Rent Free Accommodation (RFA): Its Taxability And Valuation

As per the Income Tax Act, employees receiving rent-free accommodation (RFA)/concessional rate accommodation (CRA) from their companies are eligible to pay tax on RFA. This is because rent-free accommodation is a perquisite offered to an employee by an employer, which is taxable under the head of income 'Salaries', according to the IT Act.

Thus, it is essential to determine the valuation of rent-free accommodation as provided to an employee by his or her company. The valuation rules for this perquisite have changed recently, with effect from September 1, 2023. Continue reading this article for a complete guide of rent-free accommodation on the meaning, taxability, and recent changes made in the valuation.

What is Rent-Free Accommodation?

As the name suggests, rent-free accommodation is a residential arrangement allotted to an employee against zero (rent-free accommodation) or minimal rent (concessional rate accommodation). An employer offers this perquisite to certain employees. Rent-free accommodation can include a flat, guest house, hotel, service apartment, caravan, mobile home, and more.

Though employees need not pay rent or concessional rent for accommodation in a company-provided apartment, they must pay tax on this accommodation. This is because a company adds the provided perquisite to its employee's (taxpayer's) salary. Thus, an employee's total income is assessed, including all the perquisites (in this case, rent-free accommodation), which are taxable.

Types of Rent-Free Accommodation

There are two types of rent-free accommodation as offered by the central government, state government, private and other companies:

- Furnished Rent Free Accommodation

- Unfurnished Rent Free Accommodation

Rent-Free Accommodation Taxability

Taxability of RFA/CRA has undergone amendment recently and the changes are effective from September 1, 2023. Taxability depends on various factors such as type of employer, city in which accommodation is provided, salary of employee, etc. Here is the procedure for calculating income tax on rent-free accommodation as per accommodation type:

Unfurnished Rent-free Accommodation

In the case of unfurnished rent-free accommodation, the perquisite value is calculated as follows:

| Employer | City Population | New Rates (w.e.f. 01.09.2023) | Old Rates (Till. 01.09.2023) |

| Government | NA | License fee determined by the government | Same |

| Other than Government (Owned by Employer) | Upto 10 Lakh | 5% of Salary | 7.5% of Salary |

| 10 Lakh to 15 Lakh | 5% of Salary | 10% of Salary | |

| 15 Lakh to 25 Lakh | 7.5% of Salary | 10% of Salary | |

| 25 Lakh to 40 Lakh | 7.5% of Salary | 15% of Salary | |

| Above 40 Lakh | 10% of Salary | Salary |

For properties taken on lease by an employer, the value of perquisite is lower of:

(i) actual lease rental as paid by an employer or

(ii) 10% of an employee's salary (previously 15% of salary till August 31, 2023).

Furnished Rent-free Accommodation

Furnished rent-free accommodation includes modern amenities like television, furniture, air-conditioner, etc. In the case of such accommodation, if furniture is owned by employer an additional 10% of the actual price of the amenities is added as a perquisite. If furniture is hired by the employer then the actual hire charges are to be added as a perquisite.

Taxability of Hotel Accommodation as Provided by the Employer

When an employer offers housing to an employee for less than 15 days, it would not be taxable, if employer provides hotel accommodation for 15 days and above as RFA/CRA, the value of perquisite is computed as follows:

- 24% of the salary

- Actual charges payable or paid to the hotel (whichever is lower)

This is only applicable to permanent employees. Temporary employees sent to a location for project execution or accommodated at offshore sites do not count. Thus, the following requirement is applicable if an employee gets accommodation at a new place due to transfer while retaining existing accommodation:

- Perquisite will only be calculated for one accommodation with a lower value if the stay does not exceed 90 days.

- If the period exceeds 90 days, the perquisite will be charged for both accommodations.

It is to be noted that in any case of accommodation the actual rent paid by the employee to the employer shall be deducted from the value of perquisite as calculated in the ways mentioned above. The same applies to the amenities such as furniture, televisions, refrigerators etc. provided as a part of furnished accommodation also.

Rent-Free Accommodation Calculation Example

Here is a detailed illustration of the rent-free accommodation calculation procedure:

Let's assume Mr Prabhat is an employee of XYZ company. His posting is in Jamshedpur (approximately 16 lakh population), drawing a basic salary of Rs. 5,00,000, a dearness allowance of Rs. 50,000 (this forms the salary part that includes all retirement benefits), and Rs. 50,000 as commission totalling to Rs. 6,00,000 per annum and Rs. 50,000 per month. Prabhat also gets an unfurnished rent-free accommodation from the company in Jamshedpur. Now lets understand the taxability of the same for FY 23-24:

| Particular | From 01.04.2023 to 31.08.2023 | From 01.09.2023 to 31.03.2024 |

| Salary Per Month | 50,000 | 50,000 |

| No. of Months | 5 | 7 |

| Percentage of Salary | 10% of Salary | 7.5% of Salary |

| Value of Perquisite | 25,000 | 26,250 |

| (50,000*5*10%) | (50,000*7*7.5%) | |

| Total Value of Perquisite | 52,250 (To be included as perquisite in Salary Income) | |

If the new rate is applied to the whole year, i.e., 7.5% of Salary, then the value of the perquisite will be Rs. 45,000.

Valuation of Accommodation in Subsequent Years

If an employer provides accommodation by RFA/CRA to employee in subsequent years also after it is taxed once in earlier years, then in subsequent years the value of perquisite shall be as lower of the following:

(i) Value of Perquisite calculated for that year as per rules mentioned above.

(ii) Value of Perquisite for 1st Year * Cost Inflation Index of Subsequent Year / Cost Inflation Index of 1st Year

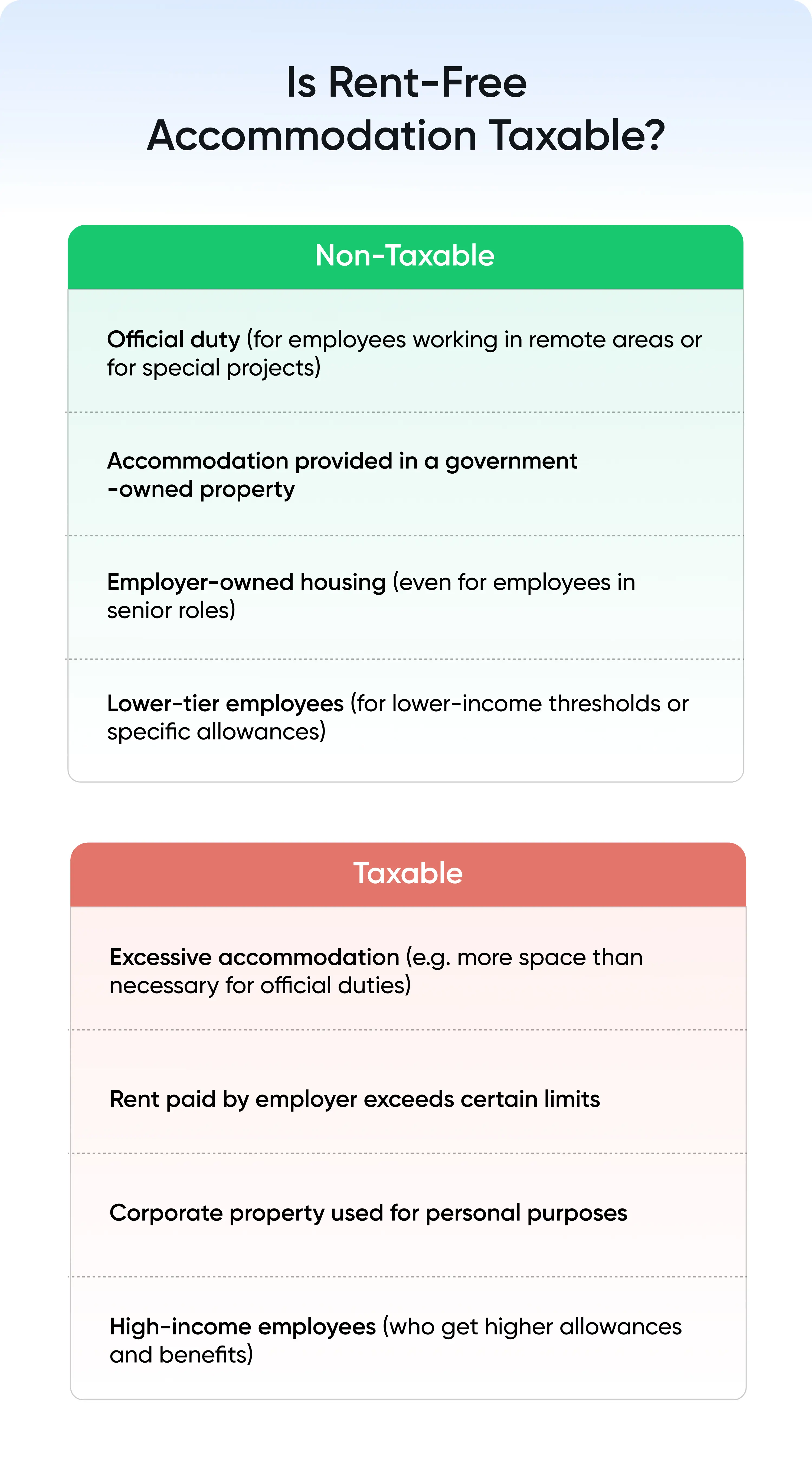

Tax Exemption on Rent-Free Accommodation

Check out the following situations that offer tax exemption on rent-free accommodation:

- If the accommodation is provided in a remote area, it is not taxable as per the law.

- When your company accommodates you in a hotel for less than 15 days due to your transfer, the perquisite value shall be eligible for tax exemption.

- If a rent-free accommodation is provided to a member of UPSC. In that case, Supreme Court Judge Union Minister, Parliament official, High Court Judge, Leader of Opposition in Parliament, etc., it does not come under taxable perquisite.

Conclusion

Though taxable, this perquisite is beneficial if your workplace is far from your house. Moreover, you can get tax exemptions on rent-free accommodations under certain circumstances. Thus, employees should know about this perquisite in detail to understand its taxability and valuation properly.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption