|

What is a Debit Note in GST: Meaning, Process, Format & Time Limit

What is a Debit Note in GST: Meaning, Process, Format & Time Limit

Debit notes or debit memos refer to a document commonly used in Business-to-Business (B2B) transactions. It helps the buyer keep track of his debt obligations towards the supplier for goods or services provided. It also helps suppliers rectify undervalued invoices.

Key Takeaways

- Debit notes rectify undervalued invoices by suppliers or notify sellers of damaged/defective goods by buyers, acting as supplementary documents in B2B transactions.

- Under GST Section 34(3), suppliers issue debit notes when tax invoice value/tax is less than actual; details reported in GSTR-1, visible in recipient's GSTR-2A/2B for GSTR-3B.

- Issue by Sep 30 of next FY or GSTR-9 date; post-amendment, ITC timeline ties to debit note date, not original invoice.

- No fixed format, but include header, date, GSTINs, serial number, invoice reference, HSN/SAC, values/taxes, and digital signature; maintain in debit note book.

What is a Debit Note?

A debit note is a commercial document that usually contains information with regard to any adjustments to be made to a particular invoice amount. Debit notes are also referred to as supplementary invoices.

Process of Issuing a Debit Note

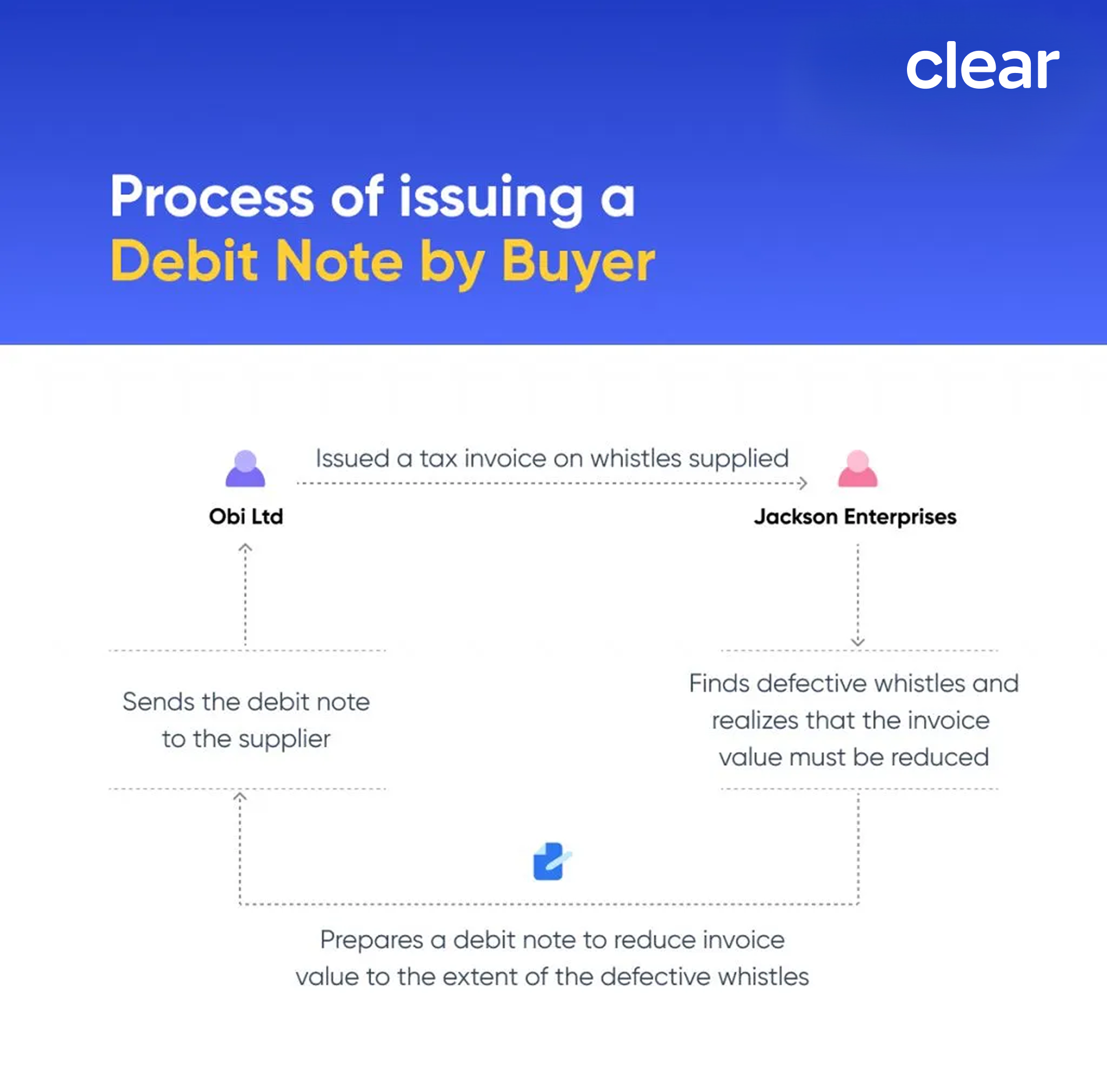

Scenario 1: By a Buyer

Jackson Enterprises makes a purchase on credit from Obi Ltd. for 10,000 whistles at the rate of Rs.15 per whistle. Obi make the delivery for the order, and an invoice for the same is given to Jackson Enterprises at the time of delivery. Upon inspection, it is found that 430 whistles are damaged, 200 are defective.

Jackson Enterprises creates a debit note to be sent to Obi Ltd. along with the return of the 630 whistles. The debit note and the return of the whistles indicate that Obi Ltd. will have to debit the amount due from Jackson Enterprises by Rs.9,450 (630 whistles x Rs.15).

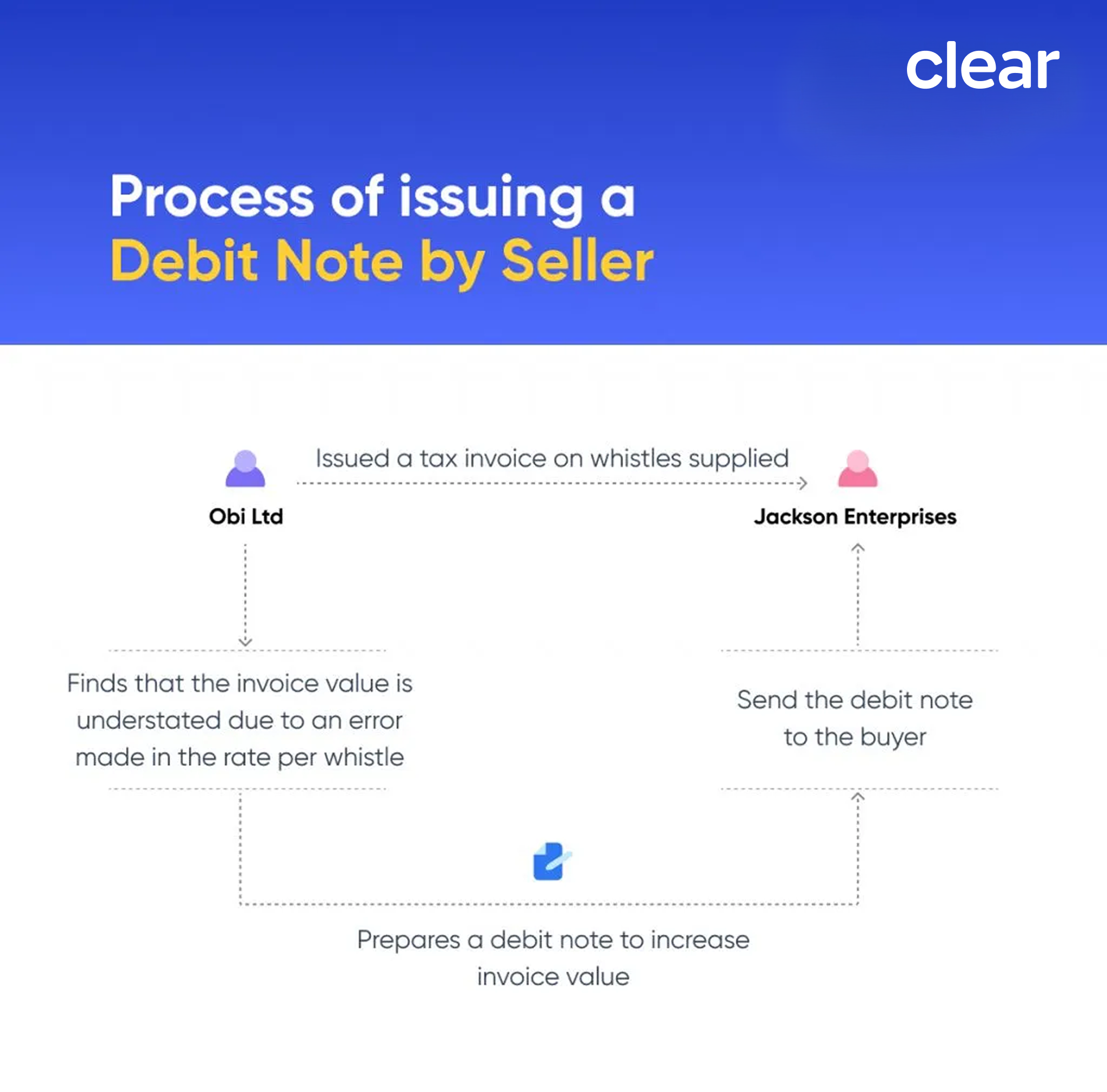

Scenario 2: By a Seller

Jackson Enterprises makes a purchase on credit from Obi Ltd. for 10,000 whistles at the rate of Rs.15 per whistle. Obi makes the delivery. The seller issues an invoice for the order, given to Jackson Enterprises upon delivery. However, Obi Ltd. realises that the rate per whistle is Rs.16 in the invoice submitted to Jackson Enterprises, thus understating the invoice by Rs.10,000.

Obi Ltd. then creates a debit note to be sent to Jackson Enterprises, thus rectifying the error mentioned above.

Reasons for Issue of a Debit Note

A debit note is issued by a buyer to a seller for the following reasons:-

- Amount stated in the invoice is incorrect

- Receipt of defective/damaged goods

- Overstatement of the value of the invoice

- Cancellation of the purchase of product/service

- When goods received do not measure up to the buyer’s expected standards

A debit note is issued by a seller to a buyer for the following reasons:-

- Amount receivable from the buyer increases

- Understatement of the value of the invoice

- Addition made to the order of product/service

Debit Note Book or Ledger

- A separate book is maintained called a debit note book. Two copies of the debit notes are maintained, one of which will be given to the supplier. The other one remains in the debit note book and serves as a record.

- When the credit note is received from the supplier, the same is marked off against the debit note in the debit note book, thus enabling a system of efficient tracking and balancing.

- Since one copy of the debit note is given to the supplier, the supplier may use it as a reference point while issuing the credit note.

Importance of Debit Note under the GST Law

As per Section 34(3) of the CGST Act 2017, a supplier of goods and services issues one or more debit notes when;

- One or more tax invoices have been issued for supply of any goods or services or both

And,

- The taxable value or tax charged in that tax invoice is found to be less than the taxable value or tax payable in respect of such supply

One of the most important roles that a debit note plays under GST is that it forms part of the details with respect to GSTR-1, the month in which the supply of goods was made. The same details form part of Form GSTR-2A and GSTR-2B for the recipient. Once the verification is done, the recipient may approve of it and submit it as part of their GSTR-3B.

Earlier, when reporting a credit note or a debit note, the original invoice number was mandatorily required to be quoted on the GSTN portal in Form GSTR-1 and Form GSTR-6.

However, the amendment pertaining to the delinking of debit notes from their original invoice resulted in the following:-

- To identify the supply type (intrastate or interstate), the place of supply can be provided for a particular debit note or a credit note.

- Where a debit note or credit note is issued only for the difference in the tax rate, the value of the note can be shown as zero. Entering the tax amount will be sufficient.

The delinking amendment also affected the treatment of Input Tax Credit (ITC) with respect to debit notes. Before the amendment, the time limit for availing ITC was linked to the date of the invoice, not the date of issue of the debit note. However, post the amendment, the time limit for availing ITC is now computed as per the date of the debit note.

For instance, if an invoice was issued in March 2019, and debit note for the same was issued in October 2019, the last date for availing ITC would be the due date of Form GSTR-3B for October 2020, since the debit note was issued in the year 2019-2020.

Amendments to Debit Notes

Where an invoice issued by the supplier requires a certain revision or change to be made to it, the amendment to the same may be made on the GST portal. There are two cases with regard to amendments:

- Amendments to be made to debit/credit note issued to registered persons

The reporting requirements to be made in this case will have to be entered in ‘Table 9C – Amended Debit/Credit Notes (Registered)’ of the Form GSTR-1.

- Amendments to be made to debit/credit note issued to registered persons

The reporting requirements to be made in this case will have to be entered in ‘Table 9C – Amended Debit/Credit Notes (Unregistered)’ of the Form GSTR-1.

Time limit to Issue a Debit Note

In general, a debit note can be issued at any time. However, as per the GST laws, the debit note will need to be issued at the earliest of the following dates:-

- On or before 30th September in a financial year following the year in which the goods and/or services were supplied.

OR

- On or before the date on which the taxpayer files the GSTR-9 (Annual Return) for the financial year.

Failure to issue the debit note within the above stipulated time will increase tax liability, interest levy, and penalties.

Debit Note Format and Contents

There is no fixed format for a debit note prescribed by law. However, some fields must be mandatorily present:-

- Header description stating the document is a debit note

- Date of issue of debit note

- Name, address, contact details and GSTIN of the supplier

- Debit note the serial number

- Name, address, contact details and GSTIN of the recipient

- Invoice reference number against which debit note is issued

- Date of creation of supplementary invoice

- Description of the goods and HSN or SAC

- Value of taxable supply of goods or services, rate of tax, and the amount of tax

- Verification of the document in the form of a digital signature

Steps to Create a Debit Note

Suppliers follow these sequential steps to issue a compliant debit note for upward tax adjustments.

Gather details: Collect supplier name, address, GSTIN; recipient details (name, address, GSTIN if registered); original invoice number and date; reason (e.g., price increase).

Assign identifiers: Use a unique consecutive serial number (up to 16 characters, non-repeating in the financial year) and issuance date.

Specify transaction: Describe goods/services, quantity, HSN/SAC code, revised taxable value, tax rate (CGST/SGST/IGST), and tax amount debited.

Review and sign: Verify calculations, add signature or digital signature of authorized person, and reference the original tax invoice.

Distribute and report: Share copy with recipient, record in books, and report in GSTR-1

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption