|

Key Difference Between IFRS and IND AS

Businesses worldwide use specific standards to prepare and publish their financial reports to stakeholders. The two most important accounting standards in the context of Indian financial markets are IND AS and IFRS. This article explains them individually and clarifies their fundamental differences.

All you need to know about IND AS

The meaning

The full form of IND AS is the Indian Accounting Standards. By definition, an accounting standard is a set of,

- Principles

- Procedures

- Rules

Financial reports are like windows through which the outside world can peep inside a company’s accounts and balances and try to understand its financial health. This understanding is critical for so many stakeholders, such as investors, debtors, tax authorities, and regulators.

Businesses within a jurisdiction must follow the rules, principles, and procedures mentioned in an accounting standard for their financial accounting policies and practices.

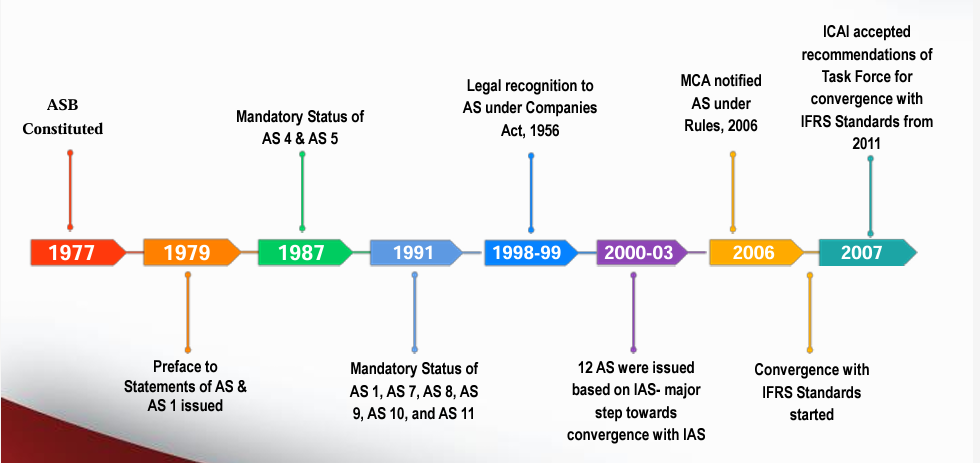

The Institute of Chartered Accountants Of India (ICAI) constituted the Accounting Standard Board (ASB) in 1977 to standardise financial reporting according to globally accepted rules and regulations. This board formulated and issued the Indian Accounting Standards.

Source - https://asb.icai.org/assets/ppt/asb_about_us.pdf

The guiding principles and the objectives behind the formulation of IND AS are:

- Streamlining accounting and reporting practices as per Indian economic realities and legal environment.

- Ensuring standardised practices for treatment and disclosure of significant financial transactions.

- Offering a uniform framework to maintain transparency in financial accounting.

- Maintaining a harmony between Indian accounting standards and globally accepted financial accounting and reporting standards.

Before the full-fledged adoption of IND AS, Indian companies followed the Indian Generally Acceptable Accounting Principles as an accounting standard for financial accounting and reporting purposes.

The applicability

From the beginning, the Ministry of Corporate Affairs has implemented IND AS in a phased manner. This has provided companies with sufficient time to arrange necessary infrastructure and training.

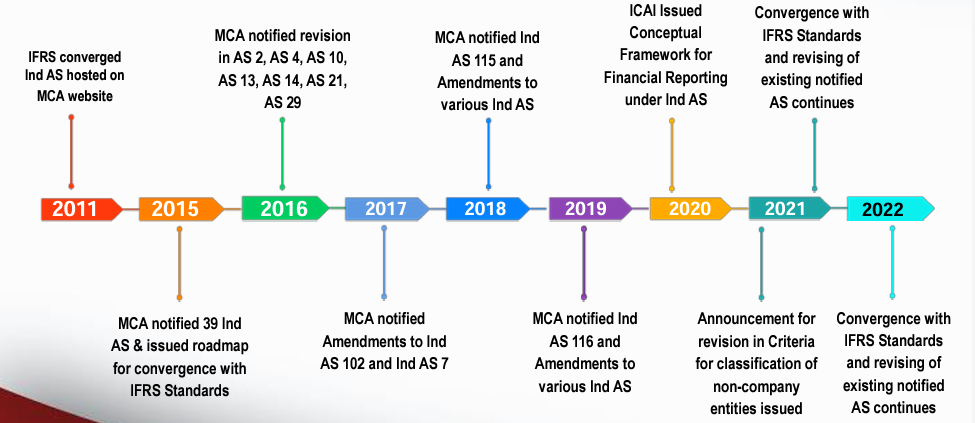

In 2015, the MCA made IND AS adoption mandatory for all listed companies and a few others from FY 2016-17. From 2018, the adoption of IND AS was further widened to:

- Every listed company, irrespective of turnover

- Non-listed companies with a net worth of more than or equal to Rs 500 crores.

- Non-banking financial companies (NBFCs) having a net worth of more than Rs 250 crores but less than Rs 500 crores.

Other than these companies, adopting IND AS is voluntary

At present, the applicability of IND AS can be of 2 types:

- Mandatory

- Voluntary

The importance

Besides mandatory applicability, adopting Indian Accounting Standards, or IND AS can also benefit voluntary adoptions. The adoption of IND AS is vital for various reasons.

- Legal compliance - As per the MCA, adopting IND AS is essential for complying with ICAI guidelines and financial accounting disclosure laws.

- Financial transparency - IND AS allows for the highest level of financial transparency for listed and non-listed companies.

- Global comparability - Financial reporting as per IND AS is highly comparable to international standards, like IFRS. It simplifies financial accounting and disclosure practices for Indian companies willing to reach out to global stakeholders.

- Accounting reliability - Financial accounting and reporting based on IND AS is well-recognised for their accuracy among stakeholders.

- Consistency across industries - IND AS accounting and reporting practices are consistently applicable across businesses and sectors in India.

All you need to know about IFRS

The meaning

IFRS stands for International Financial Reporting Standards. It has been adopted in over 168 jurisdictions, making it the most used accounting standard globally. Some major countries, (as listed below), and all EU countries, follow IFRS, which originated in the European Union. IFRS practices and principles also influence and guide the formulation of IND AS.

However, the USA and China have their own accounting standards.

The International Accounting Standards Board, or IASB, is the independent non-profit organisation responsible for developing and maintaining IFRS accounting standards.

The applicability

IFRS is applicable in 168 jurisdictions across the world, including major countries, like:

- Australia

- Russia

- Singapore

- Taiwan

- South Korea

- Turkey

- Brazil

- Canada

- The EU

- Gulf countries

- Hong Kong

- India

- Israel

- Malaysia

- Pakistan

- Philippians

- Malaysia

- Pakistan

The importance

The global acceptability of the IFRS proves the advantages it offers to companies and regulators across jurisdictions.

- More transparency and comparability - Adopting IFRS allows companies with international operations to have a transparent and comparative understanding of their businesses across geographies.

- Improved access to the global flow of capital - Companies practising IFRS in financial accounting and disclosure enjoy the confidence of the global investor community, which increases access to investments.

- Reduced cost for regulators and companies - Developing and maintenance of accounting standards can be costly. So, by providing reliable accounting standards, the IFRS has reduced the cost for regulators across countries. Companies with international operations also do not need to comply with separate standards for different jurisdictions. It saves them from many complexities and unnecessary expenditures.

- Effective corporate governance - IFRS has also improved global corporate governance practices.

Differences between IND AS and IFRS

| IND AS | IFRS | |

| Issuing Body | Institute of Chartered Accountants of India (ICAI) | International Accounting Standards Board (IASB) |

| Applicability | Mandatory in India for all 1) listed companies, 2) unlisted companies with net worth above Rs 500 crore, and 3) NBFCs with net worth between Rs 250 crore to Rs 500 crore. | Required for domestic public companies to adopt IFRS in the EU and other jurisdictions globally in 168 countries. |

| Basis | Mostly developed based on IFRS practices and principles. | Set of accounting standards practised in G20 countries |

| Financial statement components | It comprises of the following:

| It comprises of the following:

|

Examples of IND AS and IFRS

Suppose a company XYZ provides annual AC maintenance services to its customers. Services under a contractual agreement get delivered throughout the year, but customers pay for the service upfront.

As per IND AS 115, such a company can treat customers’ payment as revenue only after the completion of the year.

However, IFRS 15 requires such a company to recognise customers’ payment as revenue over the time of contractual service period.

Accounting standards are becoming increasingly essential for establishing a framework of comparability, consistency, and confidence in financial accounting and reporting practices. Voluntary adaptation of such globally accepted standards will help startups and small companies access reliable sources of capital and investors make more informed decisions.

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption