Income Tax on Pension: Are Pensions Taxable?

Pension is taxable under the head Income From Salaries. Pensions are paid out periodically, generally every month. However, the taxpayer may also choose to receive the pension as a lump sum (also called commuted pension) instead of a monthly payment. In case of a commuted pension, the taxpayer will have the option of claiming an exemption under section 10 of the Income Tax Act, 1961.

Commuted and Uncommuted Pension

Generally, the employer and taxpayer contribute together to an annuity fund, which pays the taxpayer pension out of the fund. At the time of retirement, you may choose to receive a certain percentage of your pension in lump sum rather than receiving it in installments. Such pension received in lump sum is called commuted pension. The remaining part of the pension that the taxpayer chooses to receive in installments on a monthly basis is called uncommuted pension.

For example, Mr. Anban at the age of 60 years, chooses to receive 10% of his monthly pension worth Rs 10,000 of the next 10 years in advance. This will be paid to him as a lump sum.

Therefore, 10% of Rs 10,000 x 12 x 10 = Rs 1,20,000 is his commuted pension.

He will receive Rs 9,000 per month as uncommuted pension for the next 10 years until he is 70 and after 70 years of age, he will be paid the full pension of Rs 10,000 on a monthly basis.

Taxability of Commuted and Uncommuted Pension

- Uncommuted pension or any periodical payment of pension is fully taxable as salary. In the above case, Rs 9,000 received by Mr. Anban is fully taxable. Rs 10,000, starting at the age of 70 years, is fully taxable as well.

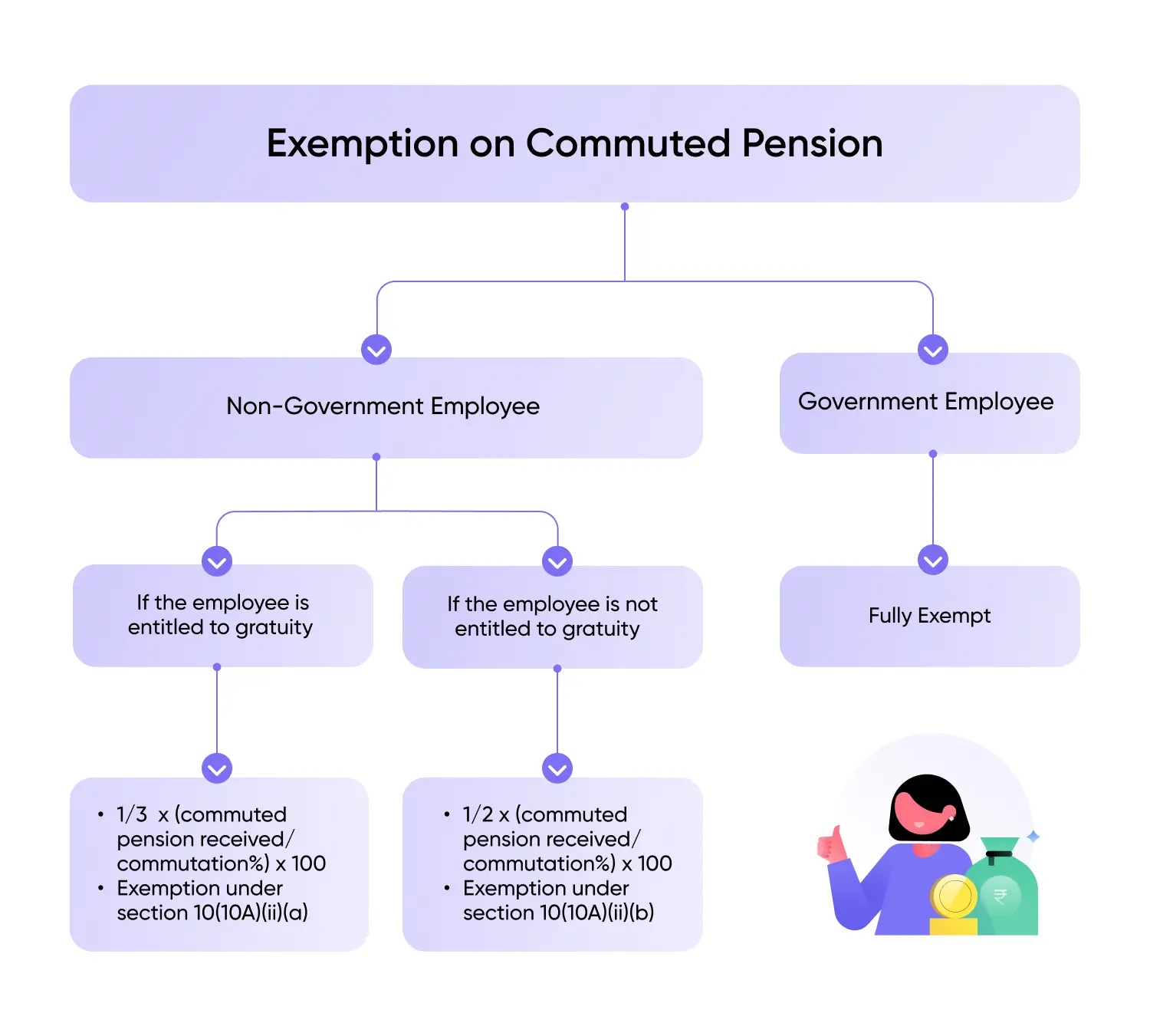

- Commuted or lump sum pension received by government employees is exempt from taxes.

- Commuted or lump sum pension received by non-government employee is partially exempt depending on whether gratuity is also received by the person:

- If a person receives both gratuity and pension – If 100% of the pension was commuted, then 1/3rd of the amount of pension is exempt and the remaining is taxed as salary.

- If a person does not receive gratuity but receives only pension – If 100% of the pension was commuted, ½ of pension amount is exempt.

Note: Exemption in respect of commuted pension is available under both the tax regimes.

Exemption On Commuted Pension

The exemption on commuted pension can be calculated as follows in two different scenarios.

Covered Under Payment Of Gratuity Act

If the taxpayer is covered under the payment of gratuity act and receives gratuity then the amount of exemption will be calculated based on the below formula u/s 10(10A)(ii)(a):

⅓ x (Commuted amount received/commutation %) x 100 |

Not Covered Under Payment Of Gratuity Act

If the taxpayer is not covered under the payment of gratuity act and does not receive any gratuity then the amount of exemption will be calculated based on the below formula u/s 10(10A)(ii)(b):

½ x (Commuted amount received/commutation %) x 100 |

Section 194P

Section 194P is applicable from 1st April, 2021. This section exempts senior citizens of age 75 years and above from filing Income tax returns if the following conditions are met:

- Senior citizens should be 75 years or above.

- He had to be a resident in the previous year.

- He has pension and interest income only, and interest accrued/ earned from the same specified bank in which he receives his pension.

- He will submit the declaration to a specified bank.

- The bank is a ‘specified bank’ as notified by the central government. These banks will deduct TDS of senior citizens after taking into account the deduction under Chapter VI-A, and the rebate under 87A.

- Senior citizens are not required to file income tax returns once the specified banks deduct TDS.

How to Report Pension Income in ITR?

- In ITR-1, go to the ‘General Information' > ‘Nature of Employment’ section > Select ‘Pensioners’. Here, there are four types of Pensioners: CG- Pensioners, SG- Pensioners, PSU- Pensioners and Other Pensioners.

- In other ITRs, go to salary schedule and select Nature of Employer as “Pensioners”. Pension income taxable as ‘salary’ has to be reported by mentioning the name, address, tax collection account number (TAN) of the employer and the tax deducted (TDS) thereon.

- The exempt portion of the pension must be reported as ‘Commuted Pension’ in the field ‘Section 10(10A)- Commuted value of pension received' under the ‘Nature of Exempt Allowance’. Mention the amount of commuted pension.

Any excess amount must be reported as ‘Annuity Pension’ under ‘Salary under Section 17(1)’ of the Income Tax Act, 1961.

Pension Received by a Family Member

Pension received by a family member is taxed under the head ‘income from other sources’ in family member’s income tax return.

- If this pension is commuted or is a lump sum payment, it is not taxable in certain cases.

- Uncommuted pension received by a family member is exempt to a certain extent. Rs. 25,000 or 1/3rd of the uncommuted pension received – whichever is less is exempt from tax. (This amount of Rs. 25,000 has been increased from Rs.15,000 with effect from FY 2024-25)

For example – If a family member receives a pension of Rs 1,00,000, the exemption available is least of – Rs 25,000 or Rs 33,333 (1/3rd of Rs 1,00,000).

Thus, the taxable family pension will be Rs.75,000 (Rs 1,00,000 – Rs 25,000)

Pension: exempted from tax

Pensions received from UNO by its employees or their family is exempt from tax. Pension received by family members of the armed forces is also exempt.

If you have any questions related to tax on pension, reach out to us at support@cleartax.in and we will assist you.

Income Tax Slab under Old Tax Regime for Senior Citizens

| Income | 60-80 years | 80 years & above |

| Upto Rs. 3 lakhs | Nil | Nil |

| Rs.3 lakhs to Rs.5 lakhs | 5% | Nil |

| Rs.5 lakhs to Rs.10 lakhs | 20% | 20% |

| Rs.10 lakhs and above | 30% | 30% |

Note: Income Tax Exemption limit is up to Rs. 3 lakhs for individuals aged above 60 years but below 80 years & up to Rs. 5 lakhs for individuals aged above 80 years.

Income Tax Slab under New Tax Regime for Individuals

Under the new tax regime, the tax slabs are the same regardless of the age. The tax slabs for the FY 2024-25 (AY 2025-26) are as follows:

| Tax Slab for FY 2024-25 | Tax Rate |

| Upto Rs. 3 lakhs | Nil |

| Rs. 3 lakhs - Rs. 7 lakhs | 5% |

| Rs. 7 lakhs - Rs. 10 lakhs | 10% |

| Rs. 10 lakhs - Rs. 12 lakhs | 15% |

| Rs. 12 lakhs - Rs. 15 lakhs | 20% |

| More than 15 lakhs | 30% |

Illustration

Mr. Anban retired on 01.10.2024. He receives a pension of Rs. 5,000 per month. On 01.02.2025, he commuted 60% of his pension and received Rs. 3,00,000 as commuted pension.

Case 1: Mr. Anban is a Non-government employee and covered under the Payment of Gratuity Act

Assuming that Mr. Anban is a non-government employee and covered under the gratuity act, his pension exemption will be calculated as follows:

| Particulars | Amount |

| Commuted Pension Received | 3,00,000 |

| (-) Exemption u/s 10(10A) | |

| (1/3 x 3,00,000/60% x 100) | -1,66,667 |

| Taxable Pension | 1,33,333 |

Case 2: Mr. Anban is a Non-government employee and not covered under the Payment of Gratuity Act

Assuming that Mr. Anban is a non-government employee and not covered under the gratuity act, his pension exemption will be calculated as follows:

| Particulars | Amount |

| Commuted Pension received | 3,00,000 |

| (-) Exemption u/s 10(10A) | |

| (1/2 x 3,00,000/60% x 100) | -2,50,000 |

| Taxable Pension | 50,000 |

Case 3: If Mr. Anban is a Government employee

Assuming that Mr. Anban is a government employee, then the entire commuted pension received by him will be fully exempt. However, the uncommuted portion will be taxable under Income From Salary.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption