Call Now

Call Now

Hindu Undivided Family – HUF Meaning, Benefits & How to Reduce Tax?

A Hindu Undivided Family (HUF) is a powerful and legal tax-saving tool under Indian income tax law, used for income splitting and wealth management. As a separate taxable entity, it can earn income and claim deductions like Section 80C, 80D, and capital gains exemptions. Forming a HUF, and obtaining the PAN involves very simple process, explained in the following blog in detail.

Key Highlights

- HUF is a separate person from the family members for tax purposes.

- Income of members can be split and shown as HUF income legally, allowing more tax benefits.

- HUF enjoys a separate basic exemption limit of Rs. 2.5 lakh under the old tax regime and Rs. 4 lakh under the new tax regime.

What is an HUF?

- The full form of HUF is Hindu Undivided Family.

- It is a separate legal entity under the Income Tax Act, created for tax purposes.

- This is one of the tax saving strategies legally available to joint families.

- An HUF can own property, earn income, and claim tax benefits independent of its members, helping families reduce their overall tax liability by legally splitting income.

- The head of the HUF is called the Karta, while the family members are coparceners.

Who can Form HUF?

- Buddhist, Sikh and Jain families are also covered under the ambit of HUF.

- HUF cannot be created by one person. Minimum of 2 persons are required to form an HUF.

- A family with lineal ascendants and descendants is required to form an HUF.

- An HUF can be created upon marriage as well.

Who are the Members of HUF?

The members of an HUF are common ancestor and all lineal descendants, including their wives and unmarried daughters. The members include:

- Karta: The head of the HUF, usually the senior-most male or female member, who manages the family affairs and has unlimited liability.

- Coparceners: All male and female lineal descendants of a common ancestor, including daughters by birth, who have equal rights in HUF property and can demand partition.

- Other Members: Wives of coparceners become members of HUF after marriage but are not coparceners themselves. They have maintenance rights but no right to demand partition.

Only coparceners can claim partition of HUF, while Karta carries unlimited liability for HUF dues, including tax obligations.

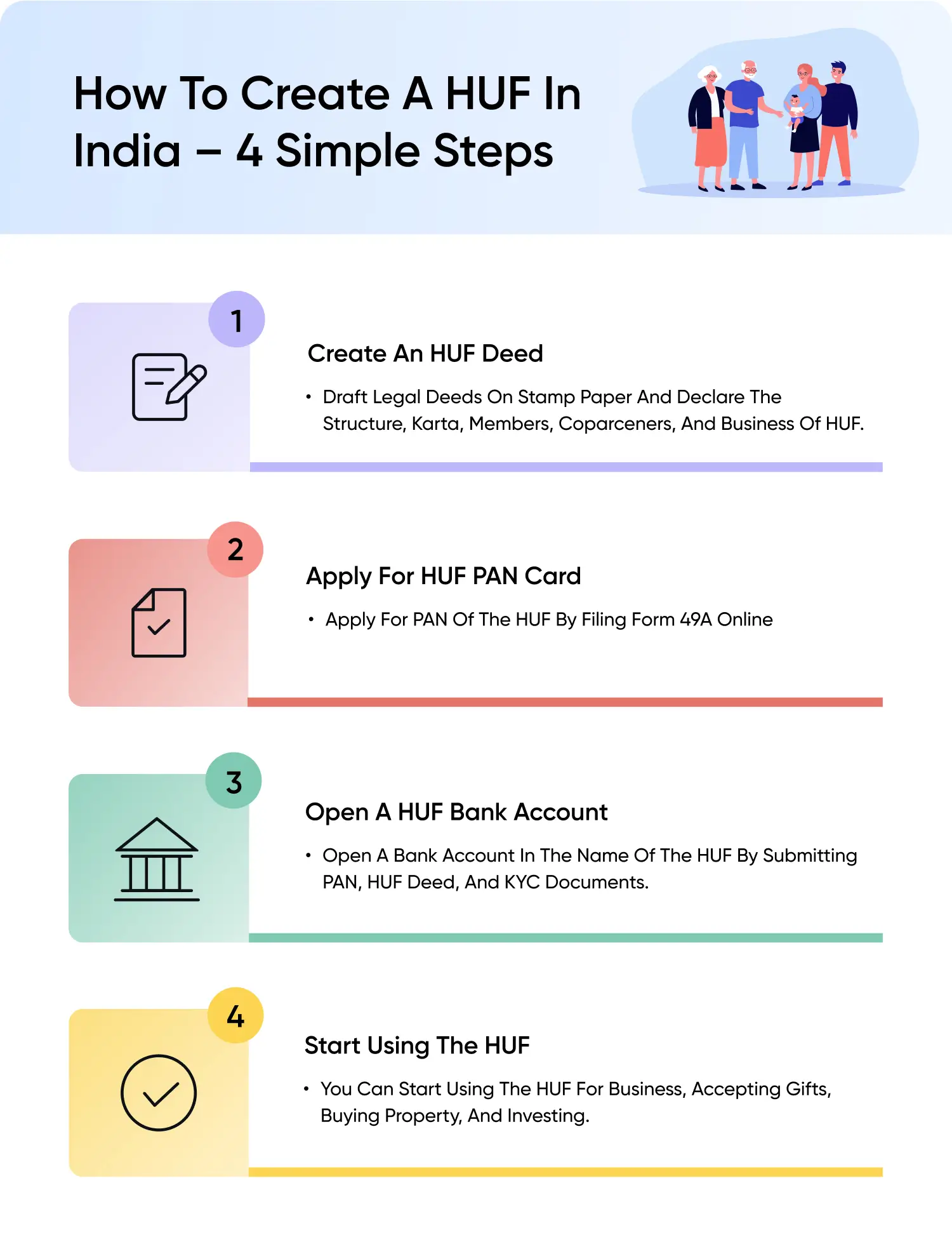

How to Form an HUF - A Step-by-Step Guide

Forming an Hindu Undivided Family (HUF) is simple and involves steps like creating an HUF deed, applying for an HUF PAN card, opening a bank account, and starting the operations of the HUF.

Step-1: Create an HUF Deed

- The first step to form an HUF is to draft a HUF deed.

- It should contain the name of the Karta, coparceners, their personal details, date of formation, amount and sources of HUF corpus, and other required details as the situation demands.

Step-2: Obtain a PAN Card

- PAN application for HUF can now be made online.

- Karta needs to make an application in form 49A along with other necessary declarations.

- Usually, digital PAN, or PAN number is generated within 48 hours of application.

Step-3: Open an HUF Bank Account

- With the PAN obtained, you can now apply for bank account in the name of HUF, in order to undertake all the transactions under the name of HUF.

- You have to submit HUF deed, PAN and other KYC documents to open a bank account in HUF.

Step-4: Transfer the Common Assets to HUF

- All the assets intended to be used under the name of HUF, including properties, liquid cash, deposits etc. can be transferred to the common pool of HUF.

How to save taxes using HUF?

The most beneficial feature of HUF from a tax perspective is that, the basic exemption limit, Chapter VI A deductions are considered separately for HUF. By forming a HUF and separating family income from the income of the individual, they can claim basic exemption limit, and deductions both under their PAN and the HUF's PAN.

Risks and Challenges of an HUF

Though HUF is a good tax saving strategy, the following are the disadvantages of forming an HUF:

- Partition disputes

- Complex compliance

- Limited applicability

- HUF cannot receive salary

Dissolution of an HUF

an Hindu Undivided Family (HUF) can be dissolved through partition, where the assets are distributed among the coparceners (family members with inheritance rights). This partition may be:

- Total Partition: All assets of the HUF are divided, and the HUF ceases to exist.

- Partial Partition: Only some assets are divided, and the HUF continues for the remaining assets.

For the partition to be legally valid, a partition deed must be drafted, stamped, and registered. The HUF’s PAN card is surrendered to the tax authorities to complete the dissolution process.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption