|

GST Composition Scheme Transition

Composition scheme is a simple and easy scheme under GST for taxpayers. Small taxpayers can get rid of tedious GST formalities and pay GST at a fixed rate of turnover.

Latest Update

Attention GST registered taxpayers! 31st March 2018 is deadline to opt into Composition for FY 2018-19

For any GST registered taxpayer who want to opt for the Composition scheme for FY 2018-19; 31st March 2018 is the deadline to file the intimation in Form GST CMP-02 to opt into composition scheme for the FY 2018-19. Follow our Step-by-step Guide to file CMP-02 Also, furnish statement in form ITC-03 within 60 days of commencement of the FY 2018-19 to declare the ITC claim that has to be reversed on inputs/capital goods in stock, in semi-finished or in finished goods.

Need to introduce Composition Scheme under GST

Every tax administration aims towards timely recovery of taxes, filing of returns, simplified generation and maintenance of records, invoices and others documents. Such elements are often a challenge for small businesses.

To overcome this shortcoming a composition scheme was introduced under the respective State VAT Laws with conditions applied on eligibility for the scheme accordingly. The GST Law also contains an option for a registered taxable person having turnover less than the limit to pay tax at a lower rate respect to certain specified conditions

Know about Composition Scheme

Composition Scheme will be granted to a taxable person only if he registers all the registered taxable persons having the same PAN under the scheme. Here the motive is to bring all the business segments having same PAN under the scheme.

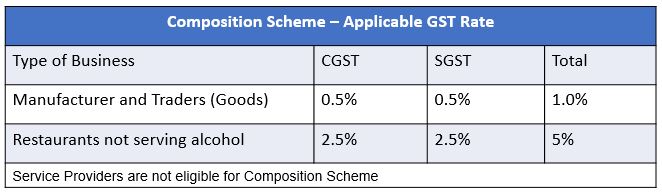

A registered tax payer, whose aggregate turnover does not exceed Rs seventy five lakh in the preceding financial year pay at a rate in lieu of central tax rate of not more than 2.5% for restaurant sector and 0.5% for manufacturers and other suppliers of turnover.

Composition Scheme will be a growth driver for small taxpayers who are carrying out intrastate transaction and does not involve into import-export of goods. As per notification dated 01.01.2018, turnover in case of traders has been defined as ‘ Turnover of taxable supplies of goods’.

GST Composition Scheme Transition Provision for Input Tax Credit on switch to and fro

As current regime provides for the composition scheme subject to certain conditions, GST Composition Scheme transition provision provides for allowance of credit of eligible duties and taxes on inputs held in stock subject to certain conditions

Switch from Normal tax payer to Composition Scheme holder

Switching from normal scheme to composition scheme, taxpayer shall be liable to pay an amount equal to the credit of input tax in respect of inputs held in stock on the day immediately preceding the date of such switch over. The balance of input tax credit after payment of such amount, if any lying in the credit ledger shall lapse.

Switch from Composite Scheme holder to Normal tax payer

Switching from composition scheme under current regime to normal tax payer under GST will attract transition provision and will be allowed credit of duties held in stocks as inputs or credit of value added Tax in respect of inputs and inputs contained in semi-finished or finished goods on the appointed date subject to the following conditions:

- Such inputs or goods are used or to be used in the making of taxable supplies

- Not being a composite scheme holder

- Being eligible to claim credit of taxes

- The inputs were not such that credit was not admissible under the earlier law due to being mentioned in any schedule or otherwise

- Being in possession of invoice or document evidencing payment of duties under earlier laws w.r.t. inputs held in stock and semi-finished or finished goods

- Such invoices and/ or documents were issued maximum twelve months before the appointed date.

The manner of calculation of amount of credit under GST for Composite scheme will be prescribed.

To know more about Composite Scheme under GST and its benefits or drawbacks, you may visit our site

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption