National Pension Scheme (NPS) 2025 - Details, Tax Benefits, Login, Online Registration & Returns

National Pension Scheme (NPS) India is a long-term investment plan for retirement under the purview of the Pension Fund Regulatory and Development Authority (PFRDA) and the Central Government. Investments can be made in NPS Tier-I account (deduction up to Rs. 2 lakhs available under section 80CCD) or both NPS Tier-I and Tier-II account.

Latest Update

- Account can be held by individuals up to 85 years of age.

- On retirement, 100% withdrawal can be made if the corpus balance is up to Rs 8 lakhs.

- Up to 80% of corpus can be withdrawn for non-government employees (60% for government employee).

NPS Withdrawal Amendment

The NPS withdrawal rules has been amended recently through an official notification by Pension Fund Regulatory Authority of India. NPS account can now be maintained by a person of age up to 85 years. Key changes in withdrawal limits are as follows:

For Government Employees

Exit Scenario | Balance at Exit | Lump Sum Allowed | Annuity Requirement |

| Retirement / Discharge | Up to Rs. 8 lakh | 100% | Not mandatory |

| Rs. 8 lakh to Rs. 12 lakh | Up to Rs. 6 lakh or up to 60% | Balance / at least 40% | |

| More than Rs. 12 lakh | Up to 60% | At least 40% | |

| Resignation / Removal | Up to Rs. 5 lakh | 100% | Not mandatory |

| More than Rs. 5 lakh | Up to 20% | At least 80% | |

| Death | Up to Rs. 8 lakh | 100% | Not mandatory |

| More than Rs. 8 lakh | Up to 20% | At least 80% |

For Non-Government Employees

Exit Scenario | Balance at Exit | Lump Sum Allowed | Annuity Requirement |

| Superannuation / 60 years / Incapacitation | Up to Rs. 8 lakh | 100% | Not mandatory |

| Rs. 8 lakh to Rs. 12 lakh | Up to Rs. 6 lakh or up to 80% | Balance / at least 20% | |

| More than Rs. 12 lakh | Up to 80% | At least 20% | |

| Voluntary Exit | Within Rs. 5 lakh | 100% | Not mandatory |

| More than Rs. 5 lakh | Up to 20% | At least 80% | |

| Death | Any amount | Up to 100% | Up to 100% |

| Joined at ≥ 60 years | Within Rs. 12 lakh | 100% | Not mandatory |

| More than Rs. 12 lakh | Up to 80% | At least 20% | |

| Death (Joined at ≥ 60 years) | Any amount | Up to 100% | Up to 100% |

National Pension Scheme - Details

| Aspects | Details |

| Objective | To promote savings and investments, and help the citizens to plan their retirement. |

| Eligibility | Only Indian citizens aged between 18 to 85 years. |

| Types of Accounts | Tier-I Account: Mandatory for government employers, optional for others Tier-II Account: Optional for everyone. |

| Minimum Contribution | For Tier I: Rs. 1000 per annum, Rs.500 for account opening For Tier II: Rs. 250 for account opening. |

| Investment Options | Active choice: The investor can choose equity allocation, whether it is equity oriented, debt oriented or bonds. Passive choice: Equity allocation is chosen based on age of the account owner. |

| Withdrawal | On retirement, at least 20% of the funds should be chosen as annuity. (40% for government employees) |

| Returns or interest | The returns in this scheme depends on market performance, there is no fixed returns in the form of interest. |

What is National Pension Scheme?

- National Pension Scheme is open to employees of the public, private and even the unorganized sectors, except those from the armed forces.

- It encourages people to invest in a pension account at regular intervals during their employment.

- After retirement, the subscribers can take out a certain percentage of the corpus.

- The remaining amount is paid as a monthly pension post your retirement.

NPS Vatsalya

- In NPS Vatsalya scheme, parents can open an NPS account for their minor children and contribute an amount every month or year until they reach 18 years old.

- Once the children are 18 years old, they can manage the account independently by converting the NPS Vatsalya account into a normal NPS account.

- As per recent announcements made in budget 2025, all the tax benefits offered to NPS scheme is also extended to NPS vatsalya accounts.

National Pension Scheme Eligibility

The NPS is a good scheme for anyone who wants to plan for their retirement early on and has a low-risk appetite. Any person fulfilling the following eligibility criteria can join NPS:

- Should be an Indian citizen (resident or non-resident) or a Non-Resident Indian (NRI).

- Should be aged between 18 – 85 years.

- Should comply with the Know Your Customer (KYC) norms detailed in the application form.

- Should be legally competent to execute a contract as per the Indian Contract Act.

- Overseas citizen of India (OCI), Persons of Indian Origin (PIOs) and Hindu Undivided Families (HUFs) are not eligible to subscribe to NPS.

- NPS is an individual pension account, thus it cannot be opened on behalf of a third person.

Features of National Pension Scheme

Age Limit

- NPS account can be opened by a Indian citizen ( including a Non-Residential Indian) is 18 to 70 years.

Returns

- This scheme has been in effect for over a decade, and so far has delivered 11% to 20% annualized returns.

- Though this scheme does not guarantee a fixed rate of interest, it has earned a better returns than other tax saving investments.

Equity Allocation

- Currently, there is a cap in the range of 50% to 75% on equity exposure for the National Pension Scheme.

- For government employees and senior citizens, this cap is 50%

- There are two options to invest in – auto choice or active choice.

- Auto choice sets your investment risk based on age—older investors get more stable, lower-risk options.

- The active choice allows you to decide on the scheme and to split your investments.

Flexibility

- NPS subscribers can contribute to the NPS fund at any time in a financial year and change the number of subscriptions.

- They can choose their own investment options.

- You are also allowed the option to change your fund manager if you are not happy with the performance of the fund.

- They can operate their account online from anywhere and continue it even when they change their city and employment.

- The scheme is portable across jobs and locations.

Withdrawals

Upon Superannuation

- A person can withdraw up to 80% of the total corpus as a lump amount after retirement, with the remaining 20% going into an annuity plan.

- Goverment employees can withdraw up to 60% of the total corpus and opt for annuity for the remaining 40%.

- Subscriber has the option to withdraw the desired amount systematically at regular periodic intervals. i.e, monthly, quarterly, half-yearly or yearly.

- Subscribers can withdraw the entire corpus if it is up to Rs 8 lakh without opting an annuity plan.

- Though withdrawals are tax-free, an annuity is taxable in slab rates.

Pre-mature Exit

- In the event of a premature exit (before reaching the age of superannuation/turning 60), at least 80% of the pension corpus must be used to purchase an Annuity.

- If the total corpus is less than or equal to Rs.5 lakh, the subscriber can opt for 100% lump-sum withdrawal.

Upon the Death of the Subscriber

- Following the subscriber's death, the entire accrued pension corpus (100%) would be paid to the subscriber's nominee/legal heir.

It is to be noted that NPS Tier-II account can be withdrawn anytime, it has no lock-in period.

National Pension Scheme - Interest Rate

As NPS is a scheme where its returns depends on market performance of the fund irrespective of equity allocation, there is no fixed interest rate for this scheme, unlike other savings scheme. The returns depend on various factors like:

- Markets and economic situation

- Equity allocation chosen

- Fund manager chosen

- Duration of the investment

NPS Calculator 2026

National Pension Scheme Types

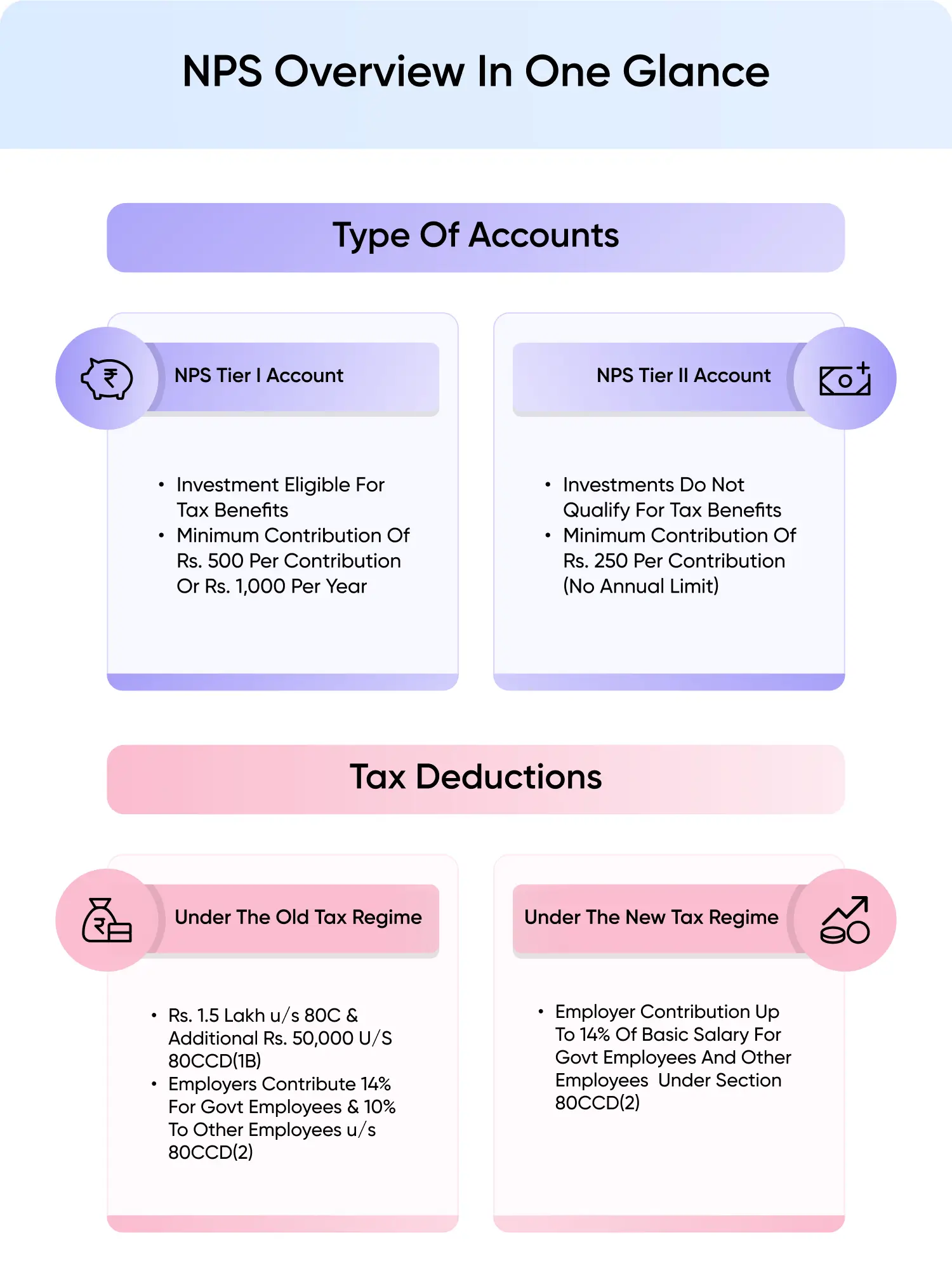

- National Pension Scheme accounts are broadly classified into Tier-I and Tier-II accounts.

- Tier-II account is optional, which can be opened by Tier-I account holders.

NPS Tier I and Tier II Accounts

NPS account can be opened in Tier I or both Tier I and Tier II. The primary differences between Tier-I and Tier-II accounts are given below:

Feature | NPS Tier-I | NPS Tier-II |

Eligibility | All Indian citizens (18–85 years) | Only those with an active Tier-I account |

Type of Account | Retirement-focused (pension account) | Voluntary savings account |

Mandatory or optional | Central/state govt. employees (optional for other employer) | No one – completely optional |

Minimum Contribution | ₹500 per contribution (₹1,000/year minimum) | ₹250 per contribution (no annual minimum) |

Withdrawals | Restricted till age 60 (partial allowed in specific cases) | Fully flexible – can withdraw anytime |

Tax Benefits | Under Sec 80C (up to ₹1.5 lakh) + Sec 80CCD(1B) (₹50k extra) | No tax benefit (except govt. employees under 80C with 3-year lock-in) |

Employer Contribution | Restrictions apply; annuity purchase mandatory | No restrictions |

Purpose | Long-term retirement savings | Flexible investment/savings |

Regulations

- The PFRDA regulates NPS with transparent investment norms, regular performance reviews, and monitoring of fund managers by NPS Trust.

National Pension Scheme Tier-I Tax Benefits - Section 80CCD

Tax Benefits For Self-Contribution

Employees who contribute to NPS can claim the following tax benefits on their contributions:

- Tax deduction of up to 10% of salary (Basic + DA) under Section 80CCD(1), subject to a maximum of Rs.1.5 lakh under Section 80CCE.

- Tax deduction of up to Rs.50,000 under Section 80CCD(1B), along with the overall limit of Rs.1.5 lakh under Section 80CCE.

- The aforesaid deductions cannot be claimed under the new regime.

Tax Benefits On Employer Contributions

- Under section 80CCD(2), deduction can be claimed for employer's contribution towards NPS up to 10% of salary (14% in case of new regime).

- If the employer is central government, 14% of salary can be claimed as deduction irrespective of regime chosen.

Tax Benefits For Self-employed People

Self-employed individuals who contribute to NPS can claim the following tax benefits on their own contributions:

- Tax deduction of up to 20% of gross income under Section 80CCD(1), subject to a total limit of Rs.1.5 lakh under Section 80CCE.

- Tax deduction of up to Rs.50,000 under Section 80CCD(1B), along with the overall limit of Rs.1.5 lakh under Section 80CCE.

- The aforesaid deductions cannot be claimed under the new regime.

Tax Benefits On Withdrawal

Partial Withdrawal

Partial withdrawals from NPS are eligible for tax exemption when the amount withdrawn is up to 25% of self-contribution, subject to the circumstances and criteria prescribed by PFRDA under section 10(12B).

Lump Sum Withdrawal

Section 10 provides a tax exemption on a lump sum withdrawal of 60% of accrued NPS funds upon reaching 60 years or superannuation.

Tax Benefit On Annuity Purchase

Tax exemption is provided on annuity purchase or superannuation at 60 years under Section 80CCD(5). However, the subsequent income from an annuity is taxed under Section 80CCD(3).

National Pension Scheme Tier-II Tax Benefits - Section 80C

- NPS Tier-II account is an optional account that can be opened by Tier-I account holders.

- Contribution made to Tier-II accounts can be claimed as a deduction under section 80C of the Income Tax Act.

- A minimum lock-in period of 3 years is required to claim this deduction.

- Up to Rs. 1.5 lakh of contribution can be claimed as a deduction, subject to the combined threshold limit under section 80C.

- This deduction cannot be availed under the new tax regime.

NPS - Other Benefits

- Investment Flexibility: NPS gives you option to choose from fund managers, and also you can choose your exposure to equity. If you are an aggressive investor, you can choose highly equity oriented funds, and vice versa.

- Transferability: Even if you switch jobs, you can contribute to your NPS account without any significant paperwork.

- Low Fund Manager Charges: NPS provides one of the lowest fund manager charges, leaving more money for investment and accumulation as compared to other funds.

- Retirement Planning: NPS is a well structured pension plan, which assists you to plan your retirement and prepare a steady income flowing mechanism post retirement.

NPS v/s UPS

As already mentioned, the government has launched Unified Pension Scheme (UPS) as an option under NPS. It guarantees a minimum pension amount on completion of a certain number of years of service. The key differences between NPS and UPS are tabulated below:

| Particulars | National Pension Scheme | Unified Pension Scheme |

| Meaning | National Pension System was started to promote savings and investments, and help the citizens to plan their retirement. | Unified Pension Scheme is an option under National Pension Scheme, guaranteeing a minimum monthly payout on retirement |

| Eligibility | Indian citizens aged between 18 to 85 | Only Central Government employees who are already covered under NPS.(retirees of NPS can also opt for UPS) |

| Tax Benefits | Deductions under section 80C, 80CCD(2) are available under the Income Tax Act. | The deductions available to NPS is also extended to UPS. |

| Minimum Pension Amount | No guaranteed minimum pension amount in this scheme. | Rs. 10,000 of guaranteed pension amount available under this scheme. |

| Employee Contribution | 10% of basic salary + Dearness Allowance (DA) | 10% of basic salary + Dearness Allowance (DA) |

| Employer Contribution | 14% of basic salary + Dearness Allowance (DA) | 8.5% of basic salary + Dearness Allowance (DA) |

| Pension calculation | Returns are based on market performance. | 50% of average basic pay over the last 12 months (for employees with 25+ years of service) |

How to Open NPS Account?

It is now possible to open an NPS account in less than half an hour. Opening an account online (enps.nsdl.com) is easy, if you link your account to your PAN, Aadhaar and mobile number.

You can validate the registration using the OTP sent to your mobile. This will generate a PRAN (Permanent Retirement Account Number), which you can use for NPS login.

National Pension Scheme - Login

- You can login to your NPS account either through NSDL protean portal or KFintech Portal.

- For NSDL and Kfintech login, you will require the user ID and password to login. The user ID is Permanent Retirement Account Number (PRAN) for login under both the websites.

NPS Customer Care Number

NPS Call Centre Number: 1800 110 708

NPS SMS Number: NPS to 56677

NPS Toll-Free Number For Registered Subscriber (with PRAN): 1800 222 080

Final Word

Hence, consider investing in the NPS scheme if the benefits elaborated above match your risk profile and investment goal. However, if you are open to more equity exposure, many mutual funds are catering to investors from diverse backgrounds available.

Related Articles:

1. Top Performing NPS Schemes 2025

2. Should I include employer’s contribution to NPS in my taxable salary?

3. How To Unfreeze NPS Account

4. NPS Statement Download

5. NPS vs PPF: Which is a Better

6. OPS vs NPS: Difference

7. Jeevan Pramaan 2025: Digital Life Certificate, Pramaan ID, RD Service and How to Download

Frequently Asked Questions

About the Author

CA Mohammed S Chokhawala

I'm a chartered accountant, well-versed in the ins and outs of income tax, GST, and keeping the books balanced. Numbers are my thing, I can sift through financial statements and tax codes with the best of them. But there's another side to me – a side that thrives on words, not figures. Read more

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption