|

GSTR-3B v/s GSTR-2A on GST Portal

GSTR-3B is used to enter the summary output and input tax credit (ITC) details so that the net tax liability can be calculated and paid. Before filing GSTR-3B, it is important to check Form GSTR-2A since it shows us the details of the invoices uploaded by our supplier. It also allows a taxpayer to ensure that the ITC claims on invoices not appearing in GSTR-2A be avoided from 1st Jan 2022 (earlier, 5% was allowed).

We will need GSTR-2A data to accurately determine how much ITC can be claimed and avoid any undue interest liability. From August 2020, taxpayers can conveniently claim ITC every period as per GSTR-2B, which is a static or constant auto-drafted ITC statement.

*Taxpayers can claim provisional ITC without any restriction for March 2020 to August 2020, as per CGST notification number 30/2020 dated 3rd April 2020.

How does ClearTax GST simplify ITC Matching & Liability Matching?

Clear GST (formerly called ClearTax GST) software allows easy comparison of GSTR-2A/2B and GSTR-1 with GSTR-3B respectively. If you have added the business and GSTIN details, it is a cakewalk.

(1) ITC Matching is made easy at GSTIN-level and PAN-level as follows:

Step 1: Click on the “GSTR-2A v/s GSTR-3B” tile.

Step 2: Select the GSTIN you want to conduct the comparison.

Step 3:Select the Financial Year. The report gets generated month-wise at both GSTIN-level and PAN-level for further download or use. PAN-level Report is as given below:

GSTIN-level Report is as given below:

(2) Advanced Reconciliation Tool for matching purchase register with GSTR-2A across months: One can get suggested matches and send mismatch details via email to suppliers.

Step 1: On the homepage, click on “Match & Reconcile”.

Step 2: Select the GSTIN you want to conduct the comparison.

Step 3: Select the Financial Year. Run the reconciliation by using one-click import feature for GSTR-2A and Purchase register.

For more details, you can get a FREE demo on how to perform GST reconciliation.

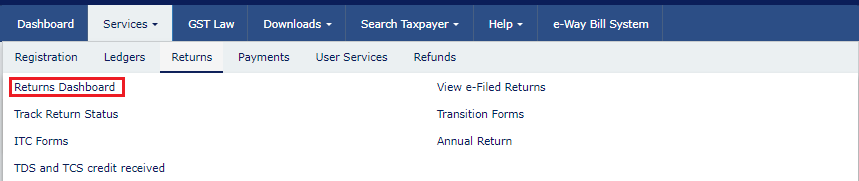

How to Compare GSTR-2A v/s GSTR-3B on the GST Portal?

Step 1: Log in to the GST portal using your credentials

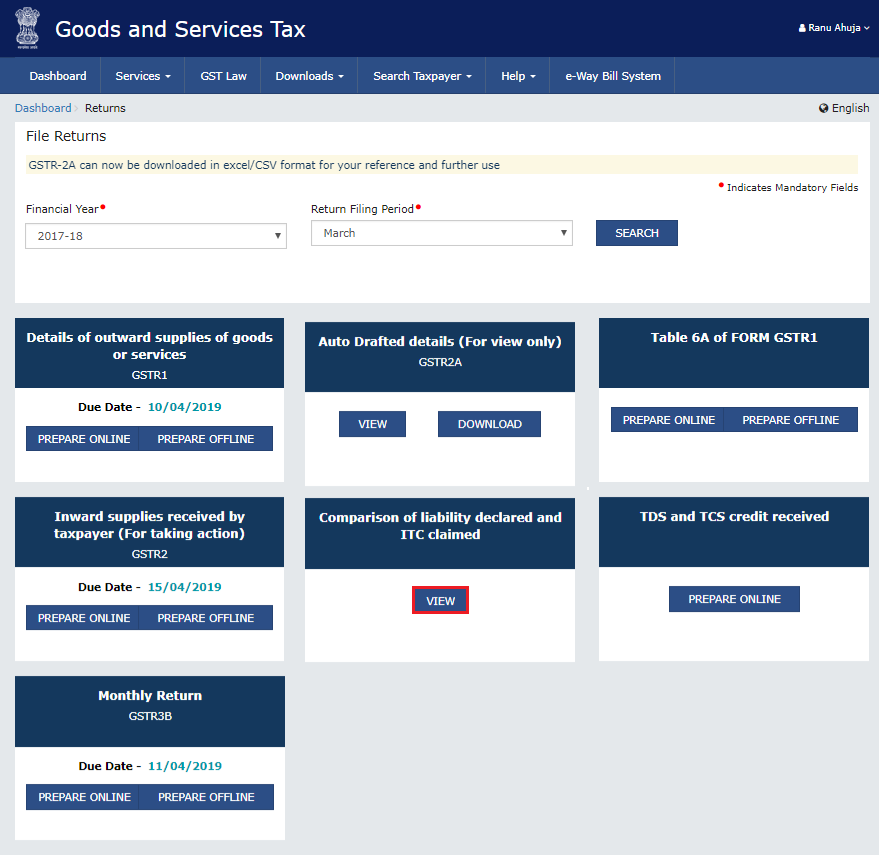

Step 2: Click on ‘Returns Dashboard’ OR Go to Services > Returns > Returns Dashboard.

Step 3: Choose the financial year and return filing period from the drop-down list.

Step 4: To compare the GSTR-3B with GSTR-2A, click on the ‘View’ button under the ‘Comparison of liability declared and ITC claimed’ tile.

The GSTIN, legal/trade name, and the financial year along with the date and time of the latest report generation will be displayed.

Below that, the ‘Credit and Liability Statement’ gets displayed, as shown below:

The following data is compared between two returns:

- Tax liability as declared in GSTR-1 and GSTR-3B

- ITC claimed in GSTR-3B and ITC available as per GSTR-2A

Click on ‘DOWNLOAD’ to get the statement in excel format. Step 5: Choose reports to further sort the data compared. Click on the following buttons to access these reports.

Each of them is detailed below:

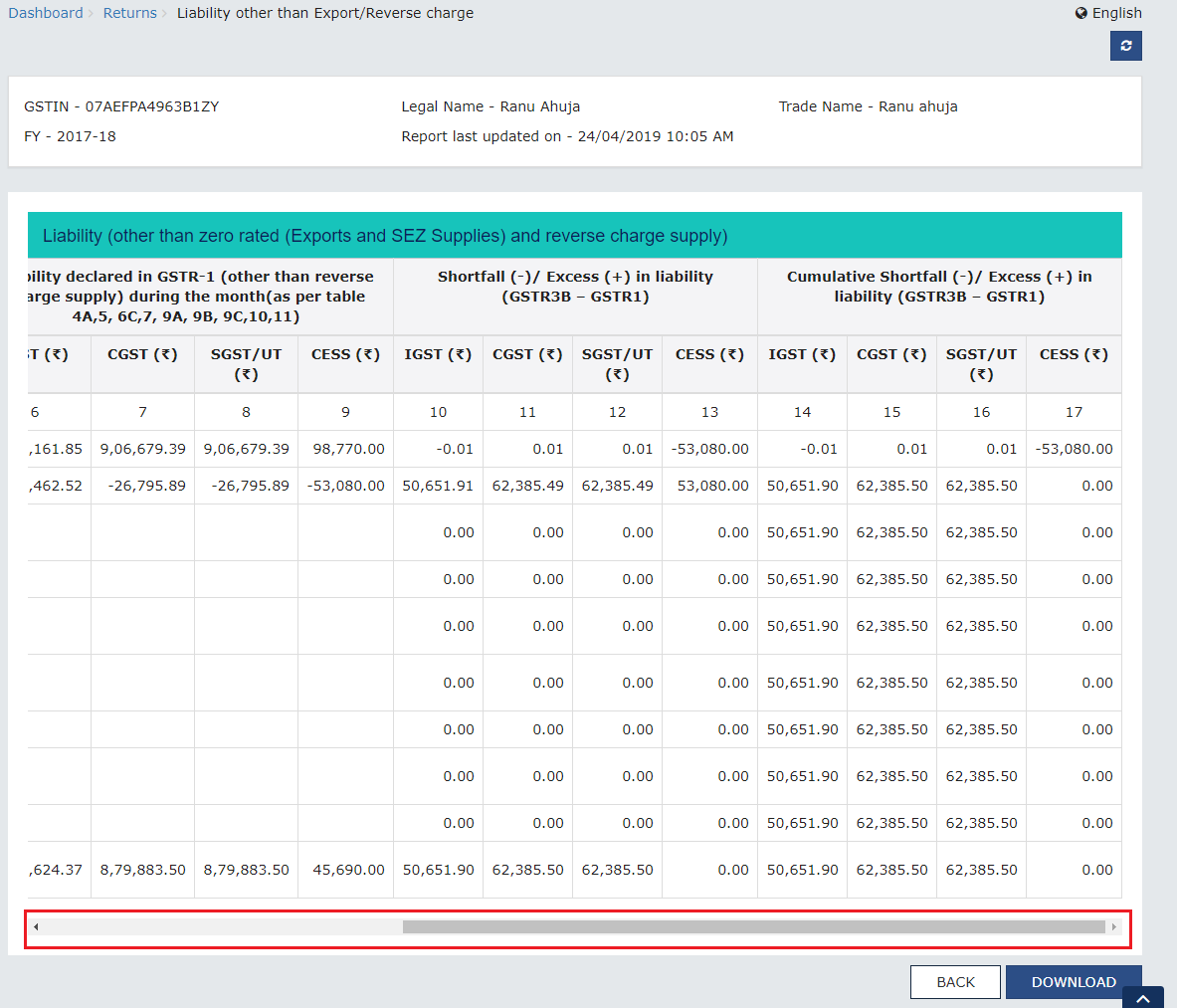

A. LIABILITY OTHER THAN EXPORT/REVERSE CHARGE

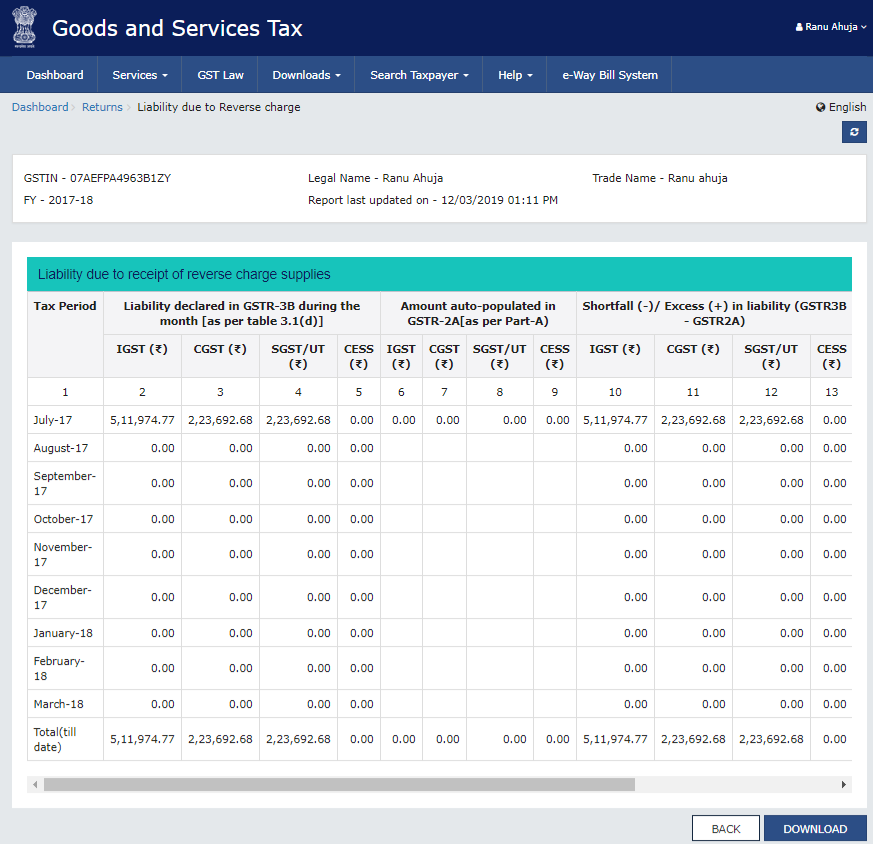

B. LIABILITY DUE TO REVERSE CHARGE

C. LIABILITY DUE TO EXPORT AND SEZ SUPPLIES

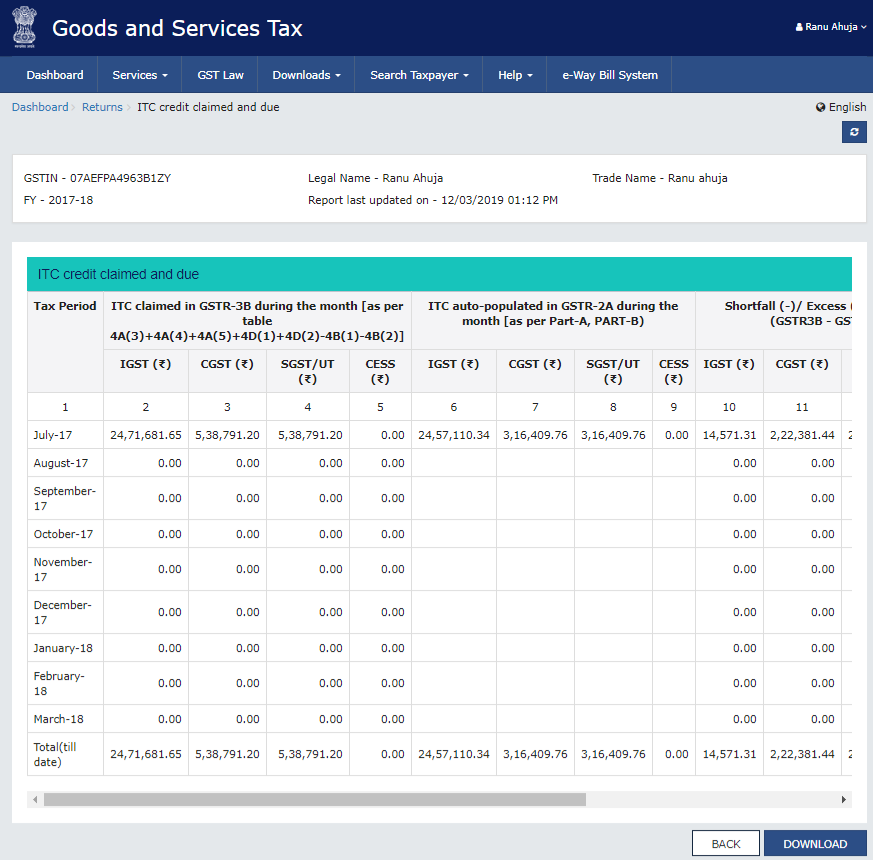

D. ITC CREDIT CLAIMED AND DUE

Important notes:

- These reports can be downloaded in excel format too.

- The comparison is classified as CGST, SGST, IGST and Cess.

- On comparing the data, the last two columns will display the shortfall/excess (including the cumulative shortfall/excess) for the financial year.

A. Liability Other Than Export/Reverse Charge (GSTR-3B v/s GSTR-1): The table compares tax liability between GSTR-3B and GSTR-1 for outward supplies. The data excludes zero-rated supplies (i.e., exports and SEZ supplies) and inward supplies liable to reverse charge. The table is given below:

Following tables of GSTR-3B and GSTR-1 are compared in columns 1 and 2:

- Tables 3.1(a) of Form GSTR-3B for the relevant period

- Total of tables 4a, 5, 6C, 7, 9A, 9B, 9C, 10, and 11 of Form GSTR-1 (other than reverse charge supply) for the relevant period.

B. Liability Due to Reverse Charge (GSTR-3B v/s GSTR-2A): The table compares tax liability between GSTR-3B and GSTR-1 for inward supplies liable to reverse charge by comparing the following tables:

- Table 3.1(d) of Form GSTR-3B for the relevant period

- Part A of Form GSTR-2A for the relevant period

C. Liability due to Export and SEZ Supplies (GSTR-3B v/s GSTR-1): The table compares the liability between GSTR-3B and GSTR-1 on the zero-rated (i.e., exports and SEZ supplies) outward supplies. The information in this table is sourced from the following:

- Table 3.1(b) of Form GSTR-3B of the relevant period

- Total of tables 6A, 6B, 9A, 9B, and 9C of Form GSTR-1 (zero-rated supplies) for the relevant period

D. ITC Credit Claimed and Due: This table can be used by taxpayers to compare the ITC to be taken in GSTR-3B with data submitted by their suppliers in their respective GSTR-1. It shall also include a comparison with data declared by their respective ISD distributors in their GSTR-6. The information in this table is sourced from the following:

- Total of tables 4A(3) + 4A(4) + 4D(1) + 4D(2) – 4B(1) – 4B(2) (ITC claimed) of Form GSTR-3B for the relevant period

- Total of auto-populated information available in Part-A and Part-B of Form GSTR-2A sourced from GSTR-1 (supplier) and GSTR-6 (ISD distributor), respectively

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption