|

The Impact of Invoice Management System (IMS) on Credit Notes

The implementation of an Invoice Management System (IMS) can significantly influence the handling of credit notes under GST. To streamlining processes and enhancing compliance, leverage IMS for accurate reporting of credit notes in GST returns and ultimately ensure cash flows are least affected by it.

Workflow Before IMS: How was ITC Reversed on Credit Note

Prior to the establishment of an Invoice Management System, the process of managing credit notes involved cumbersome manual operations. Reversal of Input Tax Credit (ITC) related to credit notes was a complex task.

1. The seller issues a credit note to the buyer.

2. The buyer acknowledges the credit note.

3. Manual adjustment of ITC occurs, which could lead to errors.

The workflow often resulted in delays and inaccuracies. A flowchart illustrating these steps is shown below to help you understand the tedious nature of the process.

Legal Updates to Invoice Management System (IMS)

IMS although introduced in September 2024, wasn’t incorporated into the GST laws until the 55th GST Council meeting. Following extensive deliberation, the GST Council has put forward several crucial modifications at the 55th GST Council meeting, held in December 2024, to strengthen the regulatory framework.

CGST Section 38 and CGST Rule 60 are said to be amended to provide a legal framework for generating GSTR-2B based on IMS actions. Moreover, CGST Section 39(1) will also be amended to allow the GSTR-3B filing only after the availability of GSTR-2B on the GST portal.

To encourage handling of credit notes on IMS, amendments are recommended. The Council has suggested revisions to CGST Section 34(2) to introduce explicit provisions regarding input tax credit adjustments by both supplier and buyer.

When a supplier issues a credit note, recipients must now specifically reverse the corresponding input tax credit, enabling suppliers to reduce their output tax obligations accordingly. Next up, the introduction of a new CGST Rule 67B outlines specific protocols governing how suppliers can adjust their output tax liability in relation to their issued credit notes clarifying the adjustment mechanism.

Furthermore, effective October 2025 period onwards, a new section for "Import of Goods" has been introduced in IMS wherein the Bill of Entry (BoE) filed by the taxpayer for import of goods including import from SEZ, will be made available in the IMS for taking allowed action on individual BoE.

Effective October 2025 tax period, specified records can be kept pending for one tax period (one month for monthly taxpayers and one quarter for quarterly taxpayers). A new facility lets taxpayers declare the exact ITC availed and reverse only that amount, either partially or fully. If ITC was never claimed, no reversal is required.

Taxpayers can save optional remarks when rejecting or keeping records pending; these remarks will appear in GSTR-2B and supplier dashboards, improving communication and reconciliation.

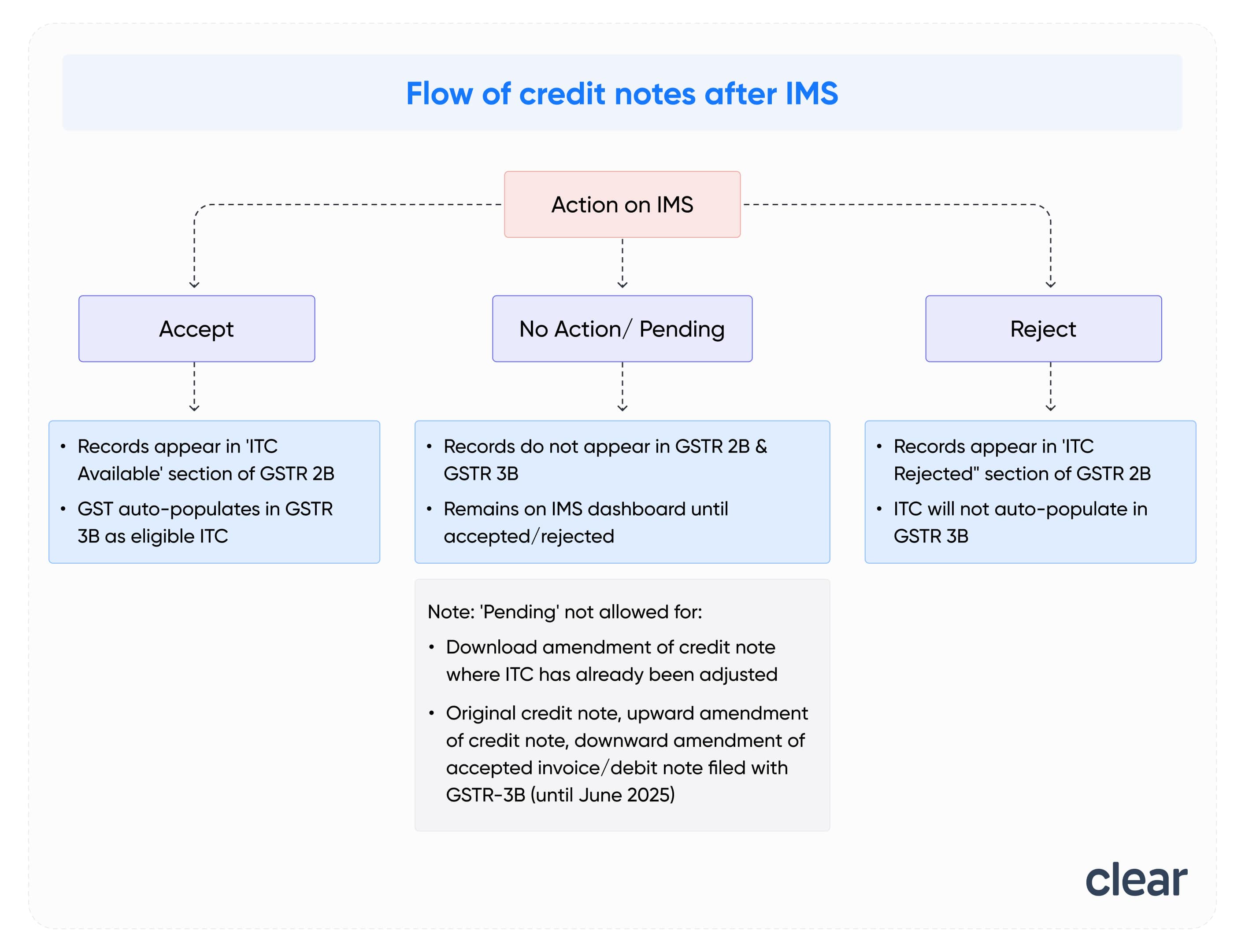

Workflow after IMS Implementation: Impact on Credit Note

With the implementation of IMS, the workflow for handling credit notes shifts dramatically.

Suppliers must take suitable action based on rejected credit notes. Failing to do this can lead to mismatches in GSTR-3B and notices due to under-payment of tax liability. Earlier, credit notes and other specified records could not be kept pending, recipients could either accept/reject credit notes. However, the latest GSTN advisory dated 23rd September 2025 has allowed to keep the following specified records pending only for one tax period, one month for monthly filers and one quarter for quarterly filers.

- Credit notes, or upward amendment of credit note

- Downward amendment of credit note where original credit note rejected

- Downward amendment of Invoice/debit note only where original Invoice already accepted and 3B has been filed

- ECO-Document downward amendment only where original accepted, and 3B has been filed

ITC reversal is automated and compliant with GST regulations. A flowchart illustrating these steps is shown below to help you understand the process.

Example of Handling Credit Note with IMS

Let's follow a transaction between Supplier "S" and Buyer "B".

- Supplier S issues a credit note of ₹50,000 (₹9,000 GST) on 1st January 2024 to Buyer B.

- Credit Note number: CN001

- Credit Note date: 1st Jan 2024

- GSTR-2B generated by Buyer B: 14th February 2024

- Reconciliation by B: 15th February 2024

- GSTR-3B filed by B on 20th February 2024

On 14th February 2024, when B sees his GSTR-2B, he finds that credit note CN001 was wrongly issued and does not belong to him. This error should not have an adverse effect on GSTR-3B of the buyer B.

Scenario 1: Without IMS (Previous Functionality)

- Credit Note Appears in GSTR-2B:

The credit note CN001 is reflected in Buyer B's GSTR-2B on 14th February 2024. - Impact on GSTR-3B:

The incorrect credit note automatically reduces Buyer B's Input Tax Credit (ITC) in Table 4A(5) of GSTR-3B. - Manual Reversal of ITC:

Buyer B notices the error during reconciliation on 15th February 2024. To fix this, B manually reverses the ITC in Table 4B(2) of GSTR-3B when filing his return on 20th February 2024.

Implications on Stakeholders:

- Supplier S: Reduces his GST liability by issuing an incorrect credit note.

- Buyer B: Incurs an additional administrative burden to manually reverse the ITC and risks compliance issues.

- GSTN (Government): The government has no visibility into the error at the invoice level, leading to a revenue loss. To address this, the government may issue notices to B, causing further complications.

Scenario 2: With IMS

- Real-Time Notification of Credit Note:

On 1st January 2024, B is notified via IMS about the issuance of credit note CN001 by S. - Immediate Rejection of Credit Note:

Buyer B might review the credit note on the same day (1st January 2024) and rejects it through IMS. This prevents the credit note from appearing in their GSTR-2B and impacting their GSTR-3B filing. - Impact on GSTR-3B:

Since the credit note is rejected at the source, there is:- No reduction in ITC in Table 4A(5) of GSTR-3B.

- No need for manual reversal in Table 4B(2).

Key Benefits of IMS for Streamlining Handling of Credit Notes

Adopting IMS for handling credit notes provides several business benefits, including:

- Better transparency and real-time data flow: Thanks to IMS, credit notes are becoming increasingly prominent in GST compliance reporting. IMS's integration into GSTR-2B ensures real-time visibility of adjustments related to invoices and input tax credit claims.

- Reduced scope for errors: IMS defines a standardised process for the flow of documents from suppliers' GSTR-1 into recipients' GSTR-2 B, including credit notes. The data between the two returns are better aligned and cross-verified to highlight any errors in taxable or tax values. In turn, the GSTR-3B is cleaner. Accordingly, the risk of penalties due to human errors is drastically reduced.

- Seamless GST Compliance: Automated systems ensure that ITC reversals and credit note adjustments follow GST regulations, helping businesses avoid penalties.

Specific Use Cases of IMS Implication for Credit Notes

- Retail Sector: In retail, when a customer returns a product, the IMS facility on the GST portal helps taxpayers track and manage credit notes issued, ensuring proper GST input tax credit reconciliation.

- Service Industry: For service-based industries, when adjustments are needed in billed amounts due to service modifications, the IMS facility on the GST portal helps monitor and reconcile the credit notes with supplier declarations.

Challenges and Considerations

While the benefits are clear, there are challenges that businesses must address:

- Operational Adjustments: While using the IMS facility on the GST portal is beneficial, businesses must establish internal processes to regularly monitor and take appropriate actions (accept/reject) on their IMS dashboard for proper ITC management.

- Training and Adaptation: Staff may require training to effectively utilise the new system.

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption