|

Tax Collected at Source (TCS) – Rates, Payment and Exemption

TCS stands for Tax Collected at Source. TCS refers to the tax payable by a seller which he collects from the buyer at the time of sale of goods. The provisions related to TCS are covered under section 206C of the act.

TCS is levied on specified goods like alcohol (1% - 5%), on specified leasing activities (2%), on sale of high value motor vehicles (1%) , and specified remittances under Liberalized Remittance Scheme (LRS) of RBI (5% - 20%). In this article, we will discuss the different transactions on which TCS has to be collected, TCS due dates, late payment interest and penalties.

Budget 2026 Update

- The TCS rate on LRS for health and education has been reduced to 2%.

- TCS rate on LRS for overseas tour package is proposed to be reduced to 2% without any stipulated amount from the existing 5% and 20%.

What is Tax Collected at Source (TCS)?

- Tax collected at source (TCS) is the tax payable by the seller which he collected from the buyer on sale.

- It should be deposited with the tax authorities within the applicable due dates.

- Section 206C of the Income-Tax Act governs provisions related to TCS. Such persons must have the Tax Collection Account Number (TAN) to be able to collect TCS.

- Seller is responsible only for collecting the tax and depositing it to the government. He is not responsible for paying the TCS out of his pocket.

Example:

- Mr. A sold goods worth Rs.100 to Mr. B on which TCS is applicable.

- Mr. A will collect the TCS at 1% from the buyer

- So, he will be collecting Rs.101 from Mr. B (Rs.100 + 1%of 100)

- The money so collected as TCS should be deposited to the government within the specified due dates.

- Mr. A is responsible only for collecting the tax and depositing it to the government.

The TCS rates for different goods is specified below:

Who Can Collect TCS?

- The seller should collect tax from the buyer in addition to the value of the goods/services.

- A buyer is a person who purchases specific goods. He is liable to pay TCS amount along with the bill amount in applicable cases.

TDS and TCS - An Illustration

Confused Between TDS and TCS? Let's get it sorted now through this illustration!

Consider yourself as a customer who has made a purchase worth Rs 100 and needs to pay the bill amount to the seller. In this case, consider the TDS/ TCS amount comes to Rs 10.

If TDS Needs to be Deducted

- The person who pays the bill (you) needs to deduct the TDS of Rs. 10 and pay only the rest (Rs. 90) to the seller.

- You are also responsible for remitting the TDS deducted to the government within the applicable due dates.

If TCS Needs to be Collected

- The seller - the person who receives the money, needs to collect the TCS amount (Rs 10) plus the bill amount (Rs. 100) from you. Totally, you will be liable to pay Rs. 110.

- The seller is responsible for remitting the TCS amount to the government within the applicable due dates.

- Broadly speaking, the whole process of collecting TCS and remitting it to the government can be compared to the system of the seller collecting GST from the customer and paying it to the government.

When Should TCS be Collected?

The seller must collect TCS at the earlier of the following two dates:

- When the seller passes the entry in the books of accounts for credit sales.

- When the seller receives the money from the buyer in any mode. (cash or cheque or draft)

In the case of the motor vehicle sale, the TCS is collected upon receipt of money from the buyer.

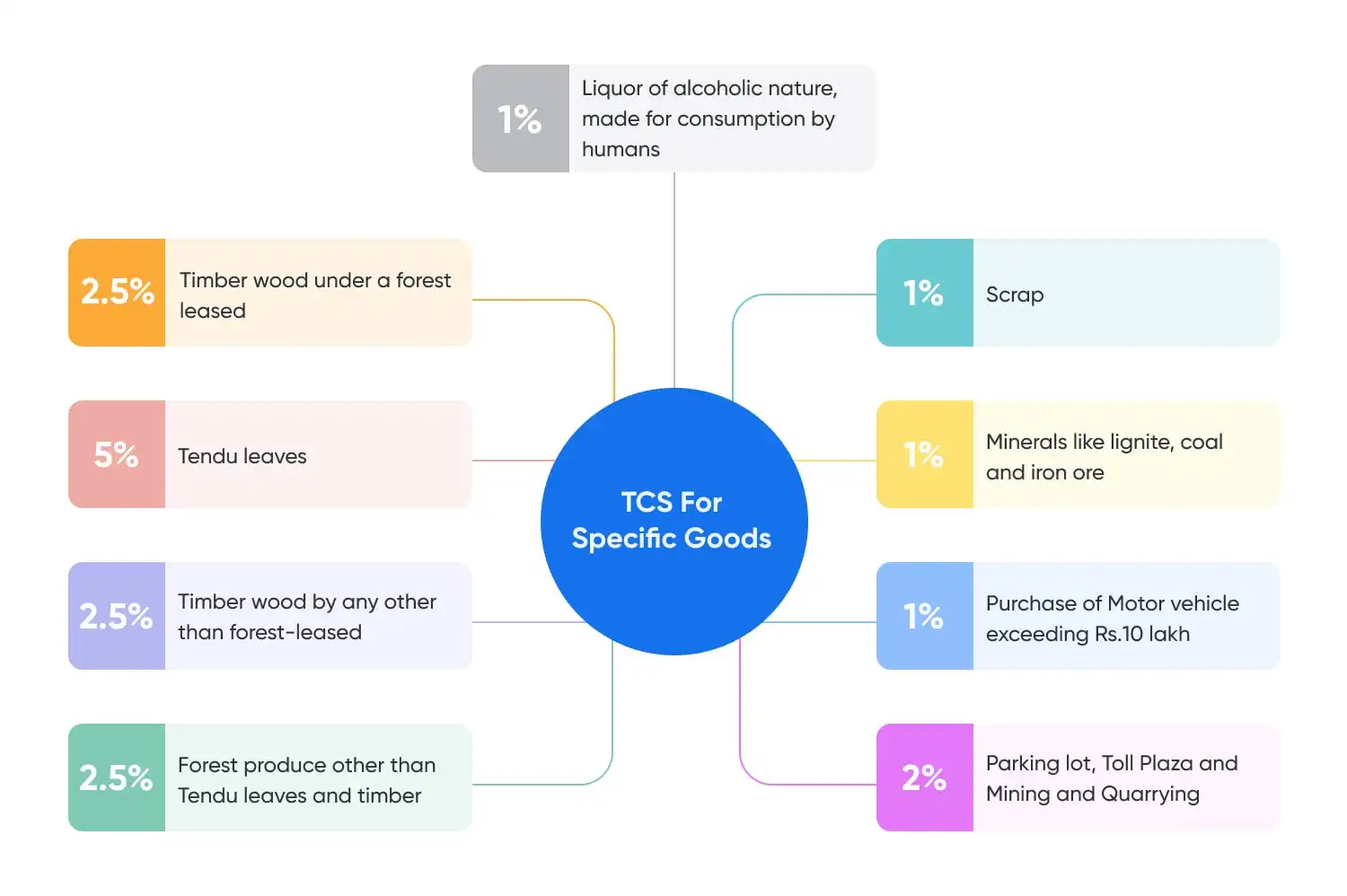

TCS Rates for Specific Goods u/s 206C(1)

Taxes are paid only when the goods are utilized for trading purposes, and not when utilized for manufacturing, processing or producing things. The tax payable is collected by the seller at the point of sale. The rate of TCS is different for goods specified under different categories under section 206C(1):

| Type of Goods or Transactions | Rate |

| Liquor of alcoholic nature, made for consumption by humans | 1% |

| Timber wood obtained under a forest leased | 2.5% |

| Tendu leaves | 5% |

| Timber wood by any mode other than forest-leased | 2.5% |

| Forest produce other than Tendu leaves and timber | 2.5% |

| Scrap | 1% |

| Minerals being lignite, coal and iron ore | 1% |

Section 206C(1C) - TCS on Leasing, Licensing, and Mining Contracts

A person granting lease or license for a

- Parking lot,

- Toll plaza

- Mine or quarry,

should collect TCS at 2%.

Section 206C(1F) - TCS on Motor Vehicle and Luxury Goods

- Section 206C(1F) applies to sale of

- Motor vehicles exceeding Rs 10 lakhs and

- Notified luxury items whose value exceeds Rs 10 lakhs.

- Motor vehicles refer not only to car, but to all motor vehicles (including bikes, etc.,).

Therefore, even if the value of the bikes purchased exceeds Rs 10 lakhs, TCS is applicable.

- The notified luxury items are listed below:

| Sl No. | Types of Goods |

| 1 | Wrist Watch |

| 2 | Art pieces like antiques, paintings and sculptures |

| 3 | Collectables such as coins and stamps |

| 4 | Yacht, rowing boats, canoe, and helicopter |

| 5 | Pair of sunglasses |

| 6 | Handbags and Purses |

| 7 | A pair of shoes |

| 8 | Sportswear and equipment |

| 9 | Home theatre system |

| 10 | Horse for racing and polo games |

- TCS at 1 % needs to be collected on sale consideration when the value of the goods exceeds Rs 10 lakhs.

Section 206C(1G) - TCS on Overseas Remittance or Overseas Tour Package

Under section 206C(1G) TCS needs to be collected by

- Authorized dealer on remittances under Liberalized Remittance Scheme

- Seller of overseas tour package program on collecting money from the customers

at the rates applicable.

TCS Exemptions

Tax collection at the source is exempted in the following cases:

- If the resident buyer furnishes a declaration to the seller that “goods” are to be utilised in manufacturing or production of any article or for the purpose of generation of power.

Example of TCS Calculation

If a buyer purchases a car from a showroom valued at Rs.11 lakh, then the showroom must collect and deposit Rs. 11,000 as the TCS. So, the total amount to be collected from the buyer is Rs.11,11,000 (Rs. 11,00,000 + Rs. 11,000).

TCS Payments & Returns

- The seller has to deposit the TCS amount within 7 days from the last day of the month in which the tax was collected (monthly).

- If the seller does not comply with TCS collection and payment provisions, he will be liable to pay interest of 1% per month or part of the month.

- Every tax collector must submit a quarterly TCS return, Form 27EQ, for the tax collected in a particular quarter. The interest on delay in payment of TCS to the government should be paid before filing the return.

TCS Certificate - What Is Form 27D?

When a tax collector files his quarterly TCS return by filing Form 27EQ, he has to provide a TCS certificate to the purchaser of the goods.

Once TCS has been filed for the receipts, a certificate is generated for the receipts reported in Form 27EQ. This certificate is known as Form 27D which is issued by the seller to the buyer as the proof of TCS collection.

Contents Of Form 27D

Form 27D contains the following details:

- Name of the Seller and Buyer

- TAN of the seller i.e. who is filing the TCS return quarterly

- PAN of both seller and buyer

- Total tax collected by the seller

- Date of collection

- The rate of Tax applied

Due Date For Form 27D

This certificate has to be issued within 15 days from the date of filing TCS quarterly returns. All the TCS due dates are summarized in the below table:

| Quarter Ending | Due date to file TCS return in Form 27EQ | Date for generating Form 27D |

| For the quarter ending on 30th June | 15th July | 30th July |

| For the quarter ending on 30th September | 15th October | 30th October |

| For the quarter ending on 31st December | 15th January | 30th January |

| For the quarter ending on 31st March | 15th May | 30th May |

In case you are still confused about filing TCS returns, feel free to consult the tax experts at ClearTax.

You can also download the format of Form 27D.

Interest Chargeable on Non-Remittances of TCS

If a tax collector fails to collect the tax or neglects to remit it to the government within the specified due dates, they will be subject to an interest charge of 1% per month or part thereof.

Penalty for Incorrect Filing of the TCS Return

According to Section 271H, a penalty may be imposed if the tax collector submits an erroneous TCS return. A minimum penalty of Rs.10,000 and a maximum penalty of Rs. 1,00,000 may be levied.

Also Read:

1. Budget 2026 Highlights

Frequently Asked Questions

About the Author

CA Mohammed S Chokhawala

I'm a chartered accountant, well-versed in the ins and outs of income tax, GST, and keeping the books balanced. Numbers are my thing, I can sift through financial statements and tax codes with the best of them. But there's another side to me – a side that thrives on words, not figures. Read more

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption