Call Now

Call Now

Tax Planning Meaning, Types, Importance & Objectives

Paying taxes on hard-earned income is something everyone feels uneasy about. Naturally, we all seek ways to minimise our tax liabilities—this process is known as tax planning. Tax planning is crucial because it not only helps reduce the amount you owe but also allows you to manage your finances more effectively. In this article, we will discuss the concept of tax planning and its importance.

What is Tax Planning?

Tax planning involves strategically organising your financial affairs to ensure that, while fully complying with the provisions of the Income-tax Act, 1961, you take maximum advantage of all exemptions, deductions, rebates, allowances, and other benefits available under the law. The goal is to minimise your tax liability to the maximum extent possible without violating any legal requirements.

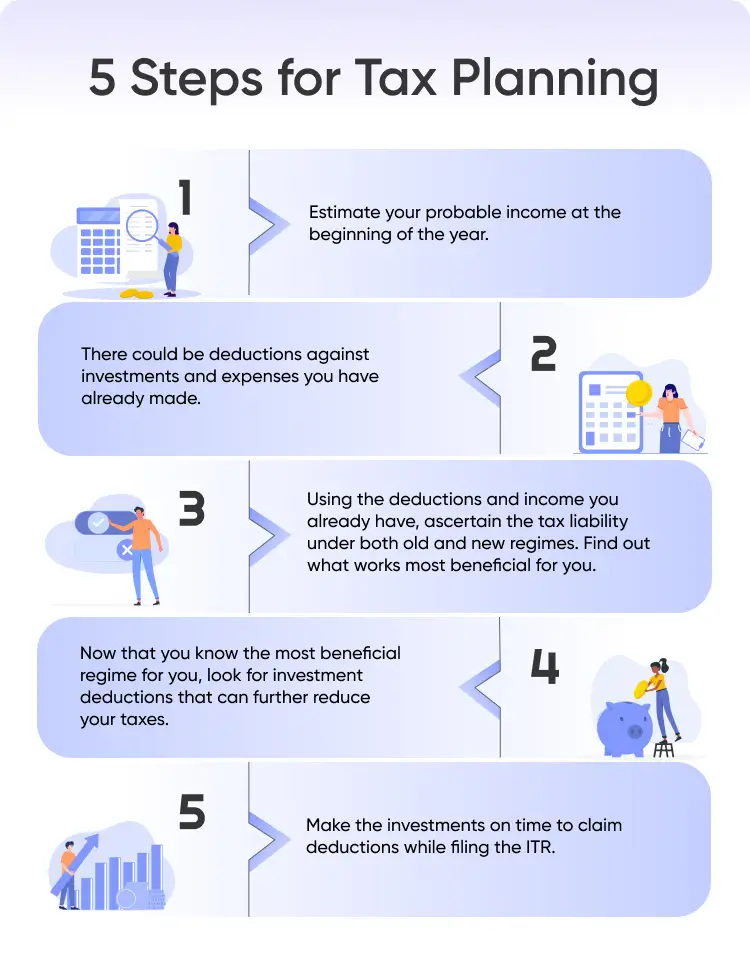

What are the Objectives of Tax Planning?

The main objectives of tax planning are as follows:

- Reduction of Taxes: The purpose of tax planning is to minimise tax liability as much as possible by utilising the deductions, exemptions, rebates, and other benefits available under the Income-tax Act, 1961.

- Increase Savings: Tax planning seeks to maximise savings by optimising tax deductions, exemptions, and incentives. Individuals can boost their savings and direct more funds toward achieving financial goals, investments, and wealth building.

- Avoid Notices: Tax planning helps prevent notices from the tax department by ensuring compliance with the provisions of the Act.

- Financial Stability: Tax planning helps individuals and businesses achieve financial stability by optimising tax liabilities.

Importance of Tax Planning

Tax planning is essential because it minimises your tax liability by smartly using deductions and exemptions available under the Act. It will provide better allocation of resources toward savings or investments. It also ensures legal compliance by reducing the risk of audits, penalties, or fines due to errors or missed deadlines. Additionally, effective tax planning improves cash flows, reduces financial risks, and helps manage taxes efficiently. These are very essential for long-term financial stability and security. Finally, it will enable people to make better financial decisions, avoid surprises, and achieve their financial objectives.

Limitations of Tax Planning

Effective tax planning requires much time and expertise. Many individuals and small businesses may not have the resources to be updated on tax laws or to hire professional advisors, and therefore, may rush or inadequately plan. Tax laws are constantly changing, and what was once an effective strategy may become obsolete or even illegal. This unpredictability creates legal risks for individuals and businesses relying on outdated tax planning methods.

Types of Tax Planning

The types of tax planning are:

- Permissive Tax Planning: This type involves using all the exemptions and deductions, available under tax laws to legally minimise tax liabilities.

- Purposive Tax Planning: The tax strategies aim at achieving specific financial goals such as investing in shares or buying a new phone.

- Short-term Tax Planning: It is for minimisation of taxes for the present fiscal year and thus making proper decisions on time.

- Long-term Tax Planning: It involves long-range strategies and considerations of future financial goals and obligations.

Important Deductions Used for Tax Planning in India

The major deductions that can be used to reduce the tax burden are as follows:

Section | Deduction on | Allowed Limit (maximum) FY 2022-23 |

80C | Investment in PPF – Employee’s share of PF contribution – NSCs – Life Insurance Premium payment – Children’s Tuition Fee – Principal Repayment of home loan – Investment in Sukanya Samridhi Account – ULIPS – ELSS – Sum paid to purchase deferred annuity – Five year deposit scheme – Senior Citizens savings scheme – Subscription to notified securities/notified deposits scheme | Rs. 1,50,000 |

80CCC | For amount deposited in annuity plan of LIC or any other insurer for a pension from a fund referred to in Section 10(23AAB) | |

80CCD(1) | Contribution to NPS account by employee | |

80CCD(2) | Employer’s contribution to NPS account | Maximum up to 10% of salary |

80CCD(1B) | Additional contribution to NPS | Rs. 50,000 |

80TTA(1) | Interest from Savings account | Rs. 10,000 |

80TTB | Exemption of interest from banks, post office, etc. (only for senior citizens) | Rs. 50,000 |

80GG | For rent paid when HRA is not received from employer | Least of : – Rent paid minus 10% of total income – Rs. 5000/- per month – 25% of total income |

80E | Education loan’s interest | Interest paid for a period of 8 years |

80D | Medical Insurance – Self, spouse and children | Rs. 25,000 |

– Parents more than 60 years old | Rs. 50,000 | |

24

| Home loan interest repayments

| Up to Rs. 2,00,000 |

Examples of Tax Planning

Here are a few examples of how tax planning can be effectively carried out:

- Choosing to opt out of the default tax regime i.e. new regime and paying tax as per the old regime to utilise the deductions which are not available under the new regime.

- Strategic replacement of assets to capitalize on depreciation provisions.

- Planned sale of capital assets based on holding period and specific deductions available for long-term assets such as Section 54, 54EC, etc.

- An individual taxpayer making a tax saver deposit of Rs. 1,00,000 in a nationalised bank to claim deduction under Section 80C.

How to save tax for different salary people:

How to Save Tax for Salary Above 7 Lakhs?

How To Save Tax For Salary Above 10 Lakhs?

How to Save Tax for Salary Above 12 Lakhs?

How To Save Tax For Salary Above 15 Lakhs?

How To Save Tax For Salary Above 20 Lakhs?

How To Save Tax For Salary Above 30 Lakhs?

How To Save Tax For Salary Above 50 Lakhs?

How to Save Tax For Salary Above 1 crore?

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption