Leave Encashment - Tax Exemption, Calculation & Formula With Example, Rules

Employees have a certain number of paid leaves in a year which they can avail at their discretion. However, most of the time these leaves remain unused. In such a scenario, the employer allows the employee to carry forward the unused leave to the next year. The employees also have an option to get paid for their unused leaves instead of taking holidays. Such monetary compensation is taxable in the hands of the employee.

This article will explain the tax implication on leave encashment received and the exemption that the employee can claim as per the Income Tax Act.

What is Leave Encashment?

Leave encashment means receiving monetary compensation in exchange for the unutilised paid leaves availabe to the employee over the course of employment.

As per labour law, every salaried person is entitled to a minimum number of paid leave every year. However, it is not necessary that an individual employee utilises all the leave he is entitled to in a year. In fact, most employers allow the employees an option of carrying forward such unutilised paid leaves.

This would invariably leave the employee with an accumulated unutilised leave balance at the time of retirement or resignation from the company, as the case may be. This compels the employer to compensate the unutilised paid leave of the employees. This concept is better known as leave encashment.

What are the Types of Leaves?

The different types of leaves are mentioned in the leave policy of a company. The leave policies differ from company to company. Here are the types of leaves generally available for employees:

- Casual leave: Casual leaves are available for 7 to 10 days. Employees may avail of these leaves for personal reasons. Encashment of this leave varies from one company to another.

- Earned leave or privilege: An employee can avail of earned leaves with prior notice to the authority. These leaves become eligible for encashment after a specific period. This policy varies from one organisation to another.

- Medical leaves: If employees cannot perform their duties towards the organisation due to health conditions, they must inform the employer of the leaves. The maximum limit of the number of medical leaves available differs from one firm to another.

- Holiday leaves: Holiday leaves are granted by employees, and no salary is deducted for these leaves. The maximum number of holiday leaves differs from one company to another.

- Maternity leaves: Maternity leaves are only available for female employees and can range from 12 to 26 weeks during pregnancy. An employee can ask for an extension, but no payment shall be made for that period. However, these leaves are not available for encashment.

- Sabbaticals: Employees can take leaves for upskilling and expand their knowledge. They can enrol for a course, and for that period of time, the employer will reimburse those leaves.

Taxation of Leave Encashment

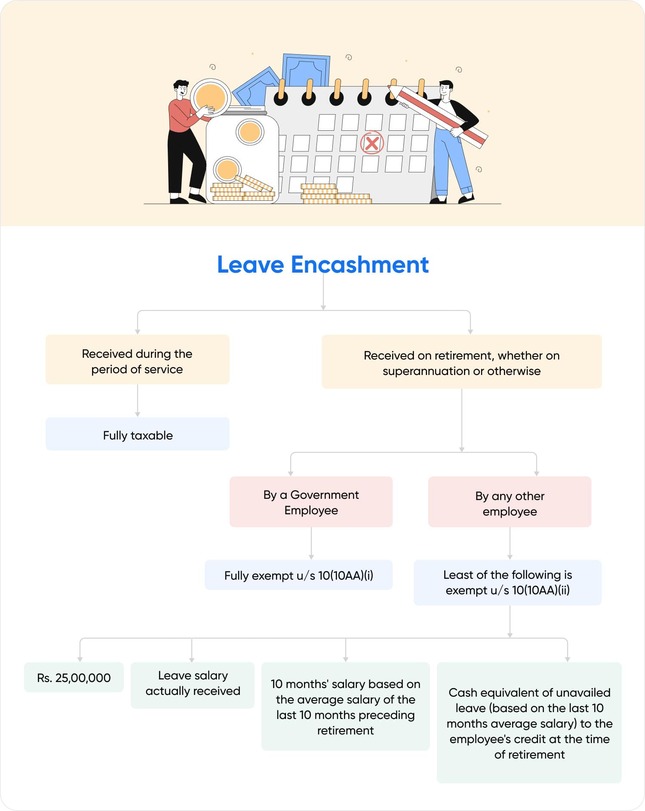

Leave encashment received by employees is taxable based on when it is received. Leave encashment can be received in the following two cases:

Leave encashment received during service

If an employee gets leave encashment while on his job, that amount becomes fully taxable and forms part of ‘Income from Salary'. However, you can claim some tax benefits under Section 89 of the Income Tax Act. You must fill up Form 10E to claim the tax relief for salary arrears on leave encashment. You can fill up and submit this form online on the income tax portal.

Leave encashed at the time of retirement or resignation

Here are the following conditions under which you can claim partial or complete exemption of leave encashment received at the time of retirement:

Leave encashment received by | Taxability |

| State and Central Government employees | Fully tax-exempt |

| Non-government employees | Partly exempt and partly taxable. The exemption is based on the calculation specified in Section 10(10AA)(ii). |

| Legal heir of a deceased employee | Fully tax-exempt Leave encashment amount received by the Legal heir of a deceased employee is fully tax-exempt in the hands of the legal heirs. |

Leave Encashment Calculation

The formula for computing leaves encashment exemption of non-government employees:

Particulars | Amount (Rs) |

| Leave encashment received (A) | XXXX |

| Less: Exemption under Section 10(10AA) – (B) Least of the following: | XXXX |

| i) Amount notified by the Government** Rs 25,00,000 (C) ii) Actual leave encashment amount (D) iii) Average salary* of last 10 months (E) iv) Salary per day *unutilised leave (considering maximum 30 days leave per year) for every year of completed service (F) | 25,00,000 XXXX XXXX XXXX |

| Leave encashment taxable – (A) – (B) | XXXX |

*Salary for this purpose includes basic salary, dearness allowance and commission based on a fixed percentage of turnover secured by the employee.

**Specified amount of Rs 25,00,000 is the aggregate amount allowed as an exemption irrespective of the frequency of leave encashment received by the employee by various employers. If an employee has utilised Rs 5,00,000 already at the time of first resignation, he is only entitled to use the balance of Rs 20,00,000 for the exemption computation next time. Hence, the overall employee is allowed a total exemption of only Rs 25,00,000 with respect to leave encashed from all employers.

Note:

1. If leave encashment is received from two or more employers in the same previous year, then the maximum amount of exemption is capped at Rs.25,00,000.

2. Exemption under section 10(10AA) would be available to an assessee irrespective of the regime under which he pays tax.

Leave Encashment Exemption Example

Let us understand leave encashment exemption with the help of an example:

Mr A is retiring after 15 years of service. Mr A was entitled to 35 days of paid leave per annum from his employer, i.e., overall 525 days of leave during his entire service (35*15).

Out of the same, Mr A has already utilised 200 days of paid leave and is left with 325 days of unutilised leave.

Mr A was drawing basic salary + DA of Rs 33,000 per month at the time of retirement and received Rs 3,57,500 as leave encashment calculated based on 325 days * Rs. 1,100 (salary per day = Rs.33,000/30 days).

Particulars | Amount (in Rs) |

| Leave encashment received | 3,57,500 |

| Less: Exempt (lowest of the below) | 2,75,000 |

| Least of the following: 1. Amount notified by the Government 2. Actual leave encashment 3. Average salary for 10 months= Rs 33,000 * 10 months 4. Rs 1,100 * (30 days * 15 completed years of service minus 200 days of utilised leave) | 25,00,000 3,57,500 3,30,000 2,75,000 |

| Leave encashment taxable as ‘income from salary | 82,500 |

Based on the employer’s leave encashment policy and the income of an individual, tax planning can be made by deciding whether it is beneficial to encash leave year on year or to receive a lump sum at the time of retirement or resignation.

One may consider the cost of inflation as well before deciding on the same.

Related Article:

Leave Encashment Calculator

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption