Call Now

Call Now

Section 44B And Section 172 Of Income Tax Act

India has a vast coastline of 7,517 km and 13 major ports. Since our country conducts a major portion of its trade through shipping, tax provisions related to the same need to be clearly defined.

Both Section 44B and Section 172 of the Income-tax Act 1961 deal with tax provisions for the shipping business. These sections simplify the taxes in the shipping business, encouraging investments and economic growth.

Read further to understand the tax provisions for these sections.

What Is Section 44B Of Income Tax Act?

Section 44B is a part of the presumptive taxation scheme under the Income Tax Act. It deals with the taxation of profits on shipping businesses carrying passengers or goods to or from an Indian port in relation to non-residents or foreign companies.

What Is Foreign Shipping Business?

Any ship belonging to or chartered by a non-resident that carries passengers, livestock, mail or goods shipped at a port in India. Any amount received in relation to such carriage shall be treated as income from the shipping business. Such income also includes demurrage charges or handling charges in relation to such carriage.

Taxation Provision of Section 44B

If they choose to pay taxes under this section, their taxable income would be calculated as 7.5% of their aggregate receipts. This provision applies to any person receiving compensation for shipping or payments on the assessee’s behalf. However, the assessee cannot avail deductions available from Section 28 -Section 43A on the profits and gains from business and profession.

If a non-resident doesn’t wish to choose presumptive taxation for their shipping business, they will be liable to pay taxes under the regular tax slabs for profits and gains from business and profession.

The provisions of section 44B are similar to the presumptive taxation under section 44AD or section 44ADA that are available for resident taxpayers, but section 44B covers only non residents taxpayers.

Section 44B: Applicability, Turnover Limit, Example

Any non-resident involved in the shipping business can opt for Section 44B. Let's look at an example to better understand.

Example: A foreign resident, Mr. Patterson, engaged in the shipping business, makes the following transportation:

- Shipping Rs. 70 lakh worth of goods from Chennai port to a port in Germany and Rs. 2 lakh as handling charges.

- Shipping Rs.1 crore worth of automobiles to Sri Lanka and Rs. 0.75 lakh as handling charges.

- Transporting passengers for receipts of Rs. 2 crore in India.

- Carry forward of losses of a manufacturing business in India of Rs. 1,00,000.

Thus, his taxable income shall be calculated as follows:

7.5% of Rs. 2 lakhs = 2,00,000*7.5% = Rs. 15,000

7.5% of Rs 2 crore = Rs. 15,00,000

Less: Carry forward losses of Rs. 1,00,000

Hence the total taxable income for Mr Patterson shall be Rs.14,15,000.

It is important to note that only the freight received in India or transported from India was considered to be income for the purpose of taxation. Hence, we have not considered the freight transported to Sri Lanka for the purpose of taxation.

Benefits Of Section 44B:

- The tax compliance procedure of these companies is facilitated by the presumptive basis applied in computing taxable income.

- The 7.5% rate is lower than the normal tax rates applicable to resident corporations.

- These businesses' taxable income is reduced by the allowable deductions from the gross freight charges, thus lowering their tax liability.

What Is Section 172 Of Income Tax Act?

This section applies to a non-resident partaking in the shipping business where the goods, livestock or passengers are transported from a port in India. The taxable income under this section shall be calculated as 7.5% of the amount paid as shipping fees to the owner or charterer of the vessel.

Furthermore, under this section, the person employed as the ship’s master must furnish tax returns for any sum paid or payable for shipping at a port. Section 172 also states the provisions for non-compliance and conditions for port clearance.

Shipping Business of Non-residents

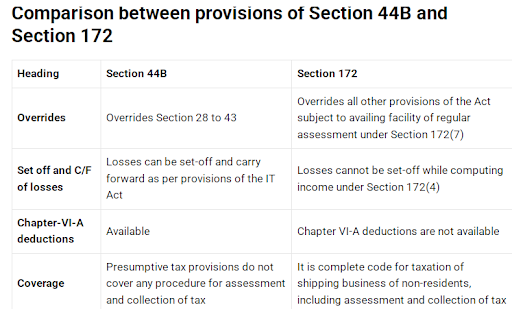

The provisions of the section apply to shipping business conducted by any foreign individual or company to and from India. For the purpose of Section 44B, any transportation made to or from India is considered for taxation. However, in the case of Section 172, only transportation made from India is considered. The ship must either belong to the non-resident or be chartered by them to be considered eligible under these sections.

Income of Non-resident from Shipping Business

The income of a non-resident from a shipping business is considered as follows:

- Any amount received or payable for transportation to or from India. It includes transportation of passengers, mail, goods and livestock.

- Any amount received or payable or deemed to be received or payable in India for transportation made outside India.

- Handling or demurrage charges.

If a non-resident chooses to pay taxes under this section, they need to declare 7.5% of the total revenue as income from the shipping business.

Both Section 44B and Section 172 do not permit any deductions for expenses from Sections 28 - Section 43A. This, however, doesn't include any carry-forward or set-off of losses or deductions under Chapter VI-A if applicable. This means if the assessee has incurred any losses, they can set it off against their taxable income.

Section 172: Applicability, Turnover Limit, Example

The master of the vessel is required to pay this tax and file their return before the vessel departs from India. However, if the shipmaster can’t do so for any reason, the assessee must show that he/she has made arrangements to file tax returns to the assessing officer.

If the officer is satisfied, he/she shall allow port clearance to the ship, provided the ship master has made provisions and assigned another person to pay the tax on his behalf. This tax must be paid within 30 days of the ship’s departure.

Example: A foreign company engaged in shipping business made the following transportations:

- Livestock for Rs. 45 lakh from Chennai port to Singapore.

- Payment of Rs. 1 crore received in India for goods being carried from Malaysia to Singapore.

- Goods worth Rs. 2 crore shipped from Mumbai to Malaysia. Freight charges are to be received in Malaysia.

- Goods worth Rs. 75 crore shipped from Bangalore to Dubai for Rs.3 Crores.

- This company’s total taxable income would be

7.5% of Rs. 45,00,000 = Rs. 3,37,500

7.5% of Rs. 1 crore = Rs. 7,50,000

7.5% of Rs. 2 crore = Rs. 15,00,000

7.5% of Rs. 3 crore = Rs. 22,50,000

The total taxable income would be Rs. 48,37,500. Now, the applicable corporate tax rate in India is 40% for a foreign company. So, the tax payable would be Rs. 19,35,000, excluding the cess and surcharge.

Option to pay tax as per normal provisions of the IT act on Shipping Income

The owner or the charterer, rather than choosing provision of Section 172 as final assessment, can make a choice to contend that an assessment in relation to his aggregate income during the last previous year and the tax due thereon be made in accordance with the other provisions of the IT Act.

But such an option must be exercised prior to the end of the assessment year in relation to the earlier year in which the date of departure of the ship from the Indian port is.

Note:

If a non-resident does not choose to be governed by provision of Section 172, any tax payment section 172 is treated as an advance tax. If such advance tax is less than the tax on assessment, the excess of the amount so paid over the amount of tax ascertained to be payable on such assessment is to be recovered from him (i.e., when Advance tax < tax payable under Section 172). But where tax payable on assessment is less than such advance tax, the amount of difference is to be refunded to him (i.e., where advance tax under Section 172 > Tax payable).

Both sections 44B and 172 are meant to simplify taxation for non-residents engaged in the shipping business. The primary difference between these two sections is that Section 44B overwrites Section 28 - Section 43A, whereas Section 172 overwrites the entire Income Tax Act. Therefore, an assessee can set off their losses and avail a deduction of Chapter VI A under Section 44B, but no such provision is allowed for assessees under Section 172.

Conclusion:

The aim of sections 172 and 44B is to simplify taxes on non-residents engaged in the sea trade. Section 44B replaces Sections 28 to 43A, whereas Section 172 replaces the entire Income Tax Act. This is the main difference between these two sections of the Income Tax Act. Consequently, an assessee can apply Section 44B to offset their losses and avail a Chapter VI A deduction. But assessees under Section 172 cannot avail this provision.

Also Read:

1. Section 44BBC: Tax on Non-Resident Cruise Ship Operators (FY 2025–26)

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption