What is Section 194D and Section 194DA under Income Tax Act?

Similar to tax deductions done at various income sources such as salary, interest income, and house rent, tax deductions at source (TDS) are also required to be done on insurance commission and life insurance premium payments.

Section 194D and Section 194DA under the Income Tax Act, 1961 are the provisions applicable respectively. Let us look into these provisions in detail.

Budget 2025 Update

In the budget 2025, the threshold limit for deduction of tax under section 194D has been increased from Rs. 15,000 to Rs. 20,000 which will be effective from 1st April, 2025.

What is Section 194D?

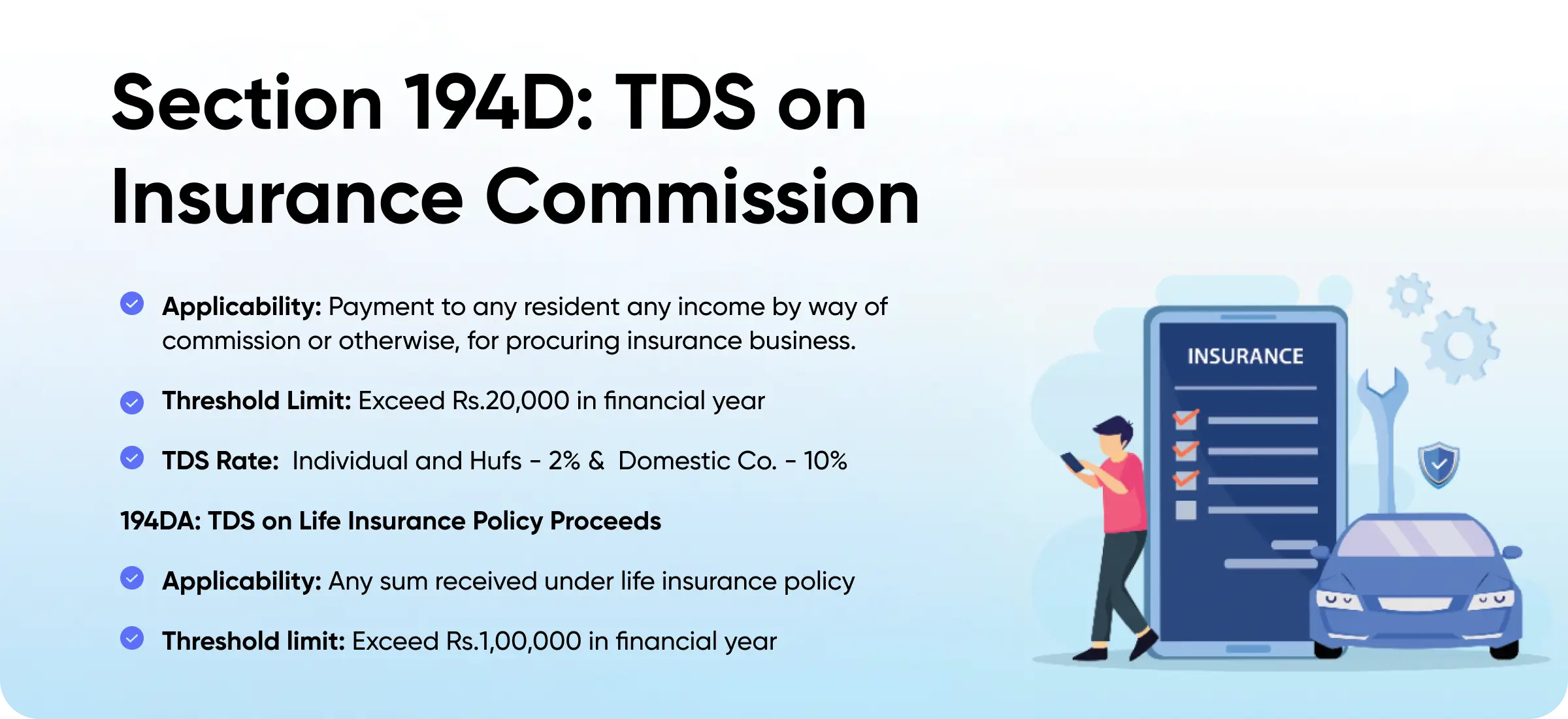

Section 194D basically covers TDS on insurance commission.

Any payments made by way of:

- Any remuneration/reward in the form of commission or otherwise,

- For soliciting or procuring insurance business (including business relating to the continuance, renewal or revival of policies of insurance)

The deduction must be made at the time of crediting the money to the payee’s account or at the time of payment in the form of cash, cheque, draft, or any other mode.

Tax is deductible only if the amount paid or payable or the aggregate of the amounts of such income paid or payable during the financial year exceeds Rs 15,000.

If you purchase any life insurance plans (other than ULIP) on or after April 1, 2023, and the aggregate premium exceeds INR 5,00,000 in a fiscal year, the money received on maturity will be taxable. Section 10(10D) will not provide an exemption to anyone.

Who is Eligible under Section 194D?

Any person who makes a payment to a resident person (Individuals, Hindu Undivided Family(HUF), companies or other taxpayers) in the form of remuneration or reward as part of the insurance business should deduct tax.

The provisions of TDS deduction under Section 194D are applicable to resident individuals only, in the case of non-residents Section 195 will be applicable.

Time Limits of Deduction of TDS for Section 194D?

Tax is deducted at the earlier of the following cases:

- At the time of credit of commission in the payee’s account.

- When the actual payment is made in cash, cheque, draft, or other modes.

Rate of TDS Deduction under Section 194D

According to Section 194D, the tax is deducted at different rates based on the type of payee:

- Individuals or HUF: 5%*

- Domestic companies: 10%

- Payee does not provide PAN: 20%

*It is to be noted that this rate is proposed to be reduced to 2% with effect from 1st April 2025.

You must also know that surcharge and health and education cess will not be applicable to these rates.

Exceptions under Section 194D

Tax need not be deducted from the amount the payer credits to the payee’s account in the following cases:

- The commission paid is within Rs 15,000.

- A self-declaration is available through Form 15G/15H.

Penalty for Late Deduction

If the deductor forgets to deduct TDS when sending a payment, interest is owed. The deductor must pay 1% interest each month or part of a month from the day the TDS was deductible until the date of actual deduction.

What is Section 194DA?

Most people in India purchase insurance products from insurers such as LIC to guarantee their future. Yet, many consumers are unaware that if the payment for a life insurance policy, including the bonus amount on maturity, exceeds Rs 1 lakh, TDS is levied under Section 194DA if the policy is not exempt under Section 10(10D), Click here to know more.

The concept of TDS on life insurance proceeds was introduced in Budget 2019, for all the maturity payments made on or after 1 September 2019.

Rate of TDS under Section 194DA

The tax must be deducted at the rate of 5% on only the ‘income part’ of the payment. This rate has been proposed to be reduced to 2% with effect from 1st October 2024. This means TDS will be applicable only on the amount exceeding the total of the premiums paid by the insured.

TDS rate increased to 20% in case the deductee fails to submit the PAN number.

There is no need to deduct taxes if the aggregate payable amount is within Rs 1 lakh. If the person has received the amount under the keyman insurance policy, the amount is taxable.

For example, consider Mr V received a maturity amount of Rs 8 lakh from his life insurance policy. Mr V has paid an amount of Rs 3 lakh as a premium for the policy over a period of 10 years.

In this case, the maturity amount is above Rs 1 lakh. Hence, the maturity proceeds will be paid after deducting 5% TDS.

In this case, the TDS would be Rs 25,000 (5% on Rs.5 lakh). After deduction, Mr V will receive Rs 7,75,000.

Exemptions under Section 194DA

- Any sum received pursuant to sections 80DD(3)

- The LIC policy is purchased after April 1, 2003, but before March 31, 2012, and the premium paid is no more than 20% of the total guaranteed.

- The LIC insurance is purchased on or after April 1, 2012, and the premium paid does not exceed 10% of the sum guaranteed.

- If the policy is issued on or after April 1, 2013, and the premium paid does not exceed 15% of the total assured. It only applies if the person additionally has a handicap as defined in Sections 80U and 80DDB.

TDS Certificate under Section 194DA

The Deductor or payer shall issue a quarterly TDS certificate to the deductee in form 16A. The deductor can download the form from the Traces and the deductee can see the same in their form 26AS.

Exemptions under Section 10(10D)

According to section 10 (10D), any sum received under the LIC policy including the amount of bonus is exempted.

This section has the following exemptions to it:

- Any amount received under Section 80DD(3).

- Any amount received under keyman insurance policy.

- LIC policy bought after 1st April 2003 but before 31st March 2012 and premium is more than 20% of the sum assured.

- LIC policy is bought after 1st April 2012 and the premium paid is more than 10% of the sum assured.

- LIC policies bought for persons with disability or severe disability according to Section 80U, or for individuals suffering from ailments covered under Section 80DDB after 1st April 2013, and the premiums are more than 15% of the sum assured.

There is no ceiling limit for claiming exemption under Section 10(10D) unless the above-mentioned conditions are satisfied.

Difference between 194D & 194DA

Particulars | 194D | 194DA |

Applicability | Insurance commission (for procuring Insurance business)

| Payment in respect of life insurance policy |

Who shall Deduct | Any person responsible for paying to a resident any income by way of remuneration or reward, whether by way of commission or otherwise, for soliciting or procuring insurance business (including business relating to the continuance, renewal or revival of policies of insurance) | Any person responsible for paying to a resident any sum (maturity amount) under a life insurance policy, including the sum allocated by way of bonus on such policy, other than the amount not includible in the total income under clause (10D) of section 10 |

When to deduct | at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier | at the time of payment thereof |

Limit | Rs. 15,000 | Rs. 1,00,000 |

Rate | Individuals or HUF: 5% * Domestic companies: 10% Payee does not provide PAN: 20% *This rate is proposed to be reduced to 2% with effect from 1st April 2025. | 5% only on the Income part of the Life Insurance policy i.e. the amount which the payee will receive on maturity after deducting the premium paid. This rate has been proposed to be reduced to 2% with effect from 1st October 2024. |

Exemption | The commission paid is within Rs 15,000. A self-declaration is available through Form 15G/15H.

| Any amount received under section 80DD(3) or 80DDA(3) LIC policy is bought after 1st April 2003 but on or before 31st March 2012 and the premium paid is not more than 20% of the sum assured. LIC policy is bought on or after 1st April 2012 and the premium paid is not more than 10% of the sum assured. If the policy is issued on or after 1st April 2013 and the premium paid is not more than 15% of the sum assured. It applies only in case of also such a person suffers from a disability as per Section 80U & 80DDB.

|

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption