Call Now

Call Now

NRI Taxation in India (2026): Slabs, Rules, ITR Forms & Capital Gains

NRI status under the Income-tax Act, 1961 classifies Indians abroad as Resident, NRI, or RNOR based on days spent in India. Residents are taxed on global income, while NRIs are taxed only on income earned or received in India, making residential status crucial for taxation and exemptions.

Key Takeaways

- NRIs and RNORs are taxed only on income earned or received in India, while Residents are taxed on global income

- You are resident if you stay ≥182 days in India in a year, or 365 days in the past 4 years + 60/120 days in the current year.

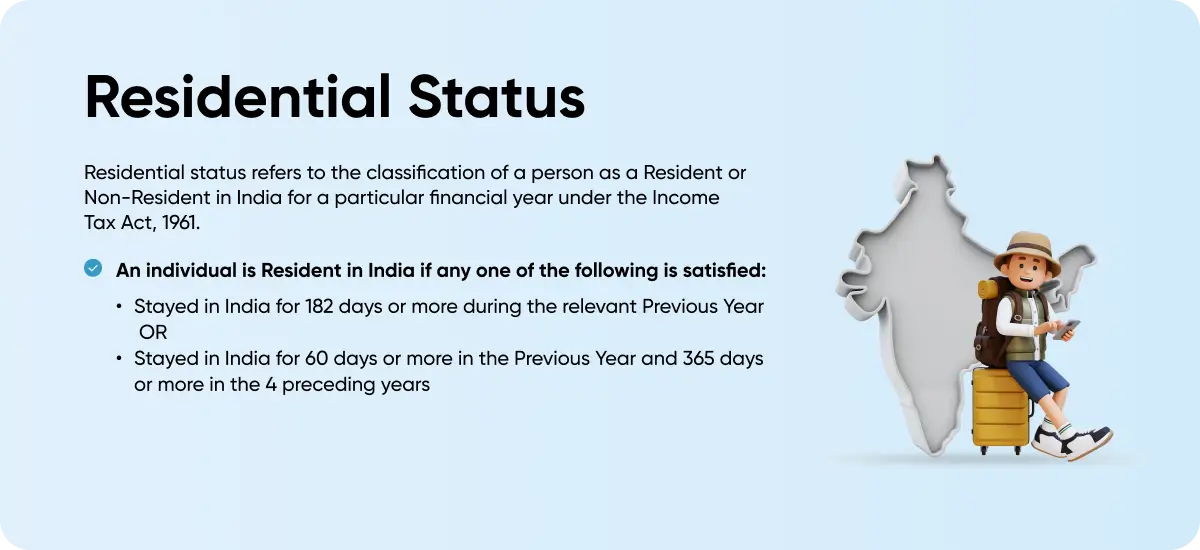

Who is a Resident in India?

A person would be a Resident of India for income tax purposes if-

- He/she is in India for 182 days or more during the financial year.

OR

- If he/she is in India for at least 365 days during the 4 years preceding that year AND at least 60 days in the relevant financial year.

Note: These days may be a single visit or counted over many visits to India.

Residential Status of Indian Citizens Leaving India for Employment

In case you are an Indian citizen, and you leave India for employment outside of India, or as a member of the crew on an Indian ship, your status will be a Non-Resident Indian (NRI) if you stay in India in the previous year for less than 182 days. Thus, if you are an Indian citizen and you live outside India for 182 days or above, you will be an NRI.

Residential Status of Indian Citizen or a Person of Indian Origin

In case of a citizen of India or a person of Indian Origin, who is outside India and has come on a visit to India during the previous year, where total income, other than income from foreign sources, exceeds Rs. 15 lakh, such person would be a RESIDENT of India for income tax purposes if

- He/she is in India for 182 days or more during the financial year.

OR

- If he/she is in India for at least 365 days during the 4 years preceding that year AND at least 120 days in the previous year.

Deemed Resident

Irrespective of the conditions listed above for being a resident, there is also a concept of deemed resident. An individual who is a citizen of India and has a total income (from other than foreign sources) exceeding Rs. 15 lakhs during a financial year, then he shall be deemed to be a resident in India in that year if he is not a tax resident of any other country.

Who is a Non-Resident in India?

If you do not satisfy the condition laid out above for a person to be considered a resident in India - you will be considered a NON-RESIDENT INDIAN (NRI). Thus, if you stay in India for less than 182 days, you will be considered an NRI.

Understanding Residential Status for Taxation in India: Resident vs Non-Resident

To identify how much tax you need to pay in India, it is important to determine what your residential status is in India. Note that the residential status must be checked for every financial year.

Say, if you are non-resident for one year, for the next year, and thereafter you must check your status again if you’ve travelled or changed homes, etc. Your tax liability in India will be defined by this status. Before we understand who is a Non-Resident Indian, let us first look at who is a Resident Indian.

Rules Governing NRI Status

The two main laws that govern and prescribe the rules for NRIs in India are as follows:

- Income Tax Act - Governs the tax liabilities of NRIs

- Foreign Exchange and Management Act (FEMA) - Governs all transactions and investments, the opening of bank accounts, etc., of NRIs

The definition of NRI is different under these acts. In this article, we have covered the definition of NRIs under the Income Tax Act 1961.

Residential Status of Indian Citizens as Crew on Indian Ships

In the case of a citizen of India and a member of the crew of a ship, for calculating the period of stay in India, the days of stay in India for a person will not include the period between the start and end dates of their Continuous Discharge Certificate (CDC). The CDC must comply with the Merchant Shipping (CDC-cum-Seafarer's Identity) Rules, 2001, under the Merchant Shipping Act, 1958. It must be for a voyage starting from an Indian port and ending at a foreign port, or vice versa. (Notification No. 70/2015/F.No.142/12/2015-TPL).

Such crew is considered as a Non-Resident Indian (NRI) for income tax purposes when they have spent less than 182 days in India. While calculating this stay of 182 days, the entire period mentioned in the Continuous Discharge Document shall be excluded even though the ship may have been on Indian coastal waters in its journey.

The number of days outside India of Indian crew working on such Indian ships gets counted only from the date when the Indian ship crosses the coastal boundaries of India. This increase in days is also applicable to you if you are an India citizen or a PIO and you live outside India and you come on a visit to India. The intention behind relaxing the minimum number of days to 182 is to protect your taxability (so you don’t get taxed as a Resident Indian) in case you decide to visit India for an extended stay to visit family or meet other obligations and end up staying more than 2 months.

If this sounds confusing, you can look at the ClearTax NRI tax filing assistance for more help.

Besides Resident and Non-Resident Indian, there is a third category – Resident but Not Ordinarily Resident (RNOR). After having spent many years abroad, if you have recently moved back to India, you may fall in the category of Resident but not Ordinarily Resident (RNOR).

Who is an RNOR?

A person is considered "not ordinarily resident" in India for a given previous year if they meet the following conditions:

- The individual should be a resident i.e., should satisfy both the conditions to become a resident and the individual has been a non-resident in India in

- 9 out of the 10 previous years preceding the relevant financial year or

- should have stayed in India for less than 730 days in the 7 years preceding the relevant financial year.

- A citizen of India, or a person of Indian origin, who has income exceeding Rs. 15 lakh from sources other than foreign income and has stayed in India for 120 days or more but less than 182 days during the relevant financial year.

- Indian citizen having total income (other than foreign source income), exceeding Rs. 15 lakhs during the PY shall be deemed to be resident but not ordinarily resident in India in that relevant financial year if he is not liable to pay tax in any other country or territory by reasons of his domicile or residence or any other criteria of similar nature.

Taxable Income of NRI and RNOR

If you are a NON-RESIDENT INDIAN (NRI), any income that is ‘earned’ or ‘accrued’ in India is taxable in India. Your Income outside of India is not taxable in India.

The salary of a non-resident seafarer for services outside India on a foreign ship will not be included in the total taxable income of the seafarer, even though such salary is credited to the NRE account of the seafarer with an Indian bank.

For instance, seafarer rendered services in Europe and spent less than 182 days in India and the company credited his salary to the NRE account with an Indian bank, then this income will not be included in the total taxable income of the seafarer.

If you are a RESIDENT BUT NOT-ORDINARILY RESIDENT (RNOR) and just returned to India, you are allowed to keep your RNOR status for up to 3 financial years post your return back to India. It could benefit you in a big way since your taxation will be very much in line with that of an NRI and therefore income that you may earn outside of India (while you may have returned) will continue to be not taxed in India. Therefore like an NRI –

- Any income that is ‘earned’ in India is taxable for you in India

- Your income outside of India is not taxable in India

However, once you have attained the status of a Resident, all of your income within and outside India will be taxable in India, barring any concessions that may be available under the Double Taxation Avoidance Agreement (DTAA) between India and the country from where your overseas income has arisen.

What Does ‘Earned’ in India Mean?

- Any income received in India or the law deems it to be received in India by you or on your behalf.

- Any income that accrues or arises in India or income that the law believes accrues or arises in India.

What Does ‘Accrues in India’ Mean?

This is laid out in Section 9 of the Income Tax Act (note that this applies to everyone while considering the income that accrues or arises to them irrespective of what their residential status is).

If your answer to any of the following is a YES then it will be considered that these incomes have accrued in India:-

- Income from a business connection in India.

- Income from any property, asset, or source of income in India.

- Capital gain on the transfer of a capital asset situated in India.

- Income from salary if the services are rendered in India.

- Income from salary which is payable to you by the Government of India for services rendered outside of India when you are an Indian citizen.

- Dividend paid by an Indian company even though this may have been paid outside India.

- Interest, royalty or technical fees received from the Central or the State Government or from specified persons in certain circumstances.

Deductions Available for NRIs under Section 80C

NRIs can claim the following deductions under Section 80C while filing their ITR:

- Payment towards Life Insurance premium

- Tuition fees paid for kids

- Payment towards Unit-Linked Insurance Plan (ULIP)

- Amount spent to repay the principal amount of the loan taken for purchasing or constructing a residential property.

- Investment in ELSS.

NRIs are also allowed deductions under certain conditions under Section 80G, 80D, 80TTA, Section 54, and Section 54EC.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption