Fund Direct Growth

Axis Long Term Equity Fund Growth

TOP AMCS

STOCK MARKETS

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption