|

What is Input Tax Credit under GST & How to claim it?

|

A significant change that GST introduced was the mechanism of input tax credit under GST.

- For beginners – Don’t worry if you have never heard of ‘input tax credit’ before. We’ll start from scratch.

- For businesses – If you are a business, you may have already heard of VAT input credit, and you will soon know how it differs from GST input tax credit.

Latest Updates

1st February 2022

Budget 2022 updates-

1. ITC cannot be claimed if it is restricted in GSTR-2B available under Section 38.

2. Time limit to claim ITC on invoices or debit notes of a financial year is revised to earlier of two dates. Firstly, 30th November of the following year or secondly, the date of filing annual returns.

3. Section 38 is completely revamped as ‘Communication of details of inward supplies and input tax credit’ in line with the Form GSTR-2B. It lays down the manner, time, conditions and restrictions for ITC claims and has removed the two-way communication process in GST return filing on the suspended return in Form GSTR-2. It also states that taxpayers will be provided information of eligible and ineligible ITC for claims.

4. Section 41 is also revamped to remove the references to provisional ITC claims and prescribes self-assessed ITC claims with conditions.

5. Sections 42, 43 and 43A on provisional ITC claim process, matching and reversal are eliminated.29th December 2021

CGST Rule 36(4) is amended to remove 5% additional ITC over and above ITC appearing in GSTR-2B. From 1st January 2022, businesses can avail ITC only if it is reported by the supplier in GSTR-1/ IFF and it appears in their GSTR-2B.21st December 2021

From 1st January 2022, ITC claims will be allowed only if it appears in GSTR-2B. So, the taxpayers can no longer claim 5% provisional ITC under the CGST Rule 36(4) and ensure every ITC value claimed was reflected in GSTR-2B.

What is input tax credit?

Input tax credit means at the time of paying tax on output, you can reduce the tax you have already paid on inputs.

Suppose, you are a manufacturer –

- Tax payable on output (final product) is Rs 450

- Tax paid on input (purchases) is Rs 300

- You can claim input tax credit of Rs 300 and you need to pay only Rs 150.

Input tax credit in GST

Input tax credit mechanism is available to you when you are covered under the GST Act. Which means if you are a manufacturer, supplier, agent, e-commerce operator, aggregator or any of the persons mentioned, registered under GST, you are eligible to claim input tax credit for tax paid by you on your purchases.

How to claim input tax credit under GST?

To claim input tax credit under GST –

- You must have a tax invoice(of purchase) or debit note issued by registered dealer

- You should have received the goods/services

Note: Where goods are received in lots/instalments, credit will be available against the tax invoice upon receipt of last lot or installment. Note: Where recipient does not pay the value of service or tax thereon within 3 months of issue of invoice and he has already availed input tax credit based on the invoice, the said credit will be added to his output tax liability along with interest.

- The tax charged on your purchases has been deposited/paid to the government by the supplier in cash or via claiming input tax credit

- Supplier has filed GST returns

- Supplier has uploaded the invoice in their GSTR-1 and it appears in GSTR-2B of the recipient or buyer. Know more.

Possibly the most path-breaking reform of GST is that input tax credit is ONLY allowed if your supplier has deposited the tax he collected from you. So every input tax credit you are claiming shall be matched and validated before you can claim it. Therefore, to allow you to claim input tax credit on Purchases all your suppliers must be GST compliant as well.

There’s more you should know about input tax credit –

- It is possible to have unclaimed input tax credit. Due to tax on purchases being higher than tax on sale. In such a case, you are allowed to carry forward or claim a refund.

If tax on inputs > tax on output –> carry forward input tax or claim refund If tax on output > tax on inputs –> pay balance No interest is paid on input tax balance by the government

- Input tax credit cannot be taken on purchase invoices which are more than one year old only in cases of special circumstances under Section 18(1). The period is calculated from the date of the tax invoice.

- Since GST is charged on both goods and services, input tax credit can be availed on both goods and services (except those which are on the exempted/negative list).

- Input tax credit is allowed on capital goods.

- Input tax is not allowed for goods and services for personal use.

- No input tax credit shall be allowed after GST return has been filed for September following the end of the financial year to which such invoice pertains or filing of relevant annual return, whichever is earlier.

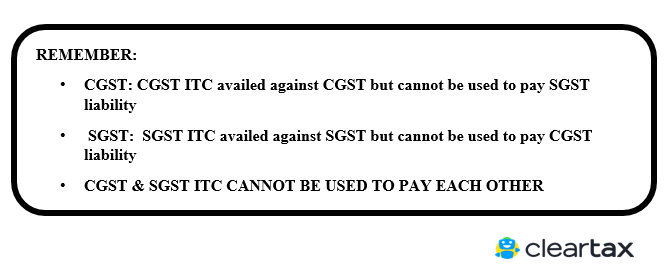

Type of taxes under GST

All existing taxes such as VAT, CST, Excise Duty, Service Tax, Entertainment Tax shall go away and GST will replace them.

There are 3 types of taxes under GST

- State GST – SGST

- Centre GST – CGST

- Integrated GST – IGST

Now let’s understand how Input Tax Credit works under GST

Suppose there is a seller Mr A and he sells his goods to Mr B. Here Mr B i.e the buyer will be eligible to claim the credit on purchases based on the invoices. Let’s understand how:

Step 1: Mr A will upload the details of all tax invoices issued in GSTR 1.

Step 2. The details with respect to sales to Mr B will auto-populate/ get reflected in GSTR 2A or GSTR-2B, the same data will be pulled when Mr B will file GSTR 2 (i.e details of inward supply).

Step 3: Mr B will then accept the details that the purchase has been made and reported by the seller correctly and subsequently the tax on purchases will be credited to ‘Electronic Credit Ledger’ of Mr B and he can adjust it against future output tax liability and get the refund.

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption