|

ClearTax GST Software for e-Commerce Sellers

E-Commerce Sellers can file their GST Returns with ease using ClearTax GST Software.

ClearTax GST Software allows sellers to import Reports generated from e-commerce websites thus making GST Return filing an easy task.

All you need to do is upload all the Sales report generated on the e-commerce websites, make some changes and upload the Excel file on ClearTax

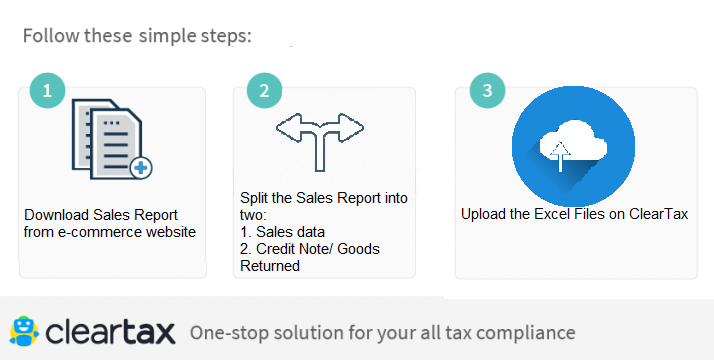

An E-commerce seller has to follow a simple 3 step process to file GSTR-1 on ClearTax:

Step 1: Download the Sales Report from the e-commerce website

All sellers on e-commerce platforms can generate a monthly Sales Report from their login.

Amazon Sellers can download Merchant Tax Report from their login.

Similarly, Flipkart and Paytm and other e-commerce Sellers can also download the Sales Report from their sellers login.

Step 2: Split the Sales Report

The downloaded Sales Report has to be split into 2 reports:

- One Excel containing details of all sales. You can do this by filtering your excel (stepwise detailed explanation provided in the PPT below).

- Another Excel containing all the Credit Notes (goods returned).

Step 3: Upload the Excel on ClearTax

All you need to do now is upload the Excels on ClearTax GST Software. Amazon, Flipkart, and PayTM Sellers can choose the Template based on the type of Excel being uploaded.

If you are a seller on any other e-commerce platform you can use our ‘Field Mapper’ to upload your Sales Reports, Map the fields and save it as a template.

Once the Excel files have been uploaded on ClearTax GST Software all you need to do is review and upload the data to GST Portal/ GSTN.

Below are the detailed guides that can help sellers download sales report and upload the Excel to ClearTax GST Software.

Amazon Sellers

Flipkart Sellers

PayTM Sellers

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption