|

Form CMP-08: Statement Filing Procedure, Due Date, Penalty and Other Pointers

In April 2019, a new tax payment process was laid down for composition dealers to simplify compliance for them. Form CMP-08 was introduced in April 2019 and was made applicable from FY 2019-2020 onwards. It replaces the erstwhile quarterly GSTR-4 filed by composition dealers.

Key Takeaways

- CMP-08 is the statement-cum-challan used by the businesses registered under the Composition scheme.

- It is a summary of quarterly sales that must be filed on or before the 18th of the month following the quarter.

- It is specially designed for small businesses to keep the tax paperwork simple and ease the return filing process.

- A late fee of Rs. 200/day (up to a maximum of Rs. 5000) is applicable for late filing of the return. If returns are not filed for 2 consecutive quarters, the system will not allow e-way bills to be generated.

What is Form CMP-08?

A composition dealer will use the Form CMP-08, which is a special statement-cum-challan to declare the details or summary of their self-assessed tax payable for a given quarter. It also acts as a challan for making payment of tax.

A composition dealer is a dealer who has been registered under the composition scheme laid down for both supply of goods and services. In addition to Form CMP-08, a composition dealer will also need to file his/her annual return via the revised format of Form GSTR-4 by the 30th of April following the end of a financial year.

Who should file CMP-08?

A taxpayer who has opted for the composition scheme has to file CMP-08 in order to deposit payments every quarter. There are two kinds of taxpayers registered using CMP-02 (Opt into Composition scheme):

- The supplier of goods being manufacturers, retailers having an annual aggregate turnover of up to Rs.1.5 crore (Rs.75 lakhs for special category States except for Jammu & Kashmir and Uttarakhand) in the previous financial year, except:

- Manufacturer of ice cream and other edible ice (whether or not containing cocoa), pan masala, or tobacco and manufactured tobacco substitutes.

- A person making inter-state supplies.

- A person supplying goods which are not taxable under GST Law.

- A casual taxable person or a non-resident taxable person.

- Businesses which supply goods through an e-commerce operator.

- The supplier of services who fulfil the conditions mentioned under the Notification Number 2/2019 Central Tax (Rate) dated 7 March 2019 having the aggregate annual turnover up to Rs.50 lakh in the previous financial year.

What is the due date to file the Form CMP-08?

Form CMP-08 must be filed on a quarterly basis, on or before the 18th of the month succeeding the quarter of any specific fiscal year. For example, the due date to file CMP-08 for the Jan-Mar 2026 quarter is 18th April 2026.

What is the penalty for not filing CMP-08 within the due date?

In case a taxpayer fails to furnish his/her statement on or before the due date, he or she will be liable to pay a late fee of Rs.200 per day for every day of delay. i.e. Rs.100 per day under CGST and Rs.100 per day under SGST. IGST Act prescribes an amount equal to the late fees for CGST and SGST Act i.e Rs.200 per day of delay. Late fee charges will be subject to a maximum of Rs.5,000 from the start of the due date to the actual filing date of the taxpayer.

Moreover, if CMP-08 of two consecutive quarters are not filed, then the e-way bill generation gets blocked. For unblocking, taxpayers need to apply to the jurisdictional tax official in Form GST EWB 05. They may also be required to file all pending forms for previous quarters.

How does a taxpayer fill CMP-08?

A taxpayer will need to fill in the following details:

Step 1- A taxpayer has to enter his/her GSTIN details. Have a look at the screenshot below to understand better:

Step 2– Once the GSTN number is entered, primary information such as the legal name and trade name will be auto-filled. The same statement will be updated for the ARN (Application reference number) and date of filing, once the payment is done. Take a look at the screenshot below for your reference:

Step 3– The third table of the form will have information/summary of the self-assessed tax liability. A taxpayer will need to provide details such as outward supplies on which tax is payable by him, including the inward supplies on which tax is payable on a reverse charge and cases of imports. Apart from this, the tax payable on these and the interest paid (if any) should be reported. Refer to the screenshot below for a better understanding:

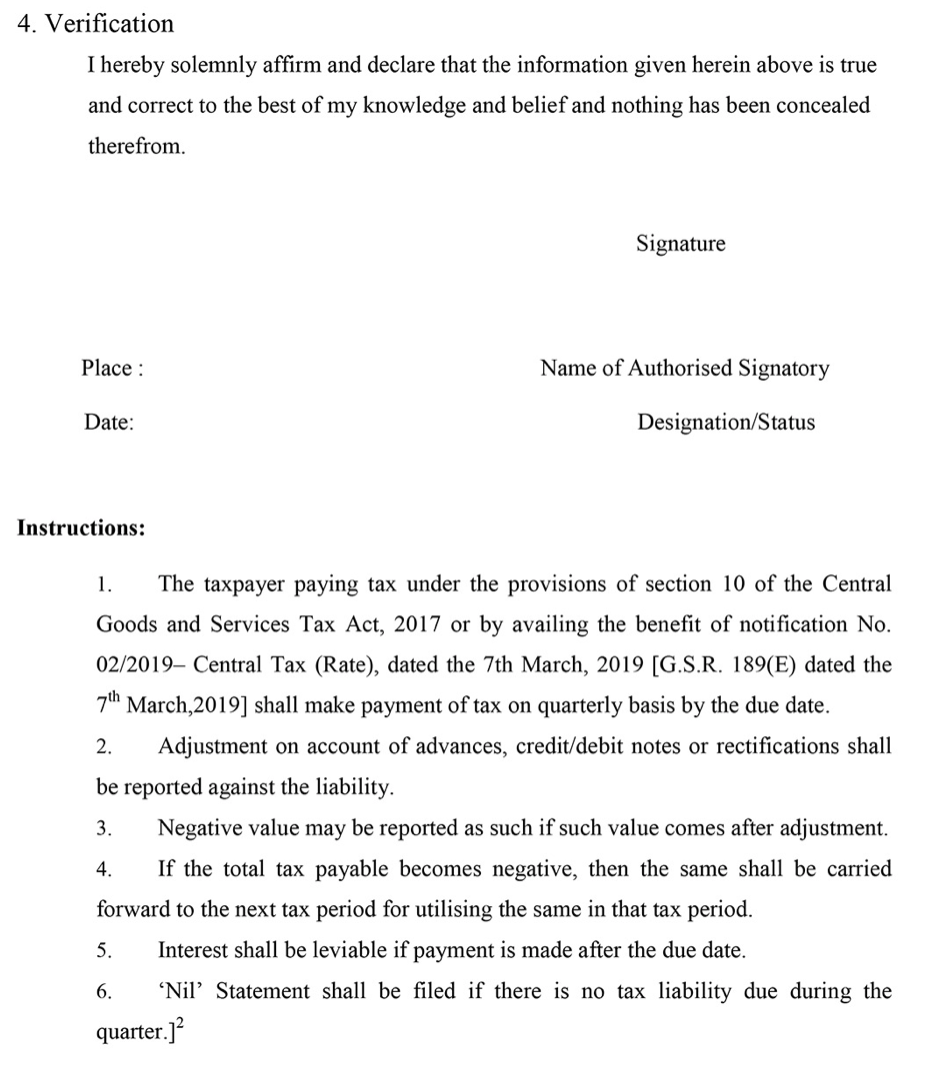

Step 4– In the final step, a taxpayer has to confirm that he/she has verified all the details that have been entered by signing the form. Here is a screenshot for your reference:

Important notes to a taxpayer:

- A taxpayer can file a ‘NIL’ return if his/her total tax liability is zero for a given quarter. A Nil CMP-08 can be filed via SMS.

- A taxpayer will be liable to pay interest as well as a penalty in case he/she misses the filing due date.

- Tax liabilities are inclusive of adjustment in relation to advances, credit notes, debit notes or, any rectifications.

For better understanding of the process, read our articles on ClearTax:

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption