|

6 Things to Remember While Transitioning to GST Regime

This is a short list of things to remember, as well as basic provisions and laws while transitioning to GST.

Migration to GST

Every taxpayer registered under Excise/VAT/service tax will enroll on the Common Portal. On enrollment, he will get a provisional certificate of registration which will have the GSTIN.

New Registrations under GST

- New business

- Manufacturers with a turnover less than Rs. 1.5 crore (threshold under GST has been reduced to 20 lakhs)

- Any trader with turnover below 20 lakhs and are selling online

- Any trader having regular inter-state sales

- Voluntary registrations are allowed

Taxability of goods/services supplied after GST

This can be understood through the point of taxation rules. If point of taxation of goods/services is before the GST implementation then it will be taxed under earlier law. GST will not be applicable. Any portion of any supply whose point of taxation is after GST implementation will be taxed under GST.

Carry forward ITC after Transitioning to GST

CENVAT Credit and VAT credit in stock will be available to be carried forward in GST. If integrated tax is paid on such goods (such as CST.) then amount of credit will be 30% for goods attracting 18% and above GST. ITC will be 20% for other goods.

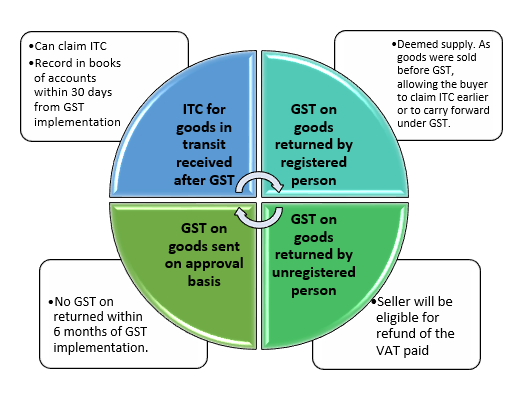

Treatment of Goods Returned

(a) Removal: must be max 6 months before GST

(b) Return: Within 6 months from the GST implementation date

If the goods are not returned within time, the supplier will not be eligible for the tax refund. Same provisions are applicable for excise.

Composition scheme

Composition scheme is available for persons with turnover upto 50 lakhs. This is just a few pointers you must keep in mind when transitioning to GST. Do you have more questions on transition to GST? ClearTax has in-depth articles on transition to GST.

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption