Call Now

Call Now

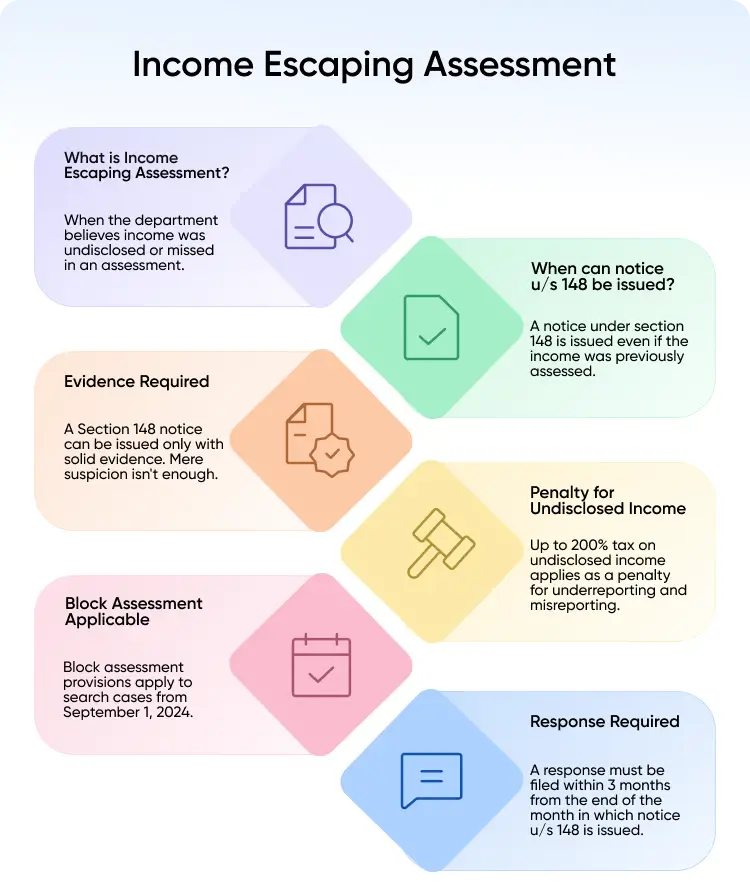

Income Escaping Assessment

After finalising the taxpayer’s total tax liability for the assessment year, the Income Tax department recognised later that some of the income had been missed while calculating the taxes during any year. This missed income is known as ‘income escaping assessment’. The Income Tax Department, under section 147, empowers the Assessing Officer to open the case and reassess that year's income. However, not only income, if the Assessing officer finds any losses, deductions or expenses not correctly claimed as per the provisions of the Income Tax Act, he can initiate an enquiry on them under the initial notice only.

Budget 2026 Update

In case of re-assessment proceedings, updated return can be filed even after the beginning of the assessment proceedings. Section 280 (Section 148 of the Income Tax Act 1961) is amended to allow the taxpayer to file updated return even after notice under the section is issued. The updated return filed will be considered for the re-assessment proceedings, not the returns filed earlier.

Assessment v/s Reassessment

After filing a tax return, the returns are automatically processed at the Central Processing Centre (CPC) in Bangalore. The software automatically selects certain cases for further scrutiny by the Assessing Officer (AO) based on certain criteria fixed by the Central Board of Direct Taxes (CBDT).

Example:

Raghav filed his income tax return on 5th July 2024 for the year ending 31st March 2024. The return has been filed in AY 2024-25. Therefore, Raghav can be issued a scrutiny assessment notice anytime before 30th June 2025.

Assessment

The entire proceeding, from the time a taxpayer receives a notice to the time the assessing officer passes the final assessment order determining the taxpayer’s final taxable income, is called an assessment proceeding. The proceedings are initiated to make sure that there is no understatement of income, excessing claim of losses or underpayment of taxes by the assessee so that the government gets the amount of revenue. A scrutiny assessment notice can be issued within three months from the end of the financial year in which the return of income has been filed.

Reassessment

If an AO has the information suggesting that any income chargeable to tax has escaped assessment, the AO has the authority to issue a notice to reopen the case for scrutiny. For instance, scrutiny proceedings in the case of Mr Rohan for FY 2023-24, have concluded, and the tax authorities are in agreement with the income Rohan has disclosed in his return. Subsequently, the assessing officer receives some information with regard to a sale of land that Rohan has carried out during FY 2023-24. Rohan did not disclose capital gains in his return for FY 2023- 24. On the basis of such information, the AO can reopen the assessment.

Instances Of Income Having Escaped Assessment

- In technical terms, the income which is not disclosed at the time of filing returns is referred to as the income escaping assessment.

- Where the assessee has an income exceeding the basic exemption limit i.e. Rs 3,00,000 under the new tax regime. The old tax regime has a basic exemption limit of Rs.2,50,000 (Rs. 3,00,000 and Rs.5,00,000 for senior and super senior citizens). The assessee has not filed Income tax return.

- Where the assessee has filed the return, but it is found that the income disclosed is understated or has losses/ deductions have been overstated.

- In case of any international transaction, the assessee has not filed the relevant report under section 92E.

- If it has been found that the assessee has any assets outside India.

Time Period To Issue Notice

As per law, a valid notice must always be served before an assessment or reassessment. The notice cannot be sent if three years have passed since the end of the relevant assessment year. However, a notice can be issued after three years but within ten years if the Assessing Officer (AO) possesses books of accounts or documents or any other evidence showing income chargeable to tax, which escaped assessment. This income evidence should be in the form of an asset, transaction of an event, or any entries in the books of accounts amounting to Rs.50 lakhs or more between three to ten years from the relevant assessment year.

Persons Authorised To Issue Reassessment Notice

An assessing officer (AO) with such below rank can also issue notice under section 148 only with the prior written approval from the Additional Commissioner or the Additional Director or Joint Commissioner or Joint Director.

Related Articles

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption