|

GST on Freight Charges: HSN/SAC Code and GST Rate

Shipping goods comes with freight charges, but how does GST affect them? This article explains how GST applies to freight, whether you can claim ITC, the HSN and SAC codes for freight, and what to expect with the Reverse Charge Mechanism (RCM) on freight charges, etc.

What are Freight Charges?

Freight charges refer to the expenses businesses incur to transport goods from one place to another. These charges vary based on several factors. The following is a breakdown of the common components of freight charges:

| Component | Description |

| Mode of Transport | The means used to move goods—road, rail, air, or sea. Each mode has distinct costs. |

| Loading and Unloading | Fees for handling the goods at both the origin and destination points. |

| Forwarding Costs | Covers safe delivery, packaging, and necessary documentation. |

How GST Applies to Freight Charges

| Scenario | GST Applicability | Explanation |

| Freight charges included in the sale invoice | GST applies at the rate applicable to the goods sold | If freight is part of the total value of goods, it gets taxed at the same rate as the goods. |

| Freight charges are billed separately | GST applies as per the freight service rate. | When billed separately, the applicable rate depends on the type of transport used. |

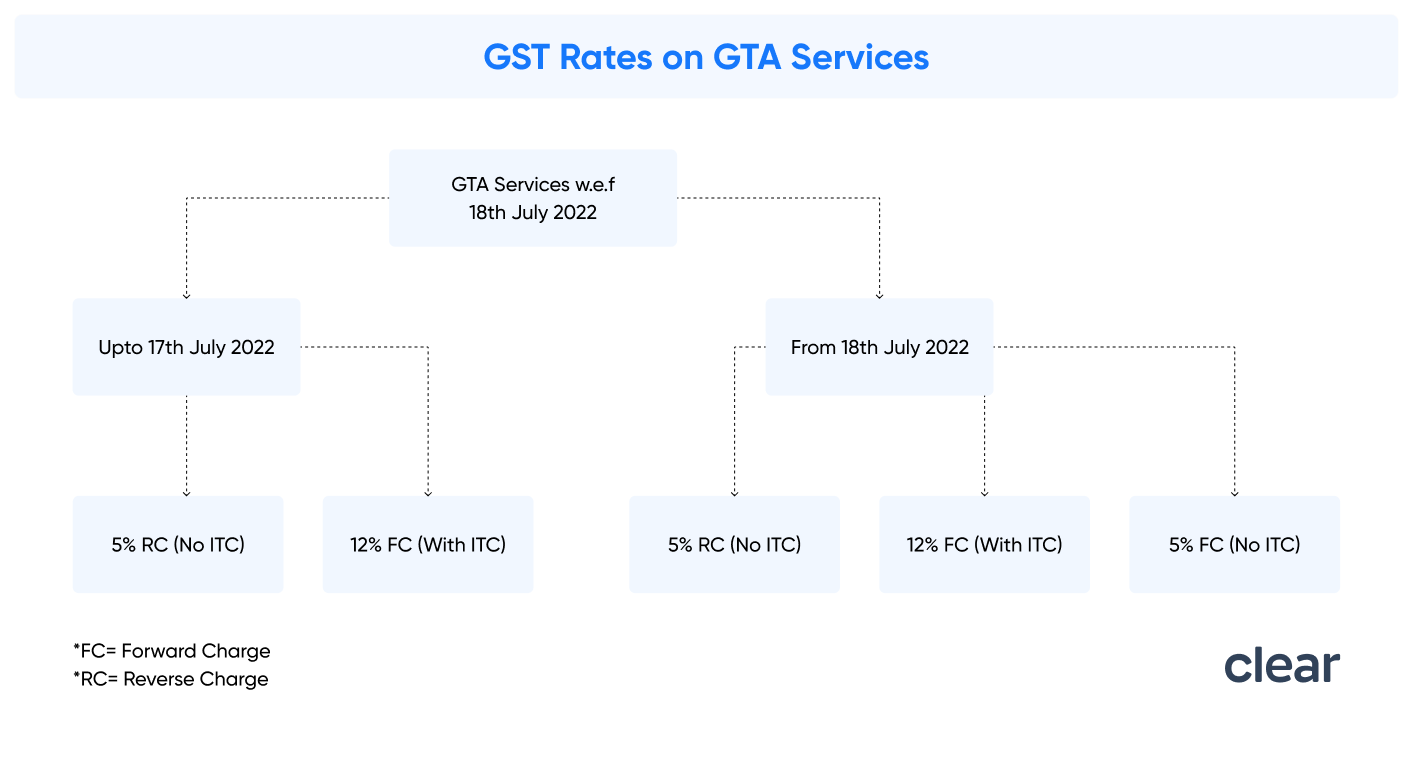

| Freight charges paid to Goods Transport Agencies (GTA) | GST applicable at 5% (without ITC) or 12% (with ITC) if the GTA opts to pay under forward charge, or 5% (without ITC) under the reverse charge mechanism | In most cases, the recipient (buyer) pays GST under RCM for GTA services. Check the list of recipients covered under the Reverse Charge Mechanism. |

| Freight charges for the export of goods | Exempt from GST | Freight services for exports are generally GST-exempt. |

Reverse Charge Mechanism (RCM) on Freight Charges

The Reverse Charge Mechanism (RCM) under GST shifts the tax liability from the supplier to the recipient, ensuring streamlined tax compliance for specific services in the transport and logistics sector.

The CBIC notification no. 03/2022-Central Tax (Rate) dated 13th July 2022 clarified the GST rates applicable to Goods Transport Agencies (GTAs) on both a forward and reverse charge basis as follows:

| Service Category | GST Rate (%) | Special Conditions/Notes |

| Goods Transport Agency (GTA) services - when the GTA does not opt to pay GST on a forward charge basis | 5% | Input tax credit is not allowed on goods and services used in supplying the service |

| Goods Transport Agency (GTA) services - when the GTA opts to pay GST on a forward charge basis | 5% or 12% | If the 5% rate is selected, input tax credit is not allowed on goods and services used in supplying the service. (Note that the option to pay GST on a forward charge basis must be exercised by the GTA by filing a declaration.) |

One must note the following:

- Other than GTAs or courier agencies, road transportation is exempt from GST.

- GTAs exclusively providing RCM-liable services are not required to obtain GST registration.

- Ancillary services (e.g., loading, unloading, warehousing) are part of the composite GTA service if billed together and taxed under RCM. Separately billed ancillary services are treated as independent taxable supplies.

The recipient can claim Input Tax Credit (ITC) where 12% GST has been paid, in all applicable cases unless restricted (e.g., ITC on freight for tax-exempt goods).

GST Rate and HSN Code on Freight Services

For GST purposes, freight includes various transportation modes. Each has specific GST implications, which businesses should understand for effective tax compliance.

| Type of Transportation Service | HSN Code | Applicable GST Rate | Notes

|

| Goods Transport Agency Services | 9965 | 5% / 12% | 5% (without ITC) or 12% (with ITC) under forward charge, and 5% (without ITC) under reverse charge |

| Transport of goods by rail (other than exempted goods) | 9965 | 5% | Input tax credit is not allowed on goods used in supplying the service |

| Transport of natural gas, petroleum crude, motor spirit, high speed diesel or aviation turbine fuel through pipeline | 9965 | 5% | Input tax credit is not allowed on goods used in supplying the service |

| Transport of goods by ropeways | 9965 | 5% | Input tax credit is not allowed on goods used in supplying the service |

| Goods transport services (other than specified categories) | 9965 | 18% | No special conditions |

| Transport of goods by road except the services of a GTA, a courier agency, or by inland waterways | 9965 | Nil | No special conditions |

| Transport of goods in a vessel by a person located in a non-taxable territory to a person located in a non-taxable territory from outside India to a customs station in India | 9965 | 5% | Input tax credit is not allowed on goods used in supplying the service |

| Transport of goods by an aircraft from a place outside India to a customs station in India | 9965 | Nil | No special conditions |

| Renting of goods carriage (with fuel cost included) | 9966 | 12% | No special conditions |

| Time charter of vessels for the transport of goods | 9966 | 5% | Input tax credit is not allowed on goods (other than ships, vessels and tankers) has not been taken |

| Supporting services in transport (does not include services by a GTA) | 9967 | 18% | Excludes GTA services |

| Postal and courier services | 9968 | 18% | No special conditions |

List of Freight Services Exempt from GST

| HSN Code | Exempt Transport Services | GST Rate |

| 9965 | Services by way of transportation by rail or a vessel within India (a) Relief materials for victims of natural or man-made disasters, calamities, accidents or mishaps (b) Defence or military equipments (c) Newspaper or magazines registered with the Registrar of Newspapers (e) Agricultural produce (f) Milk, salt and food grains including flours, pulses and rice, and (g) Organic manure | Nil |

| 9965/9967 | Services provided by a goods transport agency, by way of transport in a goods carriage of- (a) Agricultural produce (b) Milk, salt and food grains, including flour, pulses and rice (c) Organic manure (d) Newspaper or magazines registered with the Registrar of Newspapers (e) Relief materials meant for victims of natural or man-made disasters, calamities, accidents or mishaps, and (f) defence or military equipments | Nil |

Input Tax Credit (ITC) on Freight Charges

The good news is: Yes, you can—but only if the freight charges are related to your business activities.

| Condition | Requirement |

| GST Registration | Your business must be GST-registered |

| Freight for Business Use | Must be used for business purposes |

| Proper Documentation | Keep invoices to claim ITC |

By claiming ITC, you can offset the GST paid on freight against your overall tax liability.

Further, ITC on freight is not allowed where GST has been paid at the rate of 5%. Please refer to the GST rates table above to know the specific instances where ITC is not allowed on the GST paid on freight charges.

Read more:

GST on Shipping Charges

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption