Call Now

Call Now

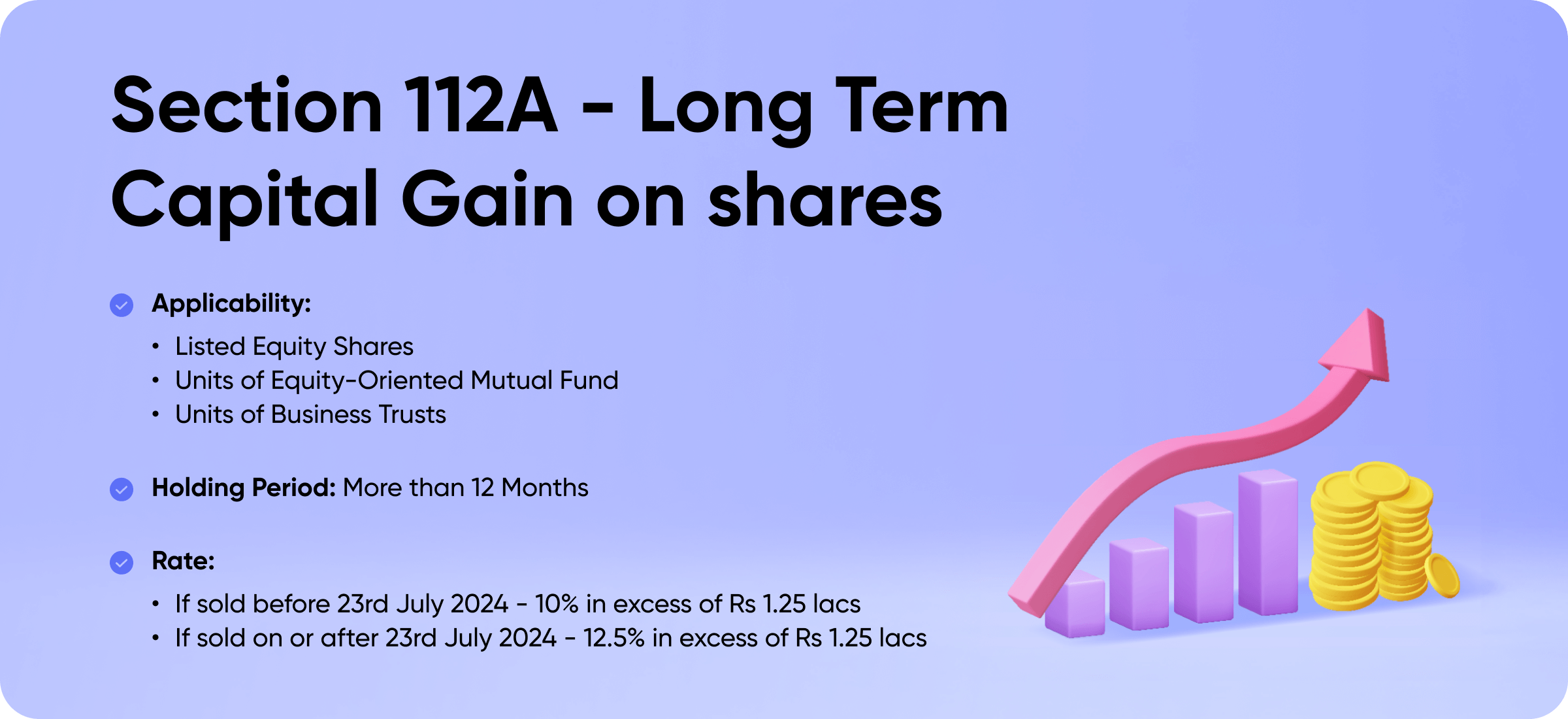

Section 112A of Income Tax Act - Long Term Capital Gains on Shares

Long-term capital gains (LTCG) on shares arise when listed equity shares, equity-oriented mutual funds, or business trust units held for over 12 months are sold at a profit. Governed by Section 112A of the Income Tax Act, LTCG on shares is taxed at 12.5%, with an exemption of up to Rs. 1.25 lakh. This guide covers LTCG tax on shares, calculation, exemptions, and applicable tax rules.

What is Section 112A?

Section 112A of the Income Tax Act deals with Long Term Capital Gains on sale of listed equity shares, equity oriented funds, and units of business trust. 12.5% of tax is levied on the capital gains. Also, it provides an exemption of Rs. 1.25 lakh on long term capital gains (LTCG) from equity investments. However, taxpayers need to understand that the rebate under Section 87A is not allowed on tax payable under Section 112A.

Long Term Capital Gains Tax Rate

The LTCG tax rate is 12.5% on capital gains from sale of listed equity shares, units of equity oriented mutual funds or units of business trusts held for more than 12 months under Section 112A. However, taxpayers are allowed an exemption of up to Rs. 1.25 lakh.

Applicability of Section 112A

To avail the beneficial rates and exemptions under section 112A, the following conditions must be met:

- Securities Transaction Tax (STT) must be paid on both purchase and sale of equity shares.

- For units of equity-oriented mutual funds or business trusts, STT must be paid at the time of sale.

- The securities must qualify as long-term capital assets.

- The securities should be held for more than 12 months.

- No deduction under Chapter VI-A can be claimed against such LTCG.

How to Calculate Capital Gains Under Section 112A?

Step 1: Gather all the capital gain transactions made during the year. You can refer all your broker statements, and cross verify with AIS.

Step 2: Classify the gains into two categories: Sale made before 23rd July 2024, and sales on or after 23rd July 2024.

Step 3: Calculate total sales consideration for both of the categories separately, and reduce the purchase cost respectively.

Step 4: You will arrive at the capital gains for both of the categories. Add the up, and reduce Rs. 1.25 lakhs from the total capital gains. You will arrive at the taxable capital gains.

What is the Grandfathering Clause in Section 112A?

The grandfathering clause under Section 112A protects gains made before 31st January 2018 from taxation. It ensures that only the gains accrued after 31st January 2018 are taxed. For listed equity shares, equity mutual funds, and units of business trusts, the cost of acquisition is taken as the higher of the actual purchase price or the fair market value as on 31st January 2018, but not exceeding the sale price. This helps investors avoid tax on past appreciation before the LTCG tax was introduced.

The Cost Of Acquisition as per grandfathering clause will be calculated as follows:

- Value I - Fair Market Value as of 31st Jan 2018 or the Actual Selling Price, whichever is lower

- Value II - Value I or Actual Purchase Price, whichever is higher

Value II shall be the Cost of Acquisition (as per grandfathering rule)

Long Term Capital Gain (LTCG) = Sales Value – Cost of Acquisition (as per grandfathering rule) – Transfer Expenses

Tax Liability = 12.5% (LTCG – Rs 1.25 lakh)

Illustration for LTCG on Shares as per Grandfathering Rule

Let us understand with an example

Mr Udit made a lump-sum investment of Rs. 20 lakh in shares of a listed company in June 2005.

FMV on January 31, 2018, is Rs. 40 lakh. Udit redeems his entire investment in May 2019 for Rs.43 lakh netting a gain of Rs. 23 lakh. However, due to the grandfathering clause, Udit’s taxable gain would be only Rs. 3 lakh.

Udit had made another one-shot investment of Rs. 15 lakh in shares of another listed company in February 2016. The FMV of the investment on January 31, 2018, was Rs. 4 lakh, and he further sold all these shares in June 2019 for a sum of Rs. 10 lakhs. In this transaction, Rahul incurred a loss of Rs. 5 lakh calculated for tax purposes as per the above-mentioned formula.

| A | B | C | D | E | F | |

| Udit’s Investment Portfolio | Sale price | Cost | FMV on 31st Jan | Value I Lower of A and C | Value II Cost of acquisition – Higher of B and D | Capital gain (A- E) |

| 1 | 43 Lacs | 20 Lacs | 40 Lacs | 40 Lacs | 40 Lacs | 3 Lacs |

| 2 | 10 Lacs | 15 Lacs | 4 Lacs | 4 Lacs | 15 Lacs | (5 Lacs) |

Exemption on LTCG on Listed Shares

Under Section 112A, long-term capital gains (LTCG) on equity shares sold are taxed at 12.5%. An exemption of Rs. 1.25 lakh is available, meaning only LTCG exceeding Rs. 1.25 lakh is taxable at the applicable rate.

The CBDT has clarified that this exemption is to be reduced from the total gains while calculating tax, not from the taxable income directly. You can use the ClearTax LTCG calculator to compute your taxes accurately, factoring in these exemptions and rates.

Example: Mr. A has an LTCG on listed shares of Rs. 3,00,000. Calculate the tax liability on the same.

- Sold on 1st March 2024 - Tax liability on listed shares = (3,00,000 - 1,00,000) * 10% = Rs. 20,000.

- Sold on 1st July 2024 - Tax liability on listed shares = (3,00,000 - 1,25,000) * 10% = Rs. 17,500.

- Sold on 1st August 2024 - Tax liability on listed shares = (3,00,000 - 1,25,000) * 12.5% = Rs. 21,875

LTCG on Transfer of Bonus and Rights Shares acquired on or before 31 January 2018

The LTCG for these shares shall be calculated by considering the FMV on 31st January 2018 as the cost of acquisition of such shares, thereby exempting gains until 31st January 2018 from tax.

Eg: You have Reliance shares purchased on 1st April 2016 and issued bonus shares as on 1st April 2017. Now if such bonus shares are sold after 31st Jan 2018, then FMV as of 31st Jan 2018 will be considered as the Cost of acquisition of such shares.

Set-off of Long-term Capital Loss with Long-term Capital Gain

The loss on the sale of long-term listed equity shares or equity-related instruments is a long-term capital loss.

Please note that long-term loss on capital gains can be set off only against long-term capital gain. In a situation of an investor has incurred losses from some securities and profits from other securities, then the same can be set off against each other.

Carry Forward of Long-Term Capital Losses on Sale of Shares

Long-term capital losses from the sale of shares can only be set off against long-term capital gains. Unlike short-term capital losses, which can be adjusted against both short-term and long-term capital gains, long-term losses cannot be set off against short-term gains.

If these losses are not fully set off in the same financial year, they can be carried forward for up to eight assessment years, but they must be adjusted only against long-term capital gains in future years.

Fair Market Value

- The Fair Market Value (FMV) of a listed security is the highest price quoted on a recognized stock market.

- If the security was not traded on 31 January 2018, the FMV is the highest price quoted on a date immediately before 31 January 2018 when the security was traded on a recognised stock exchange.

- In the case of unlisted units on January 31, 2018, the net asset value of the units on that date.

- The FMV of an equity share listed after January 31 2018, or acquired through a merger or other transfer under Section 47 will be: Purchase price x Cost inflation index for fiscal year 2017-18 / Cost inflation index for the year of purchase or fiscal year 2001-02.

Reconciliation of Capital Gain Statement vs AIS

As part of its digital initiative, the Income tax department has started receiving the details of the sale of your shares directly from depositories like CDSL and NSDL. Such data is reflected in your AIS - Annual Information Statement.

Thus, it is important that you reconcile the capital gains statement that you have with the data available in AIS before you file your ITR. Any Mismatch in ITR and AIS will result in a notice from the Income tax department

Rebate under 87A

The rebate under Section 87A of the Income Tax Act is not applicable to Long-Term Capital Gains (LTCG) taxed under Section 112A.

How to Minimise your LTCG tax?

Once long-term capital gain crosses the exemption limit for the year, the amount in excess of the exemption limit is taxable at the rate of 12.5%. But there is a smart way by which you can minimise your tax liability legally. And, this method of minimising tax liability is known as tax harvesting. Tax harvesting is of two types:

- Tax Gain Harvesting

- Tax Loss Harvesting

What is Tax Gain harvesting?

This is a tax strategy to optimise taxable gain. Here, the assessee sells the appreciated shares/mutual funds to book a capital gain up to the exemption limit. He/she then reinvests the redeemed amount in the market to benefit from market exposure while managing the taxable income.

What is Tax loss harvesting?

Tax loss harvesting is a strategy to minimise tax liability by offsetting the capital gains with other loss-making stocks.

Some points to take care of before following Tax Harvesting

- Don’t do intraday transactions

- Do a complete technical analysis of the stock before going for tax harvesting.

- Also, keep track of corporate actions like the payment of dividends before selling stocks.

- Always consult a financial advisor because it can also lead to severe losses.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption