|

GST Appeals Basics: Procedure, Time Limit, Rules, Fees, Form

GST appeals is an option for taxpayers to seek relief from a decision passed by tax authorities and courts under the GST law. The GST law provides detailed rules for filing of appeals with timelines. Read on to learn more about the rules, steps and timelines for GST appeals.

Latest Updates

3rd July 2025

CBIC issued the circular specifying the procedure related to review, revision, and appeals for orders passed by Common Adjudicating Authority(CAA). It was clarified that principal commissioner or commissioner of Central Tax shall be reviewing authority u/s 107 and revisional authority u/s 108 of CGST Act, 2017, respectively.

14th May 2025The GSTN issued advisory. Appellate authority must approve the withdrawal of appeal wherever it is submitted after the passing of final acknowledgement. Once the approval is given, the status of appeal changes from ‘Appeal submitted’ to ‘Appeal withdrawn’. Waiver scheme u/s 128A, no appeal must be pending with appellate authority against the demand order. While filing waiver application or in the already filed waiver application, taxpayers need to upload the screenshot of the appeal case folder showing status as “Appeal withdrawn”.

21st December 2024

The GST Council in its 55th meeting, has recommended to amend the proviso to section 107(6) of CGST Act, 2017 and insert a new proviso to section 112(8) of CGST Act, 2017 providing for payment of pre-deposit of 10% for filing appeals before Appellate Tribunal in cases involving only demand of penalty without involving the demand of tax.**The same would be given effect through the relevant circulars/ notifications.

What is an appeal?

Any appeal under any law is an application to a higher court for a reversal of the decision of a lower court. Appeals arise when there are any legal disputes.

What are disputes?

Tax laws (or any law) impose obligations. Such obligations are broadly of two kinds: tax-related and procedure-related. The taxpayer’s compliance with these obligations is verified by the tax officer (through audit, anti-evasion, examining etc.). Sometimes there are situations of actual or perceived non-compliance. If the difference in views persists, it results into a dispute, which is then required to be resolved. The initial resolution of this dispute is done by a departmental officer by a quasi-judicial process resulting into the issue of an initial order known by various names -assessment order, adjudication order, order-in-original, etc. GST Act defines the phrase “adjudicating authority” as any authority competent to pass any order or decision under this Act, but does not include the Board, the First Appellate Authority and the Appellate Tribunal. Thus, in a way, any decision or order passed under the Act is an act of “adjudication”. Some examples are:- cancellation of registration, best judgment assessment, decision on a refund claim, imposition of a penalty.

Steps of appeals under GST

| Appeal level | Orders passed by…. | Appeal to ——- | Sections of Act |

| 1st | Adjudicating Authority | First Appellate Authority | 107 |

| 2nd | First Appellate Authority | Appellate Tribunal | 109,110 |

| 3rd | Appellate Tribunal | High Court | 111-116 |

| 4th | High Court | Supreme Court | 117-118 |

Should every appeal be made to both CGST & SGST authorities? No. As per the GST Act, CGST & SGST/UTGST officers are both empowered to pass orders. As per the Act, an order passed under CGST will also be deemed to apply to SGST. However, if an officer under CGST has passed an order, any appeal/review/ revision/rectification against the order will lie only with the officers of CGST. Similarly, for SGST, for any order passed by the SGST officer the appeal/review/revision/rectification will lie with the proper officer of SGST only.

Filing of a GST appeal

To file an appeal under GST to the Appellate Authority, you can follow the procedure detailed in this article here.

Time limit for filing a GST appeal

An applicant can file an appeal before the Appellate Authority within three months from the date of communication of the disputed order. Further, the Appellate Authority may condone a delay of up to one month if they are satisfied that there was a sufficient cause for such delay.

General rules for filing GST appeals

All appeals must be made in prescribed forms along with the required fees. Fee will be – The full amount of tax, interest, fine, fee and penalty arising from the challenged order, as admitted by appellant, AND –10% of the disputed amount In cases where an officer or the Commissioner of GST is appealing then fees will not be applicable.

Can an authorised representative appear in court?

Yes. Any person required to appear before a GST Officer/First Appellate Authority/Appellate Tribunal can assign an authorised representative to appear on his behalf, unless he is required by the Act to appear personally. An authorised representative can be-

- a relative

- a regular employee

- a lawyer practising in any court in India

- any chartered accountant/cost accountant/company secretary, with a valid certificate of practice

- a retired officer of the Tax Department of any State Government or of the Excise Dept. whose rank was minimum Group-B gazetted officer

- any tax return preparer

Retired officers cannot appear in place of the concerned person within one year from the date of their retirement.

Appeal cannot be filed in certain cases

The Board or the State Government may, on the recommendation of the Council, fix monetary limits for appeals by the GST officer to regulate the filing of appeal and avoid unnecessary litigation expenses Can all decisions be appealed against? No. Appeals cannot be made for the following decisions taken by a GST officer-

- An order to transfer the proceedings from one officer to another officer;

- An order to seize or retain books of account and other documents;

- An order sanctioning prosecution under the Act; or

- An order allowing payment of tax and other amount in installments

A person unhappy with any decision or order passed against him under GST by an adjudicating authority can appeal to the First Appellate Authority. If they are not happy with the decision of the First Appellate Authority they can appeal to the National Appellate Tribunal, then to High Court and finally Supreme Court.

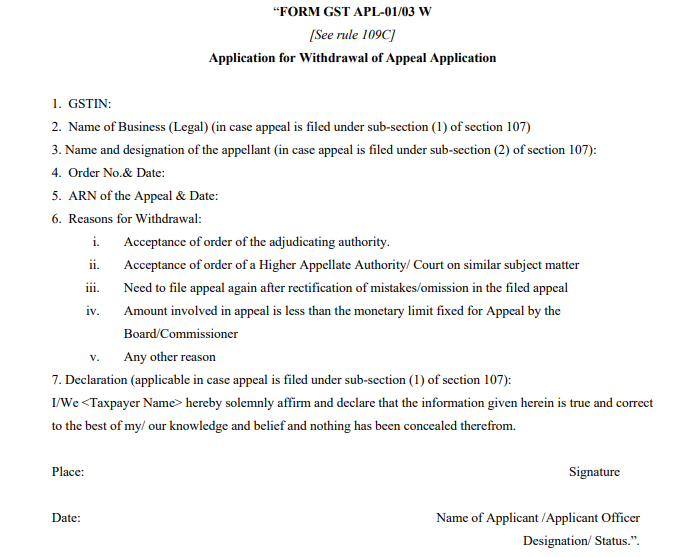

Withdrawal of a GST appeal

In the 48th GST Council meeting, it was decided to provide an option of withdrawal of a GST appeal that has already been filed. This move was made with the intention of reducing the number of litigations that the appellate authorities have to deal with. In this regard, a new Rule 109C was inserted in the CGST Rules via Notification No.26/2022- Central Tax.

Rule 109C states that the applicant can file an application for withdrawal of an appeal at any time before the show cause notice or order under Section 107(11) is issued, whichever is earlier. This is in respect of any appeal filed in Form GST APL-01 or Form GST APL-03. The application for withdrawal of the appeal will need to be submitted using the new Form GST APL-01/03W.

It is important to note here that in cases where the final acknowledgment in Form GST APL-02 has been issued, then the withdrawal of the said appeal will require the approval of the appellate authority. The appellate authority must make a decision on the application for withdrawal of the appeal within seven days of the applicant filing the same. Any fresh appeal filed by an appellant after such withdrawal should be within the time limits specified under Section 107.

New framework for multi-jurisdictional GST disputes

The CBIC issued an important Circular, CGST Circular No. 250/07/2025-GST, on 24th June 2025. According to the Circular, the Principal Commissioner or Central Tax Commissioner will act as the reviewing authority under CGST Section 107. The Common Adjudicating Authorities (CAAs) functions and reports to the Principal Commissioner.

The same official will also be vested with the revisional powers under CGST Section 108, both of which pertain to handling appeals against demand or adjudication orders. The Commissioner (Appeals) shall handle the appeals against orders passed by CAAs. They have the territorial jurisdiction over the Principal Commissioner or Commissioner of Central Tax supervising the adjudicating authority.

Earlier, there was no framework formally given by law about who could review or hear appeal against decisions by the CAA. Post-adjudication process was not addressed in the previous GST Circulars. It led to jurisdictional confusions, delays, and procedural lapses in high-value investigations of cases pertaining to tax evasions.

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption