Call Now

Call Now

Section 80DDB of Income Tax Act: Deduction Limit, Diseases Covered, Claim Deduction & Certificate

Section 80DDB is beneficial in taxation because it directly reduces your taxable income by allowing you to claim medical expenses for certain critical illnesses. Since these treatments are often costly, the deduction helps ease the financial burden and ensures you pay tax only on your reduced income after claiming expenses.

Key Highlights

- Deductions available for meical expenses for the taxpayer and their dependents.

- Deductions are allowed after adjusting reimbursements from insurance or an employer. Only out-of-pocket expenses are eligible.

- A deduction can be claimed only for an eligible disease as specified by the CBDT.

What is section 80DDB?

Section 80DDB provides tax relief to individuals and HUFs by allowing a deduction for medical expenses incurred on specified diseases that are considered serious. The deduction can be up to Rs. 40,000, and in the case of senior citizens, it can be up to Rs. 1,00,000.

Deduction under section 80DDB is allowed for medical treatment of a dependent who is suffering from a specified disease (listed in the table below).

Eligibility for Section 80DDB Deduction

- Can be claimed by an Individual or HUF.

- Cannot be claimed by corporates or any other entity.

- Allowed only to Resident Indians.

- When taxpayer has spent money on treatment of the dependent.

- Dependent shall mean spouse, children, parents and siblings.

- In case the dependent is insured and some payment is also received from an insurer or reimbursed from an employer, such insurance or reimbursement received shall be subtracted from the deduction.

Deduction limit U/s 80DDB

Under Section 80DDB, any amount actually paid for the medical treatment of specified diseases is eligible for deduction as prescribed by the CBDT. The deduction limits are given in the table below:

Dependent / Member | Age Limit | Maximum Deduction Limit |

Individual and dependent family members or members of HUF | Less than 60 years during the relevant financial year. | Rs.40,000 |

Individual and dependent family members or members of HUF | 60 Years or more during the relevant financial year. | Rs.1,00,000 |

- Under section 80DDB, the deduction is available only after adjusting any reimbursements.

- This means that if reimbursement of medical expenses already received in the form of insurance or reimbursement from employer, the amount so received of not considered for deduction.

- Essentially, only the net out-of-pocket medical expenses borne by the taxpayer are eligible for deduction under this section.

This ensures that the taxpayer does not claim a deduction for expenses that another source of funding has already covered.

Illustration

- If an individual incurred an expenditure of Rs. 80,000 in FY 2024-25 for a specified disease for which he received a sum of Rs. 30,000 from an insurance company, he can claim only Rs.10,000 under the section (Rs.40,000 less the amount received by way of insurance, Rs.30,000).

- Further, in the case of a senior citizen, an individual can claim Rs.70,000 (Rs.1,00,000 - Rs.30,000) under the same circumstance stated above since the prescribed limit for senior citizens under the section is Rs.1,00,000.

- Let us look at another example, if a taxpayer has incurred an expenditure of Rs.80,000 in FY 2024-25 in medical treatment & he has received Rs.60,000 from an insurer, then he will not be eligible to claim the deduction since the insurance amount exceeds the threshold limit of Rs.40,000.

Similarly, if he is a senior citizen, he will be eligible for a deduction of Rs. 20,000 (Rs.80,000- Rs.60,000) only in such a case.

List of Diseases and the Specialists who can give Certificate under Section 80DDB

| Serial No | Disease | Certificate to be taken from |

| (i) | Neurological Diseases where the disability level has been certified to be of 40% and above — (a) Dementia (b) Dystonia Musculorum Deformans (c) Motor Neuron Disease (d) Ataxia (e) Chorea (f) Hemiballismus (g) Aphasia (h)Parkinsons Disease | Neurologist having a Doctorate of Medicine (D.M.) degree in Neurology or any equivalent degree, which is recognised by the Medical Council of India |

| (ii) | Malignant Cancers | Oncologist having a Doctorate of Medicine (D.M.) degree in Oncology or any equivalent degree which is recognised by the Medical Council of India |

| (iii) | Full Blown Acquired Immuno-Deficiency Syndrome (AIDS) | any specialist having a post-graduate degree in General or Internal Medicine, or any equivalent degree which is recognised by the Medical Council of India |

| (iv) | Chronic Renal failure | a Nephrologist having a Doctorate of Medicine(D.M.) degree in Nephrology or a Urologist having a Master of Chirurgiae(M.Ch.) degree in Urology or any equivalent degree, which is recognised by the Medical Council of India |

| (v) | Hematological disorders (i) Hemophilia (i) Hemophilia (ii) Thalassaemia | a specialist having a Doctorate of Medicine (D.M.) degree in Hematology or any equivalent degree, which is recognised by the Medical Council of India |

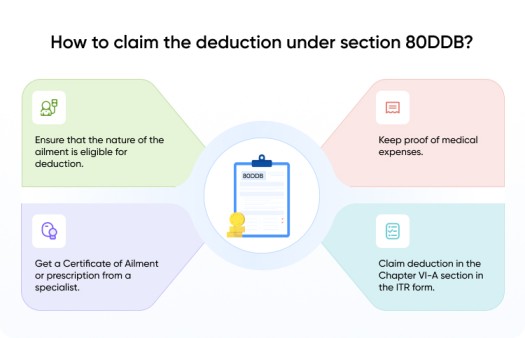

How to Obtain the Certificate for the Disease for Section 80DDB Deduction?

- The certificate can be taken from a Specialist as per the table below.

- Patients getting treated in a private hospital are not required to take the certificate from a government hospital.

- Patients receiving treatment in a government hospital have to take the certificate from any specialist working full-time in that hospital. Such specialist must have a postgraduate degree in General Medicine or an equivalent degree, which is recognized by the Medical Council of India (MCI).

- A certificate in Form 10-I is no longer required.

What Should be Mentioned in the Certificate?

The certificate should include the following details to ensure completeness -

- Patient's name and age

- Name of the disease or ailment

- Name, address, and registration number of the specialist issuing the certificate

- Qualifications of the specialist

- If the patient is receiving treatment in a Government hospital, the certificate should also include the hospital's name and address.

Conclusion

To summarise, an individual or an HUF can avail deduction on the medical expenses incurred by them on the prescribed diseases up to Rs.40,000 or Rs.1,00,000 as the case may be.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption