Call Now

Call Now

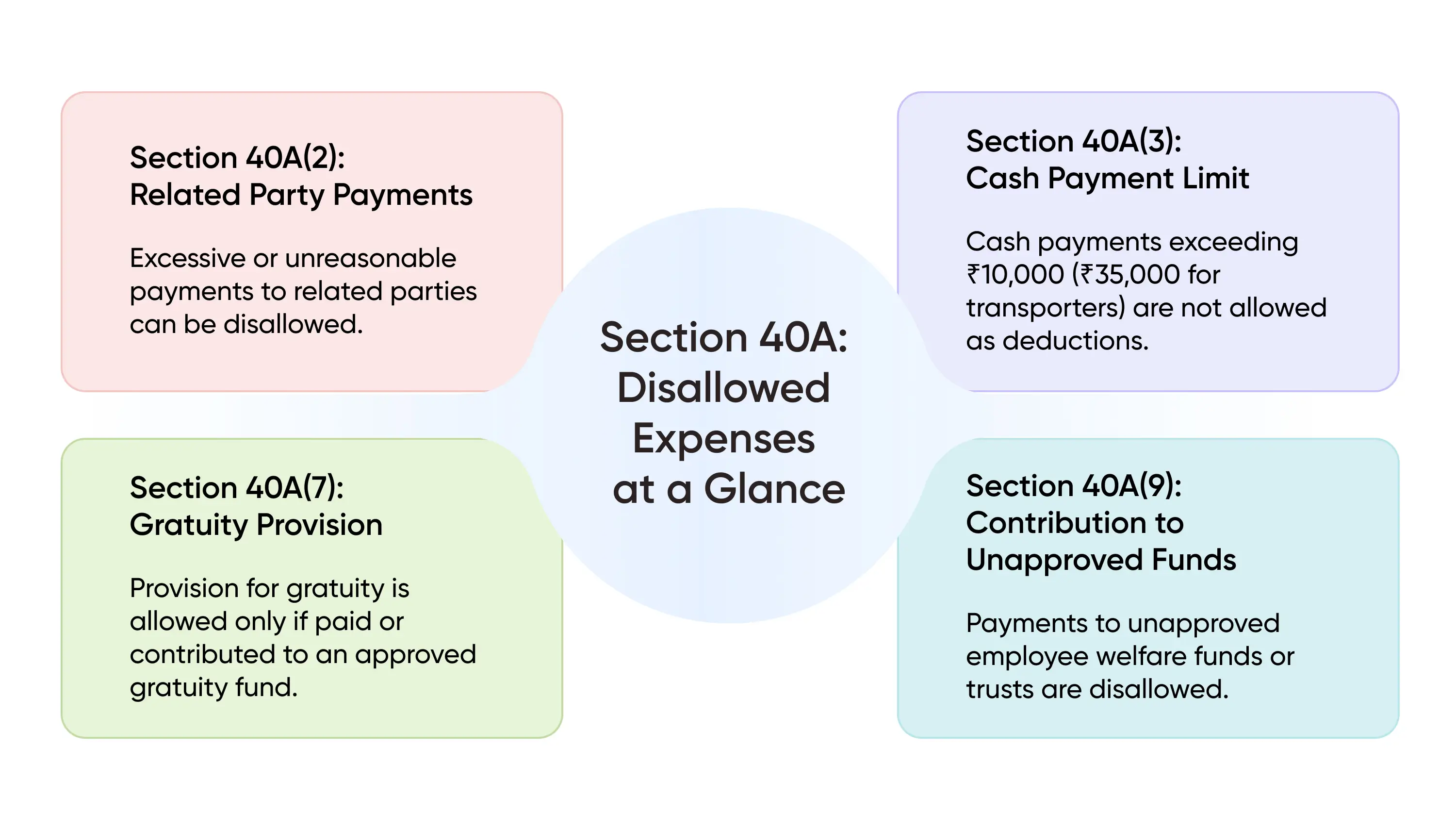

Section 40A - Disallowances Under Business Income

The provisions of Income Tax allow businesses and professionals to claim the expenses they incur in the course of business as deductions. After claiming all deductions, the net profit is considered for income tax calculations.

However, these provisions related to deductions can be misused, and businesses may claim more deductions than are rightfully claimable. Therefore, there are provisions incorporated in the law to restrict deduction claims upon satisfaction of certain conditions or completely forbid certain deductions in certain situations. In this article, we discuss disallowances given under section 40A of the Income Tax Act.

What is the Intent Behind Section 40A?

The purpose of this section is to

- Mandate proper documentation of expenses claimed

- Restrict the deductions only to the extent that it is reasonable

- Encourage non-cash payments - (Predominantly digital mode)

- Ensure transparency in related-party transactions.

It is to be noted that the provisions in section 40A have an overriding effect on the remaining provisions of the act. This means that in case of any conflicting circumstances between section 40A and other provisions - the provisions in this section shall prevail over other sections.

Summary to Section 40A

Broadly, section 40A discusses deductions pertaining to

- Related Party Transactions

- Payment made in modes other than prescribed

- Other disallowances

Related Party Transactions

This section gives discretion to assessing officer to disallow payments made to related parties, if the assessing officer opines that it is such deduction claim is excessive or unreasonable.

Who are the Related Parties?

Though people's perceptions of relatives vary, the term related party, as per the Income Tax Act, depends on the assessee's legal status. Though the meaning of relative differs based on legal status, the meaning of relative for an individual needs to be understood as it lays the foundation for definition of relative for other assessees.

Below is a table listing the related persons for various types of assessees, commonly recognised.

LEGAL STATUS OF THE ASSESSEE | MEANING OF RELATED PARTY |

Individual |

|

Company |

|

| |

Firm |

|

Association of Persons |

|

Disallowances on Payment Made to Relatives

If the payments made to relatives is considered as unreasonable or excessive by the assessing officer, the extent to which the payment is considered unreasonable can be disallowed by the assessing officer. He uses a few criteria to ascertain if the payments made are reasonable and not excessive. They include,

- The fair market value of goods and services involved or

- Legitimate needs of the business

- The payment made is relatable to the benefit derived.

Payments to be made in Prescribed Mode

If the assessee makes a payment greater than ₹10,000 in one day to one party in modes other than prescribed modes, the amount paid will be disallowed for income calculation under section 40A(3).

Points to be Considered for Allowing the Deduction

- Payments are to be made only through

- If the payment made is less than or equal to ₹10,000, even cash payments can be allowed.

- The Limit of ₹10,000 is to be considered for payment made to one party in a single day.

- When the total cash payment to a single person exceeds ₹10,000 in a day, the entire sum is disallowed, regardless of whether it is paid in more than one instalment during the day.

- The entire cash payment made to a single person in a day is disallowed if it exceeds ₹10,000, not just the amount exceeding the limit.

- If cash payments to a single person do not exceed ₹10,000 on any given day, the total sum is allowed, even if the aggregate amount exceeds ₹10,000 over multiple days.

Payments Made for Liabilities of Preceding Financial Years

- The above conditions also apply to the payments made pertaining to liabilities of the preceding financial years.

- If the deduction pertaining to these liabilities has already been claimed and the payments are made in the current financial year, the conditions prescribed above should be followed even then.

- If not, the amount claimed as a deduction in the preceding financial years needs to be disallowed in the current year for the computation of income.

Exceptions to Section 40A(3)

Even when the payment is made other than prescribed modes above the limit for the below transactions, the amount will not be disallowed.

- Payment is made to/via the following financial institutions

- Reserve Bank of India or

- Banking company

- Letter of credit arrangements through a bank

- Mail or telegraphic transfer through a bank

- Payment is made to the Government.

- Settlement through book entry adjustments

- Payment is made to the cultivator for the purchase of

- Agricultural or forest produce; or

- Animal husbandry (including livestock, meat, hides and skins) or dairy or poultry farming; or

- Fish or fish products; or

- Horticulture or apiculture products,

- Payment made to the producer for items produced in a cottage industry without the aid of power.

- Payments are made to a person in a village where there are no banking facilities available.

- Payment is made to an agent wherein the agent is required to make payment on behalf of us.

- Payment made by an authorized dealer for the purchase of foreign currency in the normal course of business.

- Payment is made to the employee or his heir on account of gratuity or similar terminal benefit. In such cases, a limit of Rs.50,000 is allowed.

Contribution and Payment of Gratuity

During employment, the employer earmarks a certain amount every year to meet the employee's gratuity expense at the end of his tenure. This is widely known in accounting terms as the Contribution to the Provision for Gratuity.

This provision prescribes certain conditions for claiming the deduction for gratuity payment or contribution. They are,

- The deduction can be claimed only if the contribution is made to an Approved Gratuity Fund or

- Payment of Gratuity is made directly to the employee.

In other cases, the contribution to the provision for gratuity is disallowed from claiming the deduction. Let us understand this concept with an illustration.

Illustration

Mr. A has contributed Rs.10,000 to an unapproved gratuity fund for ten years. He paid the accumulated balance of Rs.1,00,000 to employee at the time of the his retirement. In this case, Rs.1,00,000 is allowed on the year of payment made to the employee. Not at the year of the contribution made.

If Mr. A contributed to an approved gratuity fund, the amount could have been claimed as deduction on the year of contribution itself. No need to wait until final payment made.

The amount that has already been claimed as deduction at the year of contribution cannot be allowed again on the year of payment to employee at the end of his tenure.

Final Word

It is crucial for businesses to have a clear understanding of the circumstances in which their expenses may not be deductible for tax purposes. This article highlights common situations wherein payments may be disallowed. Awareness of these provisions are important for businesses to ensure compliance, avoid potential disallowances, and safeguard themselves from any unforeseen tax liabilities.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption