|

Casual Taxable Person under GST

A Casual Taxable Person (CTP) means a person who supplies taxable goods or services occasionally in a taxable territory where he does not have a fixed place of business. The person can act as a principal or agent or in any other capacity to supply goods or services for the furtherance of business.

Example: Mr Ravi having a place of business in Bangalore providing management consultancy services in Hyderabad where he has no place of business. Hence Mr Ravi has to register as a casual taxable person in Hyderabad before providing such services.

Note-

a. Person includes individuals, Hindu Undivided Family (HUF), company including government company, firm, limited liability partnership, an association of persons, a body of individuals, co-operative society, local authority, government including a corporation.

b. Principal place of business means the place of business specified as the principal place of business in the certificate of registration

Registration of a Casual Taxable Person

The liability to register under GST arises when the person is a supplier and the aggregate turnover in the financial year is above the threshold limit of Rs. 40 lakhs. However, there are certain categories of suppliers who are required to get compulsory registration irrespective of their turnover i.e. the threshold limit of Rs. 40 lakhs is not applicable to them. One such supplier would be a Casual Taxable Person (hereafter referred as CTP).

- A CTP cannot opt for a composition scheme.

- A casual taxable person must register at least 5 days before starting their business.

- A CTP has to obtain a temporary registration which is valid for a maximum period of 90 days in the state from where he seeks to supply as a casual taxable person.

- A CTP is required to make the advance deposit of GST (based on an estimation of tax liability).

Let’s take our previous example, Say Mr.Ravi estimates his taxable services at Rs. 100,000. He is required to make an advance deposit of Rs.18,000 (18% of Rs.100,000) to obtain temporary registration.

Note - Taxable persons who supply the specified handicraft goods are not required to register as CTP i.e. they are only required to obtain GST registration when their overall annual turnover exceeds Rs. 20 lakhs.

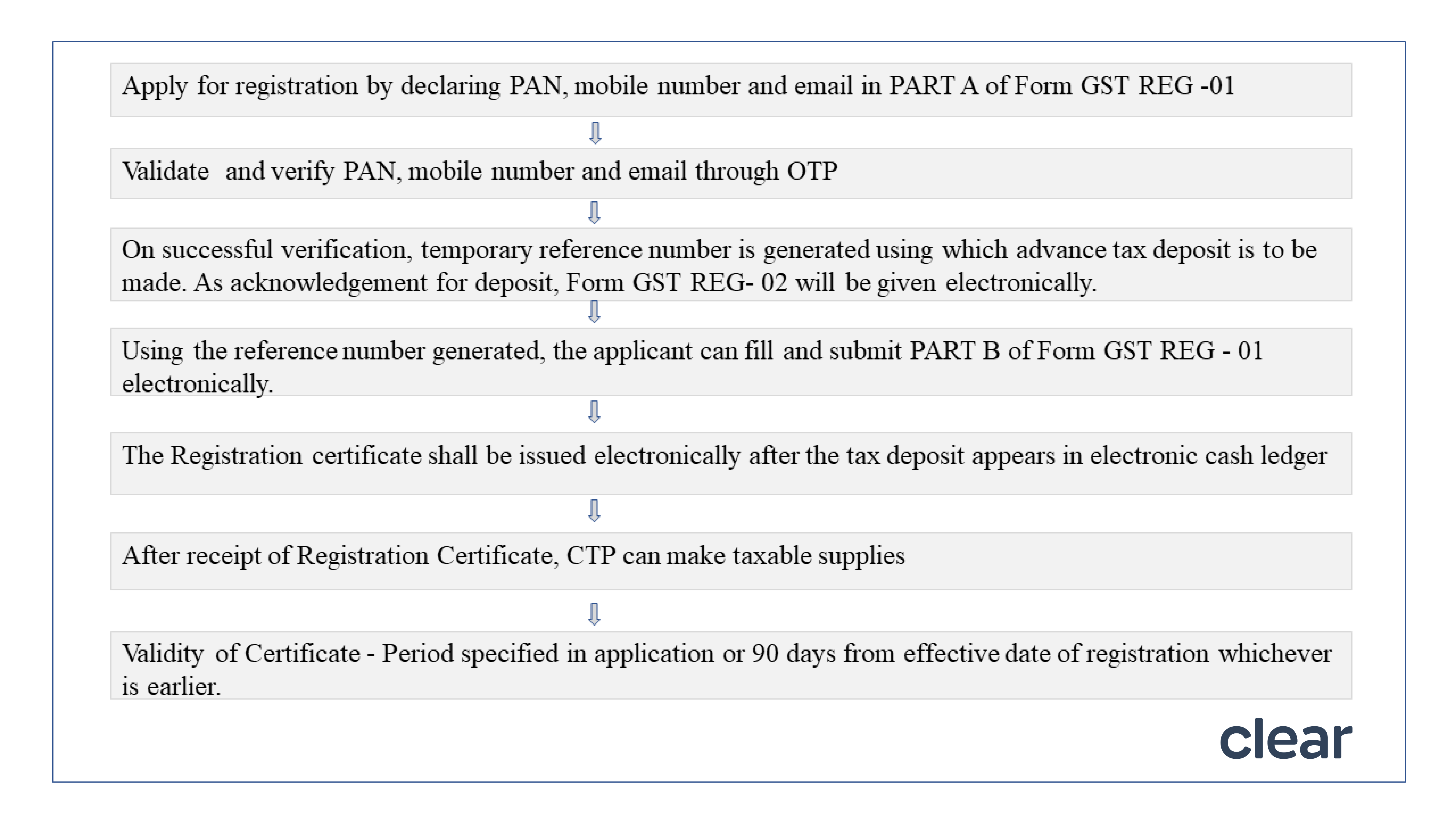

Registration Process

Extension of period of Registration

Apply in FORM GST REG-11 before the end of validity of registration. An extension can be made for a further period not extending 90 days. The extension will be allowed only on deposit of additional tax liability for the extended period.

Returns to be furnished

The casual taxable person is required to furnish the following returns

Form | Due Date |

Form GSTR-1 ( Details of outward supplies of goods or services) | On or before the 11th of the following month |

Form GSTR-3B (Summary of ITC, purchases and tax liability) | On or before the 20th of the following month |

However, if a CTP has opted for the QRMP scheme, he has to file IFF/GSTR-1 and GSTR-3B on a quarterly basis.

A casual tax person is not required to file an annual return as required by a normally registered taxpayer.

Note – All Forms can be submitted at the common portal, either directly or through a Facilitation Centre notified by the Commissioner.

Refund by a casual taxable person

CTP is eligible for the refund of any amount deposited in excess of tax liability which will be refunded after all the necessary returns have been furnished for the Registration period. Application for Refund of balance in excess of tax liability in the electronic cash ledger can be claimed in Form GST RFD-01 under the category “Refund of excess balance in the electronic cash ledger”.

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption