Call Now

Call Now

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act

The last date to file Income Tax Return (ITR) for FY 2025-26 (AY 2026-27) is 31st July 2026 for taxpayers filing ITR-1 or ITR-2. However, for taxpayers required to file ITR-3 or ITR-4 and not requiring tax audit, the last date is 31st August 2026.

Taxpayers failing to file ITR within these due date can still file a belated return before 31st December 2026. However, taxpayers will be required to pay late fees under Section 234F for filing ITR late.

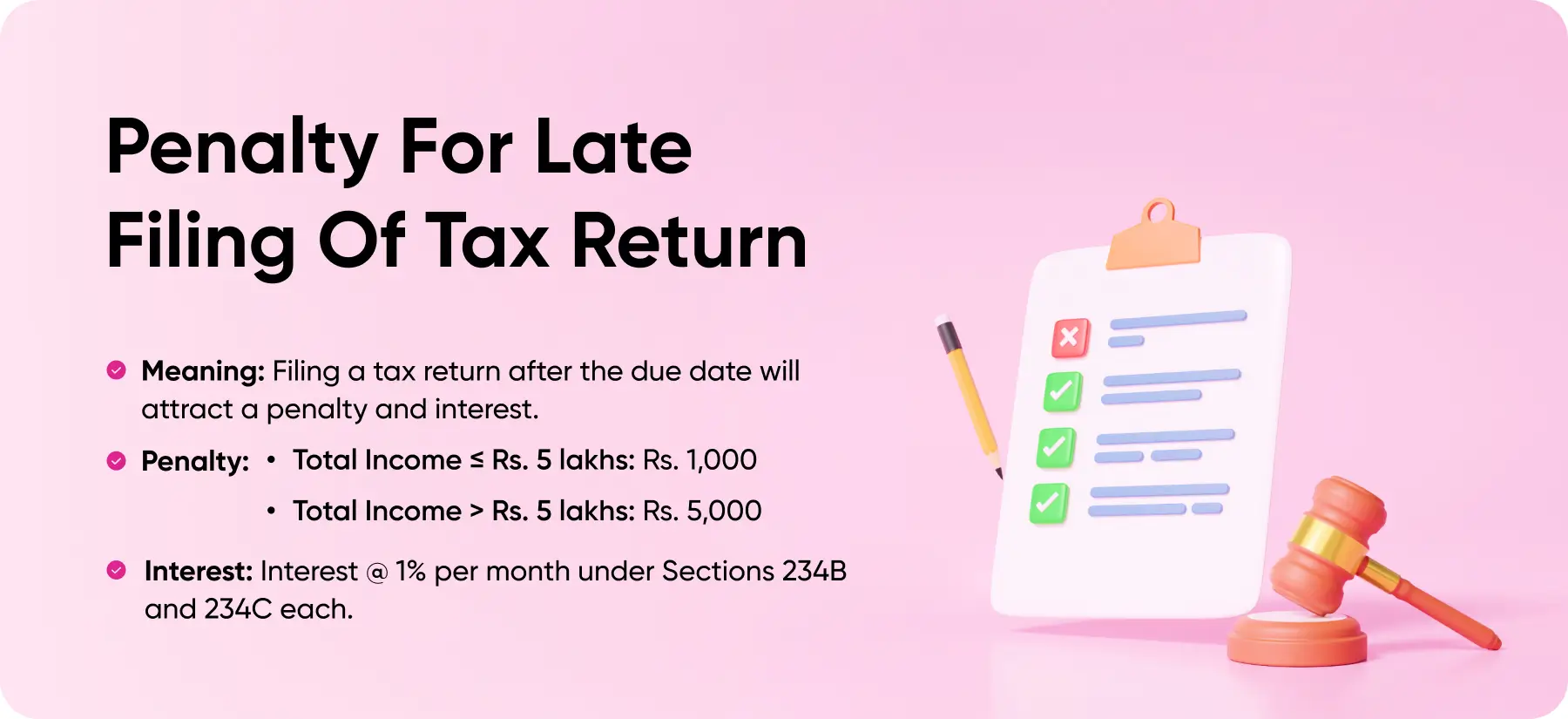

What is the Penalty for Late Filing of ITR?

Under Section 234F of the Income Tax Act, if you file your ITR after the due date, you may have to pay a maximum penalty of Rs. 5,000

For FY 2025-26, if you file your return before the specified due dates, no penalty is levied. However, returns filed after 31st July 2026 or 31st August 2026 will attract a penalty of up to Rs. 5,000. As a relief to small taxpayers, if total income does not exceed Rs. 5 lakh, the penalty for late filing is restricted to Rs. 1,000 only. Please note that section 234F is a fee for late filing, not interest.

Late Filing Fee Details

The late filing fees when the return of income is filed beyond the due date is explained below.

| Annual Taxable Income | Late Filing Fees u/s 234F |

| Up to Rs. 5 lakhs | Rs 1,000 |

| More than Rs 5 lakhs | Rs 5,000 |

Note: No late fee needs to be paid as long as the returns are filed within the due date.

Due Date for Revising Your Return

If you make a mistake while filing your ITR, you can still revise the return within 31st December 2026 of the assessment year. However, in Budget 2026 it was proposed to extended the due date to file revised returns to 31st March of the assessment year but with late fees if filed after 31st December.

This means for FY 2025-26, if a taxpayers revises ITR before 31st December 2026 there is no late fees required to be paid for filing revised returns. But if the revised return is filed between 31st December 2026 and 31st March 2027, late fees will be levied as per Section 234I.

Payment of Interest for Late Filing under Section 234A

If you fail to file your income tax return on or before the due date, you will be liable to pay interest at 1% per month or part of a month on the unpaid tax amount, as per Section 234A of the Income Tax Act. It is important to note that your ITR cannot be filed without payment of the due taxes.

The calculation of interest begins immediately after the due date. Therefore, the longer you delay filing, the higher your interest liability will be.

Carry Forward of Losses is Not Permitted if ITR is Filed Late

If you have incurred losses during the financial year, such as capital losses or business losses, it is crucial to file your income tax return within the due date. Filing your return after the deadline will disqualify you from carrying forward these losses to offset against future income, leading to higher tax liability in subsequent years.

However, there is an exception for losses under the head ‘Income from House Property’, which can still be carried forward even if the return is filed after the due date. Unabsorbed depreciation from the businesses can also be carried forwarded even if the returns are not filed within the due date.

No Option to Opt for Old Tax Regime if ITR is Filed Late

If you file your ITR after the due date, you will be mandatorily taxed under the New Tax Regime. In such cases, taxpayers cannot choose the Old Tax Regime, which means that if you have significant deductions or exemptions to claim, you will lose out on these benefits and your tax liability may be higher under the new tax regime.

Delay in Receiving Refunds

If you are entitled to a tax refund for excess taxes paid, it is important to file your ITR before the due date to ensure that you receive your refund without delays. Filing your return late can significantly postpone the processing of your refund.

Other Consequences of Filing Return in Delay

Apart from consequences from taxation perspective, there are several other factors that may be adversely affected when returns are not filed within the due date. Non filing returns on time may result in adversities in loan sanction process, VISA processing, and lower financial discipline and credit worthiness. Therefore, it is advised to file the returns well before the due date and avoid the negative consequences of delays.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption