Call Now

Call Now

A Complete Guide on Taxation of Interest on EPF Contribution Exceeding Rs 2.5 lakh

The interest earned on the EPF contribution by the employees is generally exempt from tax. However, in Budget 2021 it was proposed to make the interest earned on the PF contributions exceeding Rs. 2,50,000 in a financial year taxable. However, for government employees this limit is Rs. 5 lakh.

Read this article to understand more about the taxability of interest on EPF contributions.

EPF Interest Rate FY2025-26:

EPF Interest Rate for FY 2025-26 has Retained at 8.25%

What is EPF?

Employee Provident Fund (EPF) is a retirement benefits scheme for salaried employees. The Employees Provident Fund Organisation (EPFO) manages this scheme. Every factory/organisation having 20 or more employees must register under the EPFO. Some organisations with fewer than 20 employees can obtain EPF registration voluntarily.

All employees, including regular and contractual workers, whose wages are up to Rs 15,000 should be enrolled in the EPF by the organization.

After registration, the employee needs to contribute to the fund and the employer will also make a matching contribution. The employees cannot register for EPF on their own. So if the employee who is drawing a salary more than Rs 15,000 wishes to contribute to EPF account, they can do so with the consent of their employer.

Latest Update on Withdrawal Limit

To ensure quicker access of funds to its members, the EPFO has announced that the threshold limit for auto-settlement for advance claims has been increased from Rs. 1 lakh to Rs. 5 lakh.

Some Important Features of the EPF Scheme

The following are some of the important features of the EPF Scheme:

- The employee should make EPF contributions of Rs 1,800 or 12% on the basic salary and the dearness allowance, whichever is lower. Most companies deduct 12% of salary + DA.

- The employer must also make an equal contribution to the EPF account.

- However, the EPF contributions are payable at a maximum wage ceiling of Rs 15,000 per month. Therefore, some employers make the minimum contribution of Rs 1,800 per month (12% of Rs 15,000) to increase the in-hand salary of the employee. However, most employers choose to contribute 12% of basic salary + DA.

- The employee can contribute at a higher rate via VPF (voluntary provident fund), but the employer is not under any obligation to match contributions above 12% of basic salary + DA.

- The interest on the PF contribution is credited to the PF account at the end of the financial year. The EPF interest rates are fixed by the government each year.

- Usually, interest is credited to the EPF account after the financial year has ended.

- As per the EPFO guidelines, an organisation with less than 20 employees has to make an EPF contribution of 10% instead of 12%.

- After retirement, the employee will get a lump-sum retirement amount, which includes the contributions of both the employee and the employer with interest accrued.

What is VPF?

An employee can voluntarily enhance the monthly PF contribution up to 100% of the basic salary as a Voluntary Provident Fund (VPF). The employer is under no obligation to match this excess contribution (beyond 12% of the basic salary + DA). This amount would be credited to the same EPF account as there is no separate account for VPF, and the interest offered would be the same as EPF.

What are the Taxation Rules for Income from EPF Contributions?

Tax on interest credited to EPF account

After Budget 2021, interest on an employee’s contribution to an EPF account above Rs 2.5 lakh during the financial year is taxable in the hands of the employee. This interest is also subject to TDS.

This rule will only apply to the contributions made by the employee, while contributions made by the employer will not be taxed. The calculation of interest on the threshold limit of Rs 2.5 lakh shall also include VPF contributions.

For example, an employee’s basic salary (no dearness allowance) is Rs 50,000 per month. The employer deducts 12% of the employee’s basic salary, i.e., Rs 6,000 towards EPF contribution. However, the employee voluntarily contributes Rs 3.28 lakh in VPF during the financial year. Hence, the employee’s total EPF contribution during the financial year will be Rs 4 lakh (Rs 6,000 x 12 + Rs 3.28 lakh).

The employee will be required to pay tax on interest accrued/earned on the excess contribution of Rs 2.5 lakh [Rs 72,000(EPF) + Rs 3.28 lakh(VPF) – Rs 2.5 lakh].

In the case of government employees who contribute to GPF, the threshold of Rs 2.5 lakh has been raised to Rs 5 lakh. That is to say interest on GPF contribution in excess of Rs 5 lakh will be taxable for the employee.

Before FY 2021-22, the interest credited to the EPF account on any amount of contribution was tax-free. Now a cap of Rs 2.5 lakh has been introduced, interest on contributions beyond this shall be taxable.

Tax Deduction on Contribution to EPF Account

An employee’s contribution to the EPF account is allowed as a deduction up to Rs 1.5 lakh under Section 80C of the IT Act.

From FY 2020-21 onwards, the employer’s contribution to the EPF account shall become taxable if the contribution to EPF, NPS and/or superannuation fund exceeds Rs 7.5 lakh in a financial year. The excess contribution will become taxable. The employer needs to calculate the amount that will be taxed as a prerequisite, and this will be reflected in the employee’s Form 16.

Effective Date

This amendment has got applicable from 1st April 2021. It means the interest on the employee’s EPF contributions above Rs 2.5 lakh shall be taxable for the FY 2024-25 also.

How to Calculate the Taxable Portion of EPF interest?

As per notification No. 95/2021 dated 31st August 2021, for calculating taxable interest, the PF department shall maintain separate accounts, one with taxable contribution and another with non-taxable contribution, for all the subscribers starting from the financial year 2021-22 and onwards.

The taxpayer shall be liable to pay tax on the interest accrued in the taxable contribution account. The EPFO shall deduct TDS on such interest.

Under what Circumstances will TDS on interest be deducted?

TDS will be deducted at 10% on taxable interest income accrued above the threshold limit during the year as per Section 194A of the IT Act.

What is the Threshold Limit on Interest income above which TDS will be deducted?

For resident Indians, TDS is deductible if the interest accrued in the PF account for the financial year exceeds Rs 5,000.

However, for non-residents, there is no threshold limit. Tax is deductible even if the interest income for the year is less than Rs 5,000.

Do Employees need to Pay tax if TDS is deducted?

The employee shall pay tax on the interest accrued on the taxable portion of the PF contribution. The amount of taxable PF interest should be added as income under the head ‘income from other sources’ on which tax shall be calculated as per the applicable income tax slab rates. The employee can claim a tax credit for the TDS deducted from the interest income.

To know the amount of taxable PF interest, the employee can view the PF account statement. To know how to view the PF account statement, click here.

The New TDS Rule

The new TDS rule shall apply to all the below:-

- Exempted establishments

- Unexempted establishments

- Exempted trusts

- In the case of the death of PF members

- International workers

When will the TDS be Deducted?

TDS on the taxable interest of the PF account shall be deducted in the following scenarios-

- At the time of processing the annual accounts of EPFO,

- PF payment during the year to outgoing members on a final settlement,

- Transfer claims for transfer from exempted establishments to EPFO and vice versa,

- Transfer claims for transfer from one trust to another, and

- Transfer of past accumulations.

Who is Liable to deduct TDS on Taxable PF interest?

The TDS on taxable interest on the PF account shall be deducted as per Section 194A of the Income Tax Act. The law states that the payer of the income should deduct TDS. Hence, the payer of interest on the PF account is the provident fund department and not the employer. Therefore, TDS will be deducted by EPFO and deposited to the government. Further, the EPFO will issue Form 16A for the same.

What is the Date of TDS Deduction on Taxable PF interest?

The new TDS rule will apply to the government and private sector employees on contributions from the financial year 2021-22 and subsequent years. No TDS will be applicable on past accumulation till 31st March 2021. It will be applicable to contributions made from 1st April 2021, which exceed the threshold limit of Rs 2.5 lakh.

If the case does not include a final settlement or transfer, the PF department will deduct tax at source (TDS) on the date of credit of interest on the EPF account. The PF department credits interest in the PF account at the end of the financial year.

In any other case such as final settlement, transfer claims, on transfer from EPFO to exempted establishments, and vice versa, the TDS shall be deducted either on 1st April 2024 or on final settlement or on the transfer date, whichever is later.

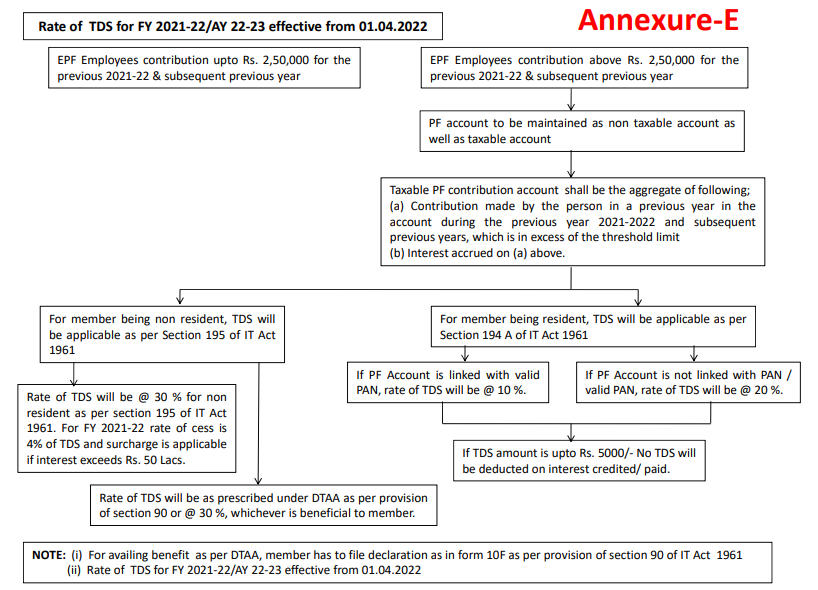

What is the Rate of TDS deduction on Taxable interest on EPF Contributions?

- For resident Indians-

If PF account is linked with a valid PAN, then TDS rate will be 10%.

If PF account is not linked with PAN, then the TDS rate will double to 20%.

However, for resident Indians, the TDS will be deducted only if the interest amount exceeds Rs 5,000.

- For non-residents

The TDS will be deducted at 30%, and it shall be deducted under Section 195 of the Income Tax Act. However, if the rate of TDS specified under the Double Taxation Avoidance Agreement (DTAA) is beneficial to PF members, then such a rate will be applicable. The TDS rate is also 30% if the PF account is not linked with PAN.

There is a 4% cess of TDS amount and surcharge applicable to non-residents. However, a cess of 4% and a surcharge will not be applicable if the TDS is deducted as per DTAA provisions.

For the FY 2023-24, the applicable surcharge rates on NRIs’ interest income are specified below:

- Interest income below Rs 50 lakh – No Surcharge

- Interest income above Rs 50 lakh to Rs 1 crore – 10%,

- Interest above Rs 1 crore to Rs 2 crore – 15%,

- Interest above Rs 2 crore to Rs 5 crore – 25%

- Interest above Rs 5 crore – 37%

Note: The surcharge will be limited to 25% if he opts to pay tax under the new regime.

How will non-resident members claim to benefit from double taxation on taxable interest?

To avail of DTAA benefits, the member must obtain a Tax Residency Certificate (TRC) by filing Form 10F to the income tax department. On receipt application in Form 10F, the Assessing Officer may issue a TRC in Form 10FB on being satisfied on this behalf. Based on such TRC, the non-resident member can claim the benefit from double taxation.

What if there is interest-on-interest from the excess PF contribution? Will it be taxed in future years too?

As per the current accounting system followed by EPFO, interest is credited on an annual basis. The government notifies the EPF interest rates at the end of the relevant financial year. If the EPF and VPF contribution is more than Rs 2.5 lakh during the financial year, the TDS needs to be deducted from the interest accrued on the taxable portion of the PF contribution.

In the subsequent years, the previous years’ accumulations of the taxable account will be brought forward, and the interest accrued on the opening balance and current years’ contribution (contribution above the threshold limit of Rs 2.5 lakh) of the taxable account shall be taxable.

The interest accrued on the brought forward balance of a non-taxable account will be exempt from tax.

Illustration

Illustration 1- Normal scenario

Mr Q is a salaried employee who contributes Rs 30,000 monthly to the EPF account. The closing balance of his PF account as of 31st March 2023 is Rs 50,00,000.

The calculation of taxable and non-taxable PF interest will be as under:

Period (FY 2023-24) | Monthly contribution (Rs.) | Cumulative balance at the end of the month | Interest accrued at 8.25% in | ||

|---|---|---|---|---|---|

Non-taxable account (Rs) | Taxable account (Rs) | Non-taxable account (Rs) | Taxable account (Rs) | ||

April | 30,000 | 30,000 | 0 | 206 | 0 |

May | 30,000 | 60,000 | 0 | 413 | 0 |

June | 30,000 | 90,000 | 0 | 619 | 0 |

July | 30,000 | 1,20,000 | 0 | 825 | 0 |

August | 30,000 | 1,50,000 | 0 | 1,031 | 0 |

September | 30,000 | 1,80,000 | 0 | 1,238 | 0 |

October | 30,000 | 2,10,000 | 0 | 1,444 | 0 |

November | 30,000 | 2,40,000 | 0 | 1,650 | 0 |

December | 30,000 | 2,50,000 | 20,000 | 1,719 | 138 |

January | 30,000 | 2,50,000 | 50,000 | 1,719 | 344 |

February | 30,000 | 2,50,000 | 80,000 | 1,719 | 550 |

March | 30,000 | 2,50,000 | 1,10,000 | 1,719 | 756 |

Balance as on 31.03.24 |

| 2,50,000 | 1,10,000 | 14,300 | 1,788 |

TDS would be deducted as per the below working:

Particulars | Non-taxable account | Taxable account |

|---|---|---|

Carried forward balance as on 31.03.2023 | 50,00,000 | 0 |

Interest accrued on opening balance | 4,125,00 | 0 |

Total contribution during the FY 2023-24 | 2,50,000 | 1,10,000 |

Interest accrued during the FY 2023-24 | 14,300 | 1,788 |

Total amount in the accounts to carry forward next year | 56,76,800 | 1,11,788 |

TDS @10% (1788 x 10%) | 0 | 179 |

Opening balance as on 01.04.2024 | 56,76,800 | 1,11,788-179 |

We can see that TDS at 10% is deducted on the interest amount of Rs 1,788 accrued in the taxable account.

If the member’s PAN is not linked to the PF account, TDS should be deducted at 20%.

Illustration 2- If funds withdrawn from the PF account

When the member withdraws any amount from the EPF account, firstly, the funds will be withdrawn from the taxable account and thereafter from the non-taxable account.

Let’s calculate the taxable and non-taxable portion of the PF account interest, and TDS calculation.

FY 2023-24

Period (FY 2023-24) | Monthly contribution (Rs) | Cumulative balance at the end of the month | Interest accrued at 8.25% in | ||

|---|---|---|---|---|---|

|

| Non-taxable account (Rs) | Taxable account (Rs) | Non-taxable account (Rs) | Taxable account (Rs) |

April | 40,000 | 40,000 | 0 | 275 | 0 |

May | 40,000 | 80,000 | 0 | 550 | 0 |

June | 40,000 | 1,20,000 | 0 | 825 | 0 |

July | 40,000 | 1,60,000 | 0 | 1,100 | 0 |

August | 40,000 | 2,00,000 | 0 | 1,375 | 0 |

September | 40,000 | 2,40,000 | 0 | 1,650 | 0 |

October | 40,000 | 2,50,000 | 30,000 | 1,719 | 206 |

November | 40,000 | 2,50,000 | 70,000 | 1,719 | 481 |

December | 40,000 | 2,50,000 | 1,10,000 | 1,719 | 756 |

January | 40,000 | 2,50,000 | 1,50,000 | 1,719 | 1,031 |

Withdrawal |

| -1,10,000 | -1,50,000 |

|

|

February | 40,000 | 1,80,000 | 0 | 1,238 | 0 |

March | 40,000 | 2,20,000 | 0 | 1,513 | 0 |

Balance as on 31.03.24 |

| 2,20,000 | 0 | 15,400 | 2,475 |

We can see that the withdrawals from the PF account was first fully adjusted from the taxable account and then from the non-taxable account.

TDS would be deducted as per the below working:

Particulars | Non-taxable account | Taxable account |

|---|---|---|

Carried forward balance as on 31.03.2024 | 50,00,000 | 0 |

Interest accrued on opening balance | 4,12,500 | 0 |

Total contribution during the FY 2024-25 | 3,30,000 | 1,50,000 |

Withdrawals during the FY 2024-25 | -1,10,000 | -1,50,000 |

Interest accrued during the FY 2024-25 | 15,400 | 2,475 |

Total funds in the accounts to carry forward next year | 56,47,900 | 2475 |

TDS @10% (2,430 x 10%) | 0 | 247 |

Balance carried forward to next year | 56,47,900 | 2,430-247 |

Taxable Interest calculation for the next year.

In the next financial year, if the employee continues to contribute Rs 40,000 monthly to the PF account, i.e. FY 2024-25, and withdraws Rs 4 lakh in June 24, the taxable interest would be calculated in the following manner:

(Assumption: 8.25 % interest rate for the FY 2024-25)

FY 2024-25

Period (FY 2024-25) | Monthly contribution (Rs) | Cumulative balance at the end of the month | Interest accrued at 8.25% in | ||

|---|---|---|---|---|---|

|

| Non-taxable account (Rs) | Taxable account (Rs) | Non-taxable account (Rs) | Taxable account (Rs) |

April | 40,000 | 40,000 | 0 | 275 | 0 |

May | 40,000 | 80,000 | 0 | 550 | 0 |

June | 40,000 | 1,20,000 | 0 | 825 | 0 |

| (As per below working) | -1,20,000 | 0 | 0 | 0 |

July | 40,000 | 40,000 | 0 | 275 | 0 |

August | 40,000 | 80,000 | 0 | 550 | 0 |

September | 40,000 | 1,20,000 | 0 | 825 | 0 |

October | 40,000 | 1,60,000 | 0 | 1,100 | 0 |

November | 40,000 | 2,00,000 | 0 | 1,375 | 0 |

December | 40,000 | 2,40,000 | 0 | 1,650 | 0 |

January | 40,000 | 2,50,000 | 30,000 | 1,719 | 203 |

February | 40,000 | 2,50,000 | 70,000 | 1,719 | 473 |

March | 40,000 | 2,50,000 | 1,10,000 | 1,719 | 743 |

Balance as on 31.03.25 |

| 2,50,000 | 1,10,000 | 14,300 | 1,788 |

Calculation of total interest accrued during the year:

Particulars | Non-Taxable account | Taxable account | ||

|---|---|---|---|---|

| Opening Balance (Rs) | During the year transactions (Rs) | Opening Balance (Rs) | During the year transactions (Rs) |

EPF contribution up to June 24 (A) | 56,47,900 | 1,20,000 | 2,228 | 0 |

Funds withdrawn in June, 24 | 2,77,772 | -1,20,000 | -2,228 | 0 |

Balance after withdrawals (B) | 53,70,128 | 0 | 0 | 0 |

Interest accrued Apr 24-Jun 24 (8.25% of A) | 1,16,488 | 1,650 | 46 | 0 |

EPF contribution Jul 24-Mar 25 (C) | 0 | 2,50,000 | 0 | 1,10,000 |

Interest accrued Jul 24-Mar 25 (8.25% of B) | 3,32,277 | 10,932 | 0 | 1,788 |

Total Interest accrued during the year (D) | 4,48,765 | 12,582 | 46 | 1,788 |

Calculation of TDS deducted:

Particulars | Non-taxable account | Taxable account |

Total funds in the accounts to carry forward next year (A+B+C+D) | 60,81,475 | 1,11,834 |

TDS @10% ((1,788 + 46)x 10%) | 0 | 184 |

Balance carried forward to next year | 60,81,475 | 1,11,834-184 |

Flow chart

Tax on EPF withdrawals

If EPF is withdrawn after five years of continuous service, then no tax is required to be paid on the contribution amount and interest received on the same. However, If you withdraw money in case of emergencies (we’ll talk about it) before a specified period of 5 years, then in that case, you won’t be exempted from tax. And the PF department will deduct TDS on EPF withdrawn before five years of continuous service at 10%.

Illustration

Mr. Ram’s total PF contribution (including interest) is Rs.5,50,000 as on 31st March 2023. Ram works in a company registered under EPFO and contributed Rs.3,50,000 to his EPF account in FY 2023-24. He received an interest of 8.25% on his contribution.

Now calculate his taxable and non-taxable contributions for FY 2023-24

Particulars | Taxable contribution | Non-Taxable contribution |

Closing balance, including interest, as on 31st March |

| 5,50,000 |

The contribution made in FY 2023-24 | 1,00,000 | 2,50,000 |

Interest accrued for FY 2023-24 | 8,250 | 20,625 |

Total | 1,08,250 | 8,20,625 |

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption