Call Now

Call Now

Set Off and Carry Forward of Losses

The Income Tax Act 1961 provides a valuable mechanism called Set-off and carried forward of Losses, which allows taxpayers to adjust losses incurred from various sources, such as business or profession, capital loss from shares and properties, interest paid on borrowed funds for house property, etc., against profit from the same or other eligible sources and also allow unutilised losses to be carried forward for future years, subject to certain conditions. These provisions are essential tools for reducing the overall tax liability and play a crucial role in effective and strategic tax planning.

Note: Under the New Tax Regime, the loss from House Property cannot be set-off against income from any other heads. Only intra-head set-off is allowed for losses from house property.

What Is Set Off of Losses?

- Set-off of losses means adjusting the losses against the profit or income of that particular year.

- Losses that are not set off against income in the same year can be carried forward to the subsequent years for set off against income of those years.

Simply speaking, it means utilising losses to reduce taxable income and save taxes.

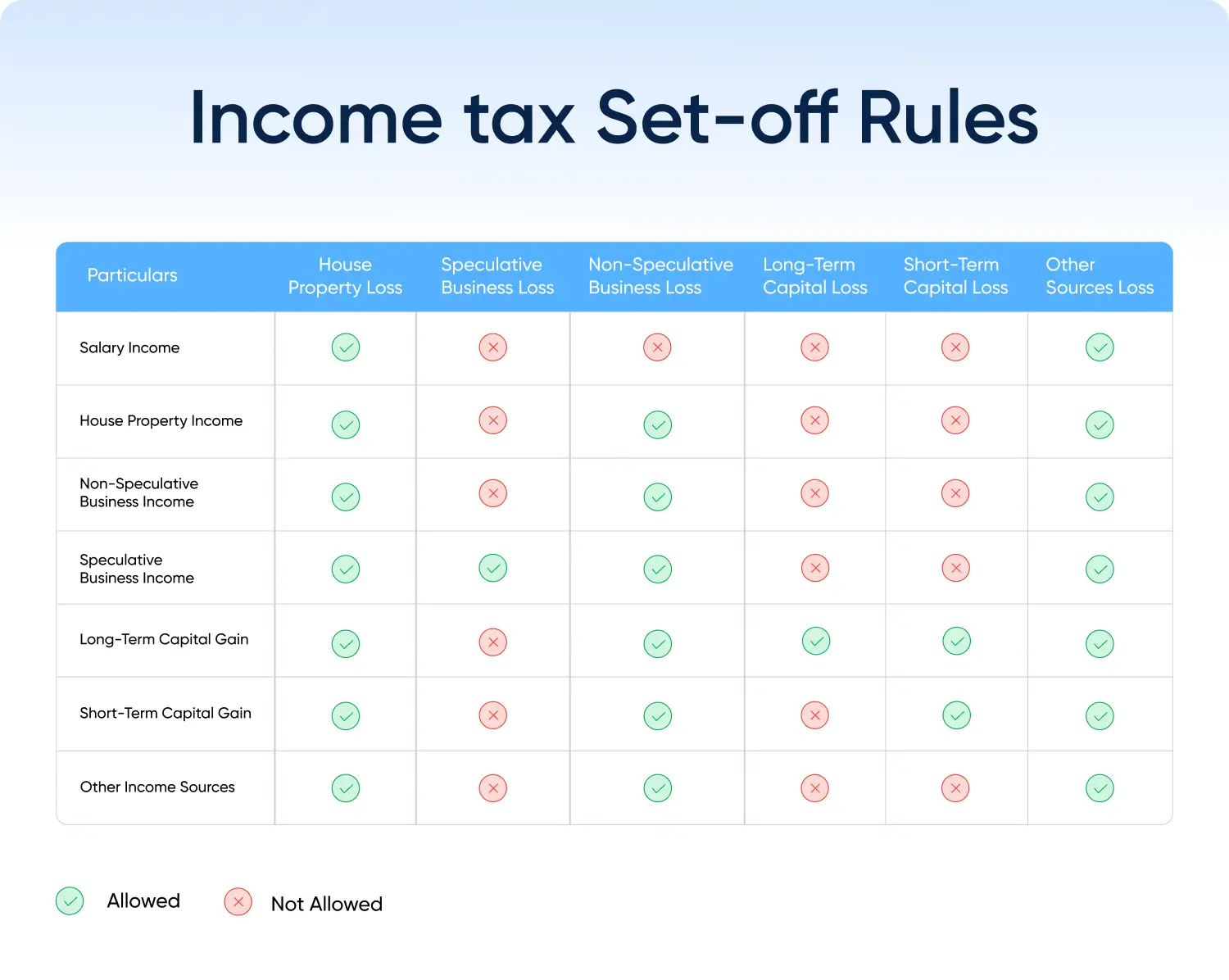

1. Intra-Head Set Off

The losses from one source of income can be set off against income under the same head of income, though sources might be different.

For eg: Loss from Business A can be set off against profit from Business B, where Business A is one source and Business B is another source under the common head of income is “Business”.

2. Inter-Head Set Off

After the intra-head adjustments, the taxpayers can set off remaining losses against income from other heads.

Given below are few restrictions for inter-head set off of losses:

- Loss from House property can be set off against income under any head up to a limit of Rs. 2 lakhs under the old tax regime only. No inter head set off allowed in new regime.

- Business loss other than speculative business can be set off against any head of income except income from salary.

Type of Loss | Can Be Set Off Against | Cannot Be Set Off Against |

Speculative Business Loss | Profit from speculative business | Income from other business or profession or any other income |

Loss from Owning & Maintaining Racehorses | Profit from the same activity (racehorses). | Any other income |

Long-term Capital Loss | Long-Term Capital Gains only | Short-Term Capital Gains or any other income |

Short-term Capital Loss | Both short-term and long-term capital gains | Any other income |

Loss from Specified Business | Profit from other specified businesses | Any non-specified business or profession or any other income |

Loss from Other Business or Profession | Profits from both specified and non-specified businesses | Salary Income |

| Loss from House Property | Set off allowed. | For Old regime: Any other head up to Rs.2 lakhs. For New Regime: Cannot be set off against any other income |

It is important to understand that any losses should first be set-off against the income from the same head. Such loss can only be set-off against incomes from other heads only when there is no income in the relevant head or the loss is more than the income under that head.

Carry Forward of Losses

After making the appropriate and permissible intra-head and inter-head adjustments, there could still be unadjusted losses. These unadjusted losses can be carried forward to future years for adjustments against income of these years. The rules as regards carry forward differ slightly for different heads of income.

1. Losses from House Property

- Can be carry forward up to next 8 assessment years from the assessment year in which the loss was incurred

- Can be adjusted only against Income from house property

- Can be carried forward even if the return of income for the loss year is filed under belated return.

- If individuals, HUF, AOP, BOI, opting to pay taxes under old tax regime, loss under the head income from house property firstly setoff against income from any other head to the extent of Rs 2,00,000 during the same year, unobserved loss will be carried forward to the following assessment year to be setoff against income under the head income from house property of future years.

- Under the new tax regime, loss under the head income from house property would not be allowed to be set off against income under any other head.

Let’s try to understand this with below example

Mr Rama aged 45 years submits the following income pertaining to the FY 2024-25

- Income from salary Rs 4,20,000

- Loss from let out property Rs -2,30,000

- Business Loss Rs -1,20,000

- Bank Interest received Rs 85,000

Computation of income under old tax regime

Particulars | Amount | Amount |

Income From Salary | 4,20,000 | |

Less: Loss from House Property of Rs. 2,30,000 but restricted to Rs. 2,00,000 | -2,00,000 | 2,20,000 |

Income From Other Sources | ||

Interest Income | 85,000 | |

Less: Business loss Rs. 1,20,000 but restricted to Rs. 85,000 | -85,000 | - |

Gross Total Income | 2,20,000 |

Note:- (a) The balance loss of Rs 30,000 from house property to be carried forward to next assessment year for set-off against income from house property of that year.

(b) Remaining business loss of Rs 35,000 will be carried forward as it cannot be set off against salary income and allowed for set-off against income from house property of that year.

Computation of income under New tax regime

Particulars | Amount | Amount |

Income From Salary | 4,20,000 | |

Income From Other Sources | ||

Interest Income | 85,000 | |

Less: Business loss Rs. 1,20,000 but restricted to Rs. 85,000 | -85,000 | - |

Gross Total Income | 4,20,000 |

Note : (a) loss from house property cannot be set off against income under any other head. Therefore, the entire loss of Rs 2,30,000 from house property to be carried forward to next assessment year for set-off against income from house property of that year.

(b) Remaining business loss of Rs 35,000 will be carried forward as it cannot be set off against salary income.

2. Losses from Non-Speculative Business (Regular Business) Loss

- The Loss should have been incurred in business

- Can be carried forward up to next 8 assessment years from the assessment year in which the loss was incurred

- Can be adjusted only against Income from business or profession

- Not necessary to continue the business at the time of set off in future years

- Cannot be carried forward if the return is not filed within the original due date.

- Person who incurred the loss alone is entitled to carry forward & set-off the loss (it can not transferred to any other person)

3. Speculative Business Loss

- Can be carry forward up to next 4 assessment years from the assessment year in which the loss was incurred

- Can be adjusted only against Income from speculative business

- Cannot be carried forward if the return is not filed within the original due date.

- Not necessary to continue the business at the time of set off in future years

4. Specified Business Loss under 35AD

- No time limit to carry forward the losses from the specified business under 35AD

- Not necessary to continue the business at the time of set off in future years

- Cannot be carried forward if the return is not filed within the original due date

- Can be adjusted only against Income from specified business under 35AD

- Not necessary to continue the business at the time of set off in future years

5. Capital Losses

- Can be carry forward up to next 8 assessment years from the assessment year in which the loss was incurred

- Long-term capital losses can be adjusted only against long-term capital gains.

- Short-term capital losses can be set off against long-term capital gains as well as short-term capital gains

- Cannot be carried forward if the return is not filed within the original due date

Let us understand with an example-

Mr P has invested in equity shares. Below are the details related to his capital gain/loss transactions for different years.

A.Y. | STCL during the year | LTCL during the year | STCG during the year | LTCG during the year | STCG taxable | LTCG taxable | Balance STCL and LTCL to be c/f |

2020-21 | 3,000 | 1,000 | - | - | - | - | STCL- 3,000 LTCL- 1,000 |

2021-22 | - | 1,300 | 5,600 | - | 2,600 (5,600- 3,000) Set-off against LTCL | - | STCL- Nil LTCL- 2,300 |

2022-23 | 800 | - | - | 7,000 | - | 3,900 (7,000- 2,300- 800) Set-off against STCL and LTCL | STCL- Nil LTCL- Nil |

2023-24 | 1,200 | 4,000 | 3,000 | 9,000 | 3,000* | 3,800* (9,000- 4,000- 1,200) Set-off against STCL and LTCL | STCL- Nil LTCL- Nil |

* The order of adjusting STCL and LTCL is not prescribed in the Act. Hence, the STCL and LTCL are first adjusted with LTCG of the year to reduce the tax liability.

6. Losses from Owning and Maintaining Race-Horses

- Can be carry forward up to next 4 assessment years from the assessment year in which the loss was incurred

- Cannot be carried forward if the return is not filed within the original due date

- Can only be set off against income from owning and maintaining race-horses only

Note:

- A taxpayer incurring a loss from a source, income from which is otherwise exempt from tax, cannot set off these losses against profit from any taxable source of Income

- Losses cannot be set off against casual income i.e. crossword puzzles, winning from lotteries, races, card games, betting etc.

Loss From Exempt Source of Income

It must be noted that Losses from Exempt sources cannot be set off against profit from taxable income or exempt income from a different source or head, and they are also not eligible to be carried forward. Since exempt income is not chargeable to tax, any loss from an exempt source is also not eligible to be set off and carried forward.

Illustration

- Mr. A is an active partner in a partnership firm. He has received a share of profit from the firm in previous years. However, for the first time, he incurred a loss from the firm in Financial Year 2023–24.

- In the following year, i.e., FY 2024–25, he again earned a share of profit.

- As per Section 10(2A) of the Income Tax Act, the share of profit received by a partner from a partnership firm is exempt from tax in the hands of the partner.

- Now, since Income from the partnership firm is exempt, the loss incurred in FY 2023-24, is also considered as loss from an exempt source and such a loss cannot be set-off against Mr.A income from other business activity,house property, income from other sources, even the profit from partnership firm in FY 2024-25. Additionally loss from partnership firm (loss from exempt source) can not be carried forward to the future in his personal return.

Section | Losses to be Carried Forward | Can be Set off against Income | Time up to which losses can be Carried Forward | Mandatory to file return in the year of loss before the due date? |

32(2) | Unabsorbed depreciation | Any income (other than salary) | No time limit | No |

71B | Loss from House property | Income from house property | 8 years | No |

72 | Loss from Normal business | Income from business | 8 years | Yes |

73 | Loss from speculative business | Income from speculative business | 4 years | Yes |

73A | Loss from specified business | Income from specified business | No time limit | Yes |

74 | Short term capital loss (STCL) | Short term capital gain (STCG) and long term capital gain (LTCG) | 8 years | Yes |

Long term capital loss (LTCL) | LTCG | 8 years | Yes | |

74A | Loss from owning and maintaining horse races | Income from owning and maintaining horse races | 4 years | Yes |

Set-off Rules for Stock Market Losses

| Loss Type | Current Year Set-off | Future Set-off | Carry Forward |

| F&O | Business income & eligible other heads (except salary) | Business income | 8 Years |

| Intraday | Speculation income | Speculation income | 4 Years |

| STCL | STCG & LTCG | STCG & LTCG | 8 Years |

| LTCL | LTCG | LTCG | 8 Years |

Related Articles

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption