Call Now

Call Now

Section 269ST of Income Tax Act - Clarification on the repayment of Loan Instalments in Cash

Section 269ST was introduced by the government to curb the black money and tax fraud in the economy. Under the section, cash transactions exceeding Rs.2 lakh are prohibited with a view to promoting the digital economy. From now on, the courts and sub registrar offices should report cash transactions not less than Rs.2 lakhs to the respective jurisdictional Income Tax Offices as per the recent Supreme Court Judgement.

The recent Supreme Court ruling highlights the importance of section 269ST in the case RBANMS Educational Institution Vs B Gunashekar on 16th April, 2025.

The case pertains to a property dispute, in which one of the parties received a cash advance of Rs. 75 lakhs. The Supreme Court indicated that the aforesaid receipt by the party is a plain violation of section 269ST, as the transaction has very well exceeded the limit of Rs. 2 lakhs. The payer of the advance was also liable to explain the need for paying a hefty amount in cash and the source of the same.

In light of the government's goal to achieve transparency in financial transactions and promote the digital economy,

- Wherever any suit is filed with a claim of Rs. 2 lakhs or above

- Wherever any sum of Rs 2 lakhs or above is payable related to a transaction in an immovable property,

the respective Courts or the Sub-Registrar office, as the case may be, should report the transactions to the Jurisdictional Income Tax officers about the details of the transactions. The latter should consider the same and verify whether the grounds of violating section 269ST apply to such transactions.

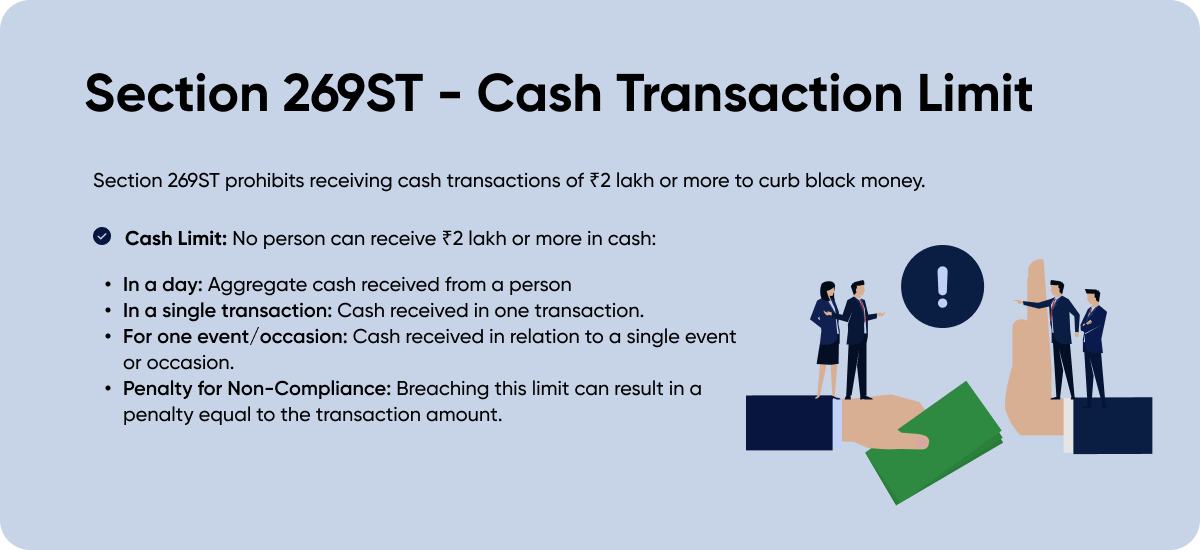

What is Section 269ST?

Section 269ST prohibits any person to receive an amount of Rs.2 lakh and above in cash:

- In aggregate from a person in a day, or

- In a single transaction, or

- In respect of transactions relating to one event or occasion from a person.

Exemptions From the Scope of Section 269ST

The provisions section 269ST is applicable to all the taxpayers, excluding the exceptions below:

- Government

- any banking company

- post office savings bank

- co-operative bank

- other persons/receipts as may be notified

- Transactions referred to in section 269SS (attracted when we accept loan from any person) will be excluded from the scope of the new section 269ST.

Section 269ST of Income Tax Act With Examples

- If one sells goods worth Rs 4.5 lakh through three different bills of Rs.1.5 lakh each to one person and accepts cash in 1 single day at different times then section 269ST(a) will get violated.

- If one sells goods worth Rs 5 lakh through a single bill (single transaction) to another person and receives cash of 2.5 lakh on day 1 and another 2.5 lakh on day 2 then section 269ST(b) will get violated.

- X accepts an order of catering, decoration and tent for the marriage event of Y. He accepts cash of Rs.1 lakh for catering Rs 1.5 lakh for decoration and Rs.1.5 lakh for tent work then section 269ST(c) will get violated even if cash is accepted on different dates. All the cash transactions related to the same occasion- the marriage of Y.

In all three cases, section 269ST gets violated and penalty u/s 271DA is applicable.

Repayment of Loan Instalments – Section 269ST

- After introducing this section, various representations were sent by NBFCs and HFCs as to whether the limit of Rs.2 lakh shall apply to one instalment of loan repayment or for the whole amount of such repayment.

- In this context, the income tax department clarified that if you are repaying the loan to NBFCs or HFCs, the one instalment of loan repayment shall constitute a single transaction.

- And so if the single loan instalment amount is less than Rs.2 lakh, it can be paid in cash. All the instalments paid for a loan shall not be aggregated for the purposes of determining the applicability of the Rs.2 lakh limit.

Introduction of Penal Provisions

- The government has also introduced penalty provisions if Section 269ST is violated.

- If a person receives the amount in cash over the above-specified limit of Rs.2 lakh, he is liable to pay a penalty equal to the amount received in cash.

- Thus, it is very important to ensure that you do not receive cash of Rs.2 lakh and above in a single transaction, aggregate from a person in a day, or in respect to transactions relating to one event or occasion from a person.

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption