|

Karnataka VAT Audit in Form VAT 240

As per the Karnataka Value Added Tax Act (K VAT), 2003, every dealer with a turnover exceeding the prescribed limit during a financial year is required to get his accounts audited by a Chartered Accountant, or a Cost Accountant or a Tax Practitioner (tax practitioner cannot certify the accounts of a Company)With the introduction of GST effective from July 1, 2017, the Financial Year has been divided into two period

- April 2017 to June 2017 – Covered under the Karnataka VAT Regime

- July 2017 to March 2018 – Covered under the GST Regime

In this article, we will try to understand the audit requirements for VAT, the format of the Audit Report and the procedure for filing the Audit Report.

Applicability of Karnataka VAT (KVAT) audit for the FY 2017-18

As per the KVAT Act 2003, a dealer is liable for a VAT audit when his turnover exceeds Rupees 1 Crore in a financial year. Additionally, the Commercial Tax Department of Karnataka (CTDK) vide Notification No. FD 53 CSL, 2018 dated 29/09/2018 have extended VAT audit requirement to those dealers who have a turnover between Rs.25 Lakhs to Rs 1 Crore during the first three months of FY 2017-18.

Form and Due Date of KVAT audit for the FY 2017-18

Vat Audit is required to be filed in the form VAT 240 and the due date for filing the same is as follows:

| Turnover (April to June 17) | Due Date |

| 25,00,000 to 1,00,00,000 | 31st March 2019 |

| 1,00,00,000 and above | 31st December 2018 |

Specific points to be noted for 2017-18 KVAT audit

a. Audited Financial Statements have to be bifurcated into two periods – Pre GST period for the conduct of VAT audit and Post GST Period for the conduct of GST Audit;

b. Records to be maintained to ensure that the entire years turnover has been rightly declared under the VAT or under the GST returns and tax appropriately discharged;

c. Special focus should be on transition issues and cut off procedures like:

- Closing Balance of VAT credit should have been carried forward to GST by filing TRAN 1 credit;

- In case the dealer has not received statutory forms (Form C, Form H, etc.) against sales made at the concessional rate then the credit to be carried forward to GST should be restricted to the extent of tax payable on such pending Forms;

- Sales Returns of goods sold under VAT Regime from a registered person- Returns will be treated as supplies in the hands of the purchaser and he is required to charge GST on the same;

- Sales Returns of goods sold under VAT Regime from an unregistered person – Seller required to claim a refund of the VAT

d. Liability identified under the VAT audit needs to be discharged before filing the Form VAT 240.

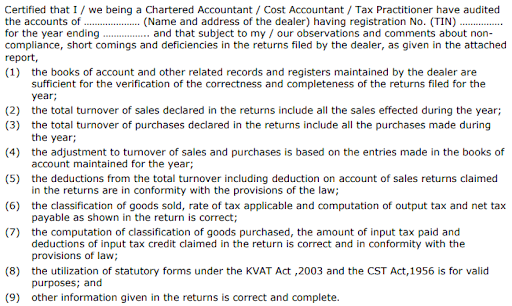

Format for Form 240

a. General information of the dealer in Part-1 of VAT 240

b. Particulars of turnovers, deductions and payment of tax in part-2 of VAT 240.

c. Particulars of Declarations and Certificates in Part-3 of VAT 240

d. Certificate from Chartered Accountant / Cost Accountant / Tax Practitioner who has audited the books of accounts

e. Summary of the additional tax liability or additional refund due to the dealer on the audit for the year

Procedure for filing Form VAT 240

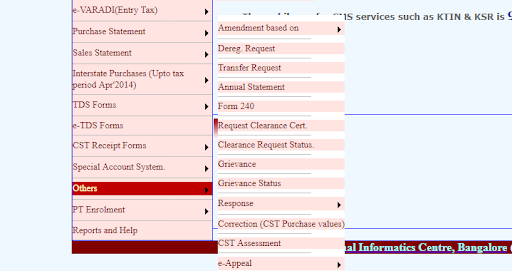

Step 1: Login to Karnataka website – Department of Commercial Taxes.

Step 2: Click on “Others” then on “Form 240”

Step 3: Enter the summary of the report as specified in Form 240

Step 4: Upload the scanned copies of Part 1, 2 and 3 of Form VAT 240

Step 5: Pay additional tax for the year, if payable

Step 6: Submit Form VAT 240

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption