Call Now

Call Now

Saving Taxes on Long-Term Capital Gains

Saving capital gains tax in India is possible through smart tax planning using legal exemptions and deductions under the Income Tax Act. By investing in options like capital gain bonds, residential property, or eligible mutual funds within prescribed timelines, taxpayers can reduce or even eliminate capital gains tax on the sale of assets.

What is Capital Gains Tax?

- Capital gains are the profits investors make when they sell their assets for a higher price than the price at which they were acquired. They include land, vehicles, jewellery, shares, and stocks.

- Capital gains are taxable, and there are two types: short-term and long-term. Short-term capital gains result from the sale of an asset held for up to 24 months (2 years).

- The criteria is 12 months for listed equity shares, equity-oriented funds and units of UTI.

- Long-term capital gains result from the sale of assets held for more than the holding period as discussed above.

Long-Term Capital Gains Tax

There are certain exemptions available for long-term capital gains. If you carry out specific investments/activities outlined in the Income Tax Act, you can legitimately save on long-term capital gains tax. One of the key requirements for avoiding capital gains tax is to reinvest the proceeds from the sale of the property/assets in the prescribed assets or bonds.

Let us look at the three primary long-term capital gains tax exemptions:

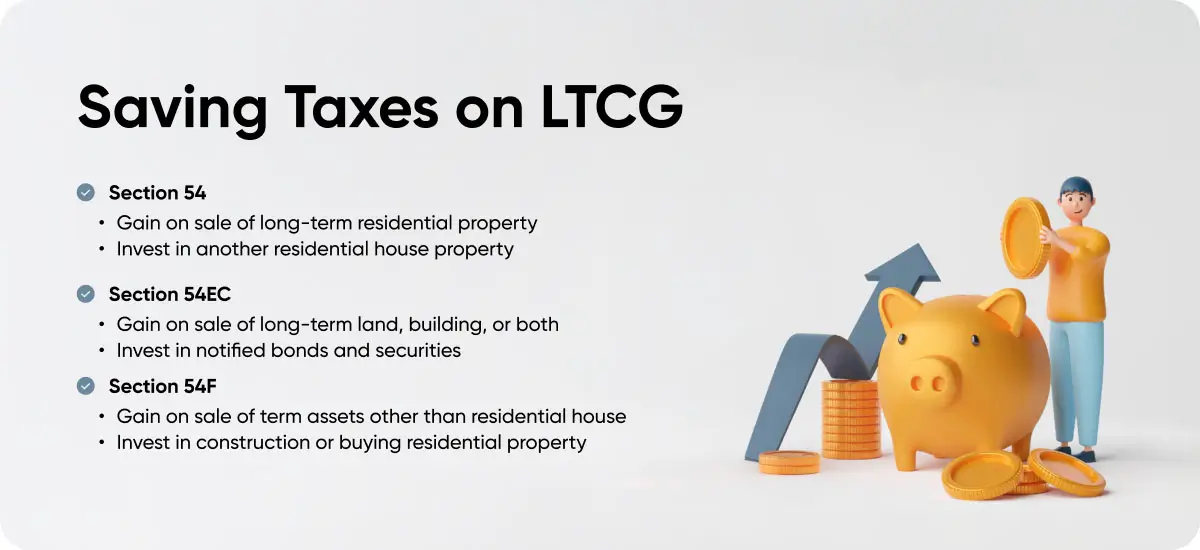

- Section 54: Section 54 addresses the exemption from long-term capital gains on the sale of a residential property if the proceeds are reinvested in another residential property.

- Section 54EC: Section 54EC addresses the exemption from long-term capital gains on the sale of a land or buildings if the proceeds are reinvested in designated bonds.

- Section 54F: Section 54F relates to exemption from long-term capital gains on the sale of any asset other than a residential property, if the proceeds are reinvested in the purchase of a residential property.

- Capital Gains Account Scheme (CGAS): If you are unable to invest long-term capital gains before the due date of filing your Income Tax Return (ITR) for the year, you can deposit the funds in a CGAS account.

Sell One House and Purchase Another

Assume you're selling a home you've owned for over two years. The purchase cost of the house is Rs. 20 lakhs when you acquired it, and you are selling it for Rs. 42 lakhs. In this case, you earned a profit of Rs. 22 lakhs (ignoring the indexation benefit) and must pay long-term capital gains tax on this amount. According to the act, you must pay 20% LTCG tax (with indexation) and a 4% surcharge and cess. However, if you use the proceeds from the sale of the previous residential property to purchase another residential property, you will be exempt from paying this tax.

Exemption under Section 54

- Section 54 exempts you from paying LTCG tax on the sale of an old house if you acquire a new house either one year before or within two years of selling your old one.

- If you intend to build a new house, you must do so within three years of selling your old one.

- You can claim an exemption up to the lesser of (i) the amount of capital gains or (ii) the purchase/construction cost of a new house / residential property. In the current case, if you purchase a new house for Rs.22 lakh or higher, you will not be required to pay any LTCG tax.

Restrictions/Conditions under Section 54

- Only 1 House: You can only claim an exemption for the acquisition of 1 house. If you use capital gains to acquire more than one house, you can only claim an exemption for the cost of one dwelling.

- House in India: You are eligible for an exemption under Section 54 only if you purchase a home in India. Any residential property purchased outside India will not be considered for exemption.

- Lock-in: You cannot sell the new house purchased using the proceeds from the sale of the old house for three years after the purchase or completion of construction. If you sell the new house within such prescribed time, Section 54 exemption will be revoked, and you will have to pay the LTCG tax.

- Max Limit: If the capital gains from the sale of an old house are more than Rs. 10 crores, then the excess of capital gains over and above Rs. 10 crores is to be ignored for exemption. i.e., the maximum capital gains that can be claimed as exempt under this Section is Rs.10 crores.

Sell Your Stocks and Buy a House

Other long-term assets, such as land, commercial buildings, stocks, mutual funds, bonds, automobiles, patents, trademarks, jewels, and machinery, also provide capital gains. For example, you want to sell listed equity shares you've held for over a year. You purchased the shares for Rs. 15 lakhs and sold them for Rs. 23 lakhs. You are getting capital gains of Rs. 8 lakhs in this case. These capital gains can be exempted from tax if invested in purchasing or constructing a new residential property.

Exemption under Section 54F

- Section 54F exempts you from paying LTCG tax on the sale of long-term capital assets other than a house if you utilise the sale proceeds to buy/construct a new house.

- The new house should be purchased either one year before or within two years of the sale of the long-term asset.

- If you intend to build a new house, it must be completed within three years of the sale of the long-term asset.

- In this Section, the exemption is available on the investment of sale proceeds and not capital gains. For example, to claim the total exemption, all sale proceeds need to be invested.

- You can get a total exemption if you invest the whole of the sale proceeds in buying the new house.

- However, if you are using only a portion of the sale proceeds amount, the capital gains exemption will be calculated as follows:

Amount of Capital Gains * Cost of New House / Sale Proceeds from Sale of Assets

Restrictions/Conditions under Section 54F

- Only 1 House: You can only claim an exemption for the acquisition of 1 house. If you use capital gains to acquire more than one house, you can only claim an exemption for the cost of one dwelling.

- Max Limit: The Finance Act 2023 introduced a maximum limit under this Section. As per it, if the sale proceeds from the sale of long-term capital assets are more than Rs. 10 crores, then the excess of sale proceeds over and above Rs. 10 crores is to be ignored for exemption. i.e., the Maximum Capital Gains that can be claimed as exempt under this Section are to be based on an investment of sale proceeds of Rs. 10 crores.

- Lock-in: You cannot sell the new house purchased using the proceeds from the sale of the old house for three years after the purchase or completion of construction. This means that if you sell the new house within three years of the completion of purchase/construction, the benefit you receive under Section 54 will be revoked, and you will have to pay the LTCG tax.

- Additional Condition: This section's benefit is available only to taxpayers who do not own more than one house.

Sell your House or Stocks and Invest in Bonds.

Another approach to reducing LTCG tax is to invest capital gains in notified bonds if you are selling a long-term asset but do not intend to invest in a new dwelling. To avail of these exemptions, the interest rate on these bonds is 5.25% annually, and they are typically issued by government agencies such as the Rural Electrification Corporation (REC) and the National Highways Authority of India (NHAI). The interest earned is not tax-free.

Exemption under Section 54EC

- Section 54EC provides that you do not have to pay LTCG tax on the sale of any long-term capital assets if the capital gains are invested in the designated government bonds and instruments.

- The bonds must be purchased within six months following the asset's sale.

- The maximum that can be invested in this manner is Rs. 50 lakhs.

Restrictions/Conditions under Section 54EC

- You are only entitled to a tax break if you invest in the notified bonds and securities.

- You will lose this exemption if you sell these bonds within five years after obtaining them.

- This exemption will be withdrawn if you borrow against these bonds within five years after acquisition.

Deposit in Capital Gain Deposit Account Scheme

- Section 54 and Section 54F are complemented by the Capital Gain Account (CGAS) Scheme, 1988.

- If you cannot invest all / desired capital gains in new property by the due date for submitting your income tax return, you can deposit the unutilised amount in any public sector bank under the CGAS Scheme.

- Once the money is in this account, you must utilise it within two years (if you are buying a new house) or three years (if you are building a new house).

- You must open the account before the deadline for filing your ITR, and the funds must only be used to purchase/construct a residential property.

- If the money is not used to buy/build a residential property within the stipulated time, the capital gains exempted earlier will be taxed in the future year.

Other Tax Saving Strategies

Transfer Expenses

- Expenses incurred solely for the purpose of transfer can be claimed as a deduction in calculation of capital gains tax.

- For example, you can claim deductions on stamp duty charges, brokerage, legal fees etc. as deduction.

- However, expenses indirectly incurred cannot be claimed as a deduction such as travel and lodging expenses, telephone and courier charges related to sale of property etc.

Cost of Improvement

- For the land to be used or re-used in the desirable state, you might have incurred certain expenses namely leveling, water connection, demolition of old structures and clearing the debris, internal connectivity such as roads, electricity connection etc.

- You can claim those expenses as cost of improvement in calculation of capital gains.

- If the capital gains are long term in nature, indexation can also be claimed for cost of improvement.

Indexation Benefits

- Indexation benefits can be availed if the capital gains are long term in nature.

- For resident individuals, there is still an option to claim indexation benefits on sale of land.

- Indexation benefit adjusts the purchase cost to the inflation levels at the date of sale, thereby increasing the purchase price and eventually reduce the taxable capital gains.

Tax Loss Harvesting

- You can offset the long term capital losses on sale of shares, mutual funds or any other asset, with the long term capital gains on properties, etc.

- Even short term capital losses can be set off against long term capital gains.

- This set off can be done even if the loss assets are immediately purchased again at the same price.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption