|

Composition Scheme Rules under GST

Composition Scheme Rules under GST provide for all the procedural compliance w.r.t. intimation for Composition Scheme, the effective date for levy, conditions, and restrictions on the levy, validity of levy and rate of tax.

Latest Updates

5th July 2022

(a) The due date of GSTR-4 for FY 2021-22 is further extended by a late fee waiver up to 28th July 2022 vide Notification 12/2022 dated 5th July 2022.

(b) The due date of CMP-08 for April-June 2022 is extended up to 31st July 2022 vide Notification 12/2022 dated 5th July 2022.26th May 2022

As per the CGST Notification no.7/2022 dated 26th May 2022, the late fee has been waived for the delay in filing GSTR-4 for FY 2021-22, if it is filed between 1st May and 30th June 2022.24th February 2022

Composition taxable persons and those interested to opt into the scheme for FY 2022-23 must submit a declaration on the GST portal in Form CMP-02 by 31st March 2022.28th May 2021

As per the outcome of the 43rd GST Council meeting and CBIC notification,

(1) Interest relief has been provided for filing of CMP-08 for Jan-March 2021 quarter as per which, for any delay, interest is not charged until 3rd May, whereas 9% of reduced interest will be charged if filing is done thereafter until 17th June, and 18% later on.

(2) The due date to file GSTR-4 for FY 2020-21 is extended up to 31st July 2021.

(3) The maximum late fee for GSTR-4 that can be charged will be restricted to Rs.500 per return for nil filing and Rs. 2000 for other than nil filing.1st May 2021

(1) The due date to file GSTR-4 for FY 2020-21 was extended from 30th April 2021 to 31st May 2021.

(2) Form CMP-08 that was due by 18th April 2021 for January-March 2021 has been given a relaxation in the interest charges. No interest for filing on or before 8th May, interest reduced to 9% between 9th May and 23rd May, but charged at 18% thereafter.

(3) The time limit to file ITC-03 by newly opted composition taxable persons for FY 2021-22 is extended up to 31st May 2021.

Intimation and Effective date for Composition Levy

For persons already registered under pre-GST regime

Any person being granted registration on a provisional basis (registered under VAT Act, Service Tax, Central Excise laws etc) and who opts for Composition Levy shall electronically file an intimation in FORM GST CMP-01, duly signed, before or within 30 days of the appointed date.

If intimation is filed after the appointed day, the registered person:

- Will not collect taxes

- Issue bill of supply for supplies FORM GST CMP- 03* must also be filed within 60 days of the exercise of option:

- Details of stock

- Inward supply of goods received from unregistered persons held by him on the date preceding the day of exercise of option

For persons who applied for fresh register under GST to opt scheme

For fresh registration under the scheme, intimation in FORM GST REG- 01 must be filed.

Registered under GST and person switches to Composition Scheme

Every registered person under GST and opts to pay taxes under Composition Scheme, must follow the following:

- Intimation in FORM GST CMP- 02 for exercise option**

- Statement in FORM GST ITC- 3 for details of ITC relating to inputs lying in stock, inputs contained in semi-finished or finished goods within 60 days of commencement of the relevant financial year

Effective date for composition levy

- The option to pay tax under Composition Scheme shall be effective:

- For persons already registered under pre-GST regime: Appointed Day

- Registered under GST and person switches to Composition Scheme: Filing of Intimation

- For persons who applied for fresh register under GST to opt scheme Option to pay tax under Composition Scheme shall be effective from:

- where the application for registration has been submitted within thirty days from the day he becomes liable for registration, such date.

- In the above case, the effective date of registration shall be the date of grant of registration.

Conditions and Restrictions for Composition Levy

- The person opting for the scheme must neither be a casual taxable person nor a non-resident taxable person.

- The goods held by him in stock on the appointed date must not be purchased from a place outside his state. The goods should therefore not be classified as:

- Interstate purchase

- Imported Goods

- Branch situated outside the State

- Agents or Principal situated outside the State

- Where the taxpayers deal with unregistered person, tax must be paid or no stock must be held

- Mandatory display of invoices of the words ” composition taxable person, not eligible to collect tax on supplies”

- Mandatory display of the words “Composition Taxable Person” on every notice and signboard displayed at a prominent place.

- He is not a manufacturer of such goods as may be notified by the Government during the preceding financial year.

Validity of Composition Levy

It depends on the fulfilment of conditions (discussed above), however, an eligible person for scheme may also opt out of the scheme by filing an application. In case Proper Officer has reasons to believe that taxpayer is not eligible for the scheme or contravened any Rules or ACT, he may issue show cause notice followed by an order denying the entailment of the scheme.

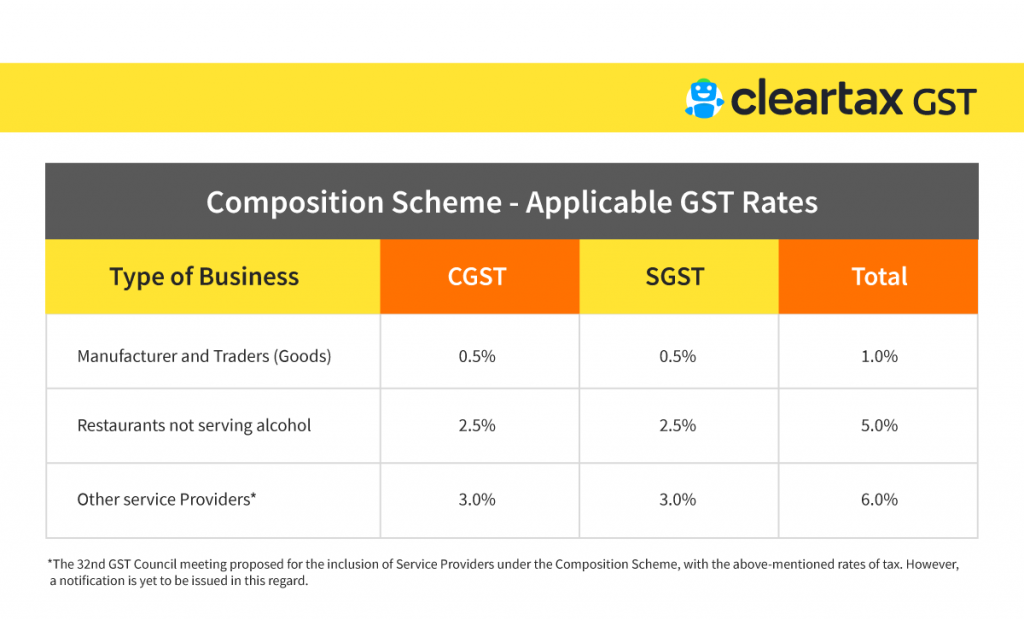

Rate of Tax

The rate of tax prescribed for different categories of registered persons have been described below:

Composition Scheme Rules under GST- Compliance

Composition Scheme Rules under GST provides for submission of different forms meant for respective purposes followed by due date for submission of such forms, which are as follows:

| Form Required | Purpose | Due Date |

| Form GST CMP-01 | To opt into the scheme by provisional GST registration holder(from VAT regime) | Prior to appointed date or within 30 days of the said date |

| Form GST CMP-02 | Intimation of willingness to opt into the scheme for GST registered normal taxpayers | Prior to commencement of Financial Year |

| Form GST CMP-03 | Details of stock and inward supplies from registered and unregistered persons | Within 90 days of the exercise of the option |

| Form GST CMP-04 | Intimation of withdrawal from the scheme | Within 7 days of the occurrence of the event |

| Form GST CMP-05 | Show cause notice on contravention of Rules or Act by a proper officer | On any contravention |

| Form GST CMP-06 | Reply to show cause notice | Within 15 days |

| Form GST CMP-07 | Issue of Order | Within 30 days |

| Form GST REG-01 | Registration under Composition scheme | Prior to the appointed date |

| Form GST ITC-01 | Details of inputs in stocks, semi-finished and finished goods | 30 days of withdrawing option |

| Form GST ITC-03 | Intimation of ITC available | Within 60 days of commencement of the financial year |

All the above-mentioned forms must be duly signed and filed electronically on Common Portal, either directly or through a Facilitation Centre notified by the Commissioner.

Conclusion

Any person who opts for the scheme will be deemed to have been opted for all the places of business having the same registered PAN. Hence, you may not choose any one of all the place of business to be registered under the scheme. Composition Scheme Rules under GST have been targeted to be strict and crisp for the persons availing the Composition Scheme.

To know more about Composition Scheme, its benefits, and drawbacks, and Transition Provisions for your business, do read through our other articles.

Below is the downloadable format (PDF) prescribed by the government for registering as a composition dealer.

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption