|

Lower GST Rate Composition Scheme for Service Providers

|

The Government introduced the composition scheme to assist small taxpayers and reduce the compliance burden. A dealer under composition scheme is required to maintain fewer records/books of accounts and not required to file monthly returns. Earlier, the scheme was available to only the suppliers of goods. However, in the 32nd GST Council Meeting, it has been announced that the scheme will now be available to service providers too. The scheme for service providers is available from 1 April 2019 . The article details out the conditions to opt into the scheme by service providers.

Latest Updates:

6th February 2023

Composition taxable persons and those interested to opt into the scheme for FY 2023-24 can do so by submitting a declaration on the GST portal in Form CMP-02 by 31st March 2023.5th July 2022

(a) The due date of GSTR-4 for FY 2021-22 is further extended by a late fee waiver up to 28th July 2022 vide Notification 12/2022 dated 5th July 2022.

(b) The due date of CMP-08 for April-June 2022 is extended up to 31st July 2022 vide Notification 12/2022 dated 5th July 2022.26th May 2022

As per the CGST Notification no.7/2022 dated 26th May 2022, the late fee has been waived for the delay in filing GSTR-4 for FY 2021-22, if it is filed between 1st May and 30th June 2022.24th February 2022

Composition taxable persons and those interested to opt into the scheme for FY 2022-23 must submit a declaration on the GST portal in Form CMP-02 by 31st March 2022.28th May 2021

As per the outcome of the 43rd GST Council meeting and CBIC notification,

(1) Interest relief has been provided for filing of CMP-08 for Jan-March 2021 quarter as per which, for any delay, interest is not charged until 3rd May, whereas 9% of reduced interest will be charged if filing is done thereafter until 17th June, and 18% later on.

(2) The due date to file GSTR-4 for FY 2020-21 is extended up to 31st July 2021.

(3) The maximum late fee for GSTR-4 that can be charged will be restricted to Rs.500 per return for nil filing and Rs. 2000 for other than nil filing.1st May 2021

(1) The due date to file GSTR-4 for FY 2020-21 was extended from 30th April 2021 to 31st May 2021.

(2) Form CMP-08 that was due by 18th April 2021 for January-March 2021 has been given a relaxation in the interest charges. No interest for filing on or before 8th May, interest reduced to 9% between 9th May and 23rd May, but charged at 18% thereafter.

(3) The time limit to file ITC-03 by newly opted composition taxable persons for FY 2021-22 is extended up to 31st May 2021.

What is the Composition Scheme for Service Providers?

The composition scheme for service providers gives an option to taxpayers rendering services having aggregate annual turnover up to Rs. 50 lakh to pay tax at a nominal rate, subject to conditions. The following persons can opt into this scheme:

- Supplier of services only (i.e., service providers)

- Suppliers of goods and services (i.e., those suppliers who were not eligible for composition scheme earlier)

Note: Suppliers of goods and restaurant service providers were earlier eligible under the composition scheme.

Registration into Composition levy by Service providers

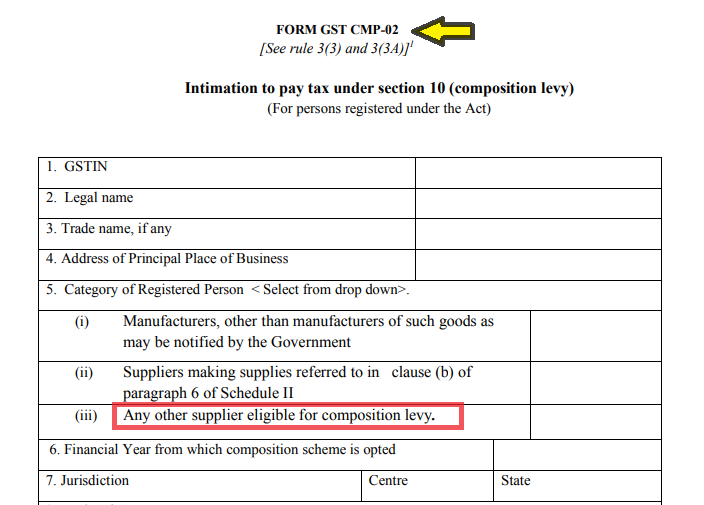

The composition scheme rules apply to the scheme notified under notification number 2/2019 dated 7th March 2019. Hence, the method for opting into the scheme for service providers remains similar to that of an existing composition taxpayer. However, such taxpayers must particularly tick mark Sl. no.5(iii) i.e., ‘any other supplier eligible for composition levy’.

The rest of the fields needs to be filled like any other composition scheme dealer.

Merits and Demerits of composition scheme:

| Merits | Demerits |

| Fewer compliances | Cannot claim the input tax credit |

| Reduced tax liability | Cannot charge or collect tax from the customer. So, a taxpayer bears the liability himself under the scheme. |

| Fewer details in books of accounts | Cannot carry out interstate transactions or Exports |

Conditions to be fulfilled to be eligible under the scheme

- The supplier of service must have a turnover of less than Rs. 50 lakh in the previous financial year.

- The supplier should not be supplying non-taxable goods.

- The supplier should not be engaged in making inter-state supplies.

- The supplier should not supply through an e-commerce operator.

- The supplier should not be a casual taxable person or non-resident taxable person.

- The supplier must issue a bill of supply instead of a tax invoice. The supplier must mention the words ‘composition taxable person’ on the bill of supply.

- The supplier cannot charge and collect tax from the customer.

- The supplier cannot claim the input tax credit.

- The supplier must pay normal tax for reverse charge supplies.

- The supplier cannot be supplying ice cream and other edible ice, whether or not containing cocoa, pan masala and tobacco and manufactured tobacco substitutes.

Rate for composition service providers

For composition service providers, the applicable GST rate is 6% (being 3% CGST + 3% SGST) For calculation of the aggregate annual turnover, the value of supply of exempt services by way of extending deposits, loans or advances where the income is represented by way of interest or discount, shall not be taken into account. Compliance by service providers under the composition scheme: The taxpayers would be required to file only one Annual return with quarterly payment of taxes (along with a simple declaration).

Comparison between normal and composition scheme

Illustration:

| Sl.No | Description | Normal taxpayer (Rate – 18%) | Composition taxpayer (Rate – 6%) |

| 1 | Sales value | 118000 | 118000 |

| 2 | Sales value exclusive of taxes | 100000 | 118000* |

| 3 | Output GST | 18000 | 7080 |

| 4 | Purchases | 40000 | 40000 |

| 5 | Input GST @ 18% | 7200 | 7200 |

| 6 | Total purchase value (6 = 4 + 5) | 47200 | 47200 |

| 7 | Net GST liability (7 = 3 – 5) | 10800 | 7080 |

| 8 | Gross Profit (8 = 1 – {6+7}) | 60,000 | 63,720 |

*Note: In a composition scheme, the dealer is unable to collect tax from the customer.

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption