|

Drawbacks of Registering under the GST Composition Scheme

The GST Composition Scheme is extremely important for those traders who have a turnover below Rs. 1.0 crore* annually. While it has its benefits, there are also several drawbacks of registering under the GST Composition Scheme, and that will be addressed in this article.

*CBIC has notified the increase to the threshold limit from Rs 1.0 Crore to Rs 1.5 Crores from 1st Feb 2019.

In our previous article, we elaborated on why a taxpayer should choose to get himself registered under section 10 of the GST law, which provides the benefit of limited compliance and lower tax rates for small taxpayers.

Latest Updates on Composition Scheme

5th July 2022

(a) The due date of GSTR-4 for FY 2021-22 is further extended by a late fee waiver up to 28th July 2022 vide Notification 12/2022 dated 5th July 2022.

(b) The due date of CMP-08 for April-June 2022 is extended up to 31st July 2022 vide Notification 12/2022 dated 5th July 2022.26th May 2022

As per the CGST Notification no.7/2022 dated 26th May 2022, the late fee has been waived for the delay in filing GSTR-4 for FY 2021-22, if it is filed between 1st May and 30th June 2022.24th February 2022

Composition taxable persons and those interested to opt into the scheme for FY 2022-23 must submit a declaration on the GST portal in Form CMP-02 by 31st March 2022.28th May 2021

As per the outcome of the 43rd GST Council meeting and CBIC notification,

(1) Interest relief has been provided for filing of CMP-08 for Jan-March 2021 quarter as per which, for any delay, interest is not charged until 3rd May, whereas 9% of reduced interest will be charged if filing is done thereafter until 17th June, and 18% later on.

(2) The due date to file GSTR-4 for FY 2020-21 is extended up to 31st July 2021.

(3) The maximum late fee for GSTR-4 that can be charged will be restricted to Rs.500 per return for nil filing and Rs. 2000 for other than nil filing.1st May 2021

(1) The due date to file GSTR-4 for FY 2020-21 was extended from 30th April 2021 to 31st May 2021.

(2) Form CMP-08 that was due by 18th April 2021 for January-March 2021 has been given a relaxation in the interest charges. No interest for filing on or before 8th May, interest reduced to 9% between 9th May and 23rd May, but charged at 18% thereafter.

(3) The time limit to file ITC-03 by newly opted composition taxable persons for FY 2021-22 is extended up to 31st May 2021.

Drawbacks of Registering under the GST Composition Scheme

Limited Territory for Business: A taxpayer registered under the composition scheme is barred from carrying out inter-state sales and cannot offer import-export of goods and services. Thus, he is compelled to carry out only intra-state transactions and this limits the territory of his business. Furthermore, this section limits the benefit only to the boundary of the state.

No Credit of Input Tax: There has been no provision of input credit on B2B transactions. Thus, if any taxable person is carrying out business on B2B model, such person will not be allowed the credit of input tax paid from the output liability. Also, the buyer of such goods will not get any credit on tax paid, resulting in price distortion and cascading.

This will further result in a loss of business as a buyer registered as a normal taxpayer will not get any credit when buying from a person registered under composition scheme. Eventually, such buyers might avoid purchases from a taxpayer under composition scheme.

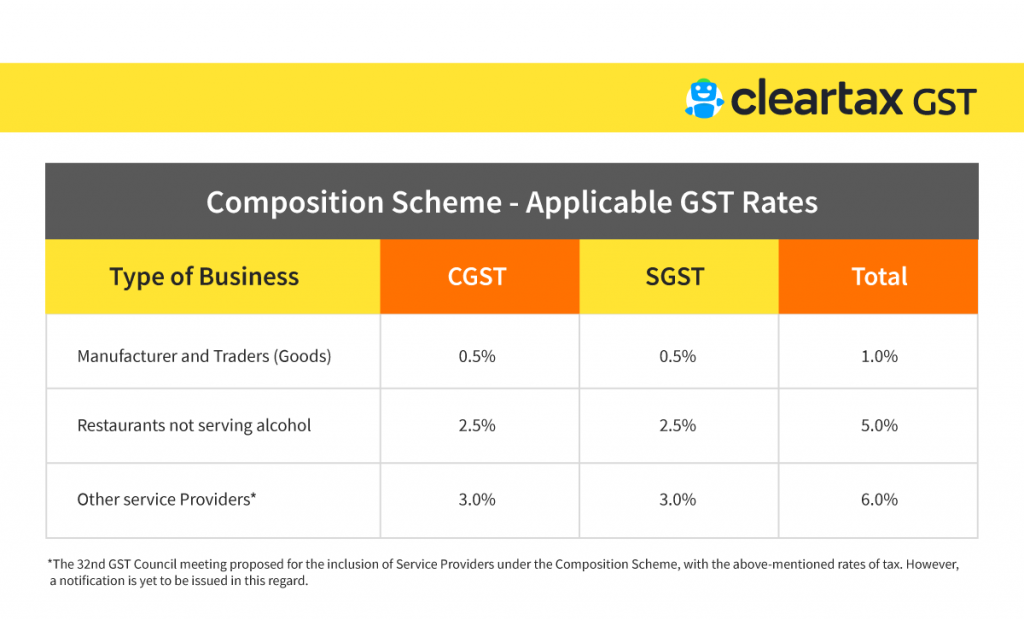

No Collection of Tax: Though the rate of composition tax is kept very nominal at 1% or 5%, a taxpayer under composition scheme is not allowed to recover such tax from his buyer, as he is not allowed to raise a tax invoice

As per notification 01/2018 dated 01.01.2018, turnover for traders has been defined as ‘ Turnover of taxable supplies of goods’.

Consequently, the burden of such tax is kept on the taxpayer himself and this has to be paid out of his own pocket. Thus the fundamental principle of limited compliance and tax burden on small taxpayer is defeated here.

Penal Provision: Another provision which is heavily debated is the penal provision for a taxpayer under composition scheme. As per the GST Law, if the taxpayer who has previously been given registration under composition scheme is found to be not eligible for the composition scheme or if the permission granted earlier was incorrectly granted, then such taxpayer will be liable to pay the differential tax along with a penalty which can extend up to the amount of total tax liability i.e 100%.

On analysis of this provision, it can be fairly said that if a small taxpayer who has limited knowledge of tax laws and compliance makes any mistake under composition scheme, he shall be liable to pay tax at the standard rate on his total turnover along with a penalty which will be equal to the total tax liability.

Electronic Commerce out of scope: One of the major industries which has flourished in recent times, is the e-commerce in India. There have been numerous companies who are into e-commerce, some of them have turnover into crores, however many of them are still at nascent stage and have not achieved breakeven as well. Such units carry out their business online through internet and supply across states.

Since they are into inter-state supplies they are not eligible for composition scheme and thus the benefit of this section has been kept away from them. This is further in contradiction with the government vision of “Digital India” and “Startup India” which are aimed to promote the startup ecosystem and digital experience for Indian citizens.

Not applicable to the supplier supplying goods through E-commerce

Composition scheme is considered instrumental in enabling small taxpayers to reduce the burden of compliance. However, under the current scenario, a small taxpayer has to act very consciously if he chooses to get registered under the composition scheme.

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption