|

Is it Possible to Revise GSTR-3B ?

|

It is not possible to revise GSTR-3B once it is filed.

However, the Government has allowed 'Reset GSTR 3B' through which the status of 'Submitted' will be changed to 'Yet to be Filed', and all the details filled in the return will be available for editing. All the entries posted in the Electronic Liability Register will be deleted, and the ITC of this return integrated with the Electronic Credit Ledger will be reversed. This option can be availed only once.

Let’s see how it is to be done:

Steps to Revise GSTR-3B

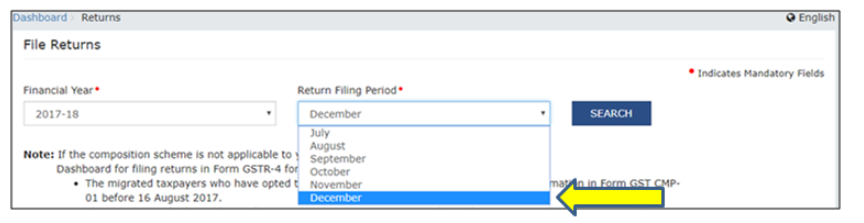

Step 1: Log in to the GST portal and go to the RETURN DASHBOARD

Step 2: Select the year and the month for which you want to reset GSTR-3B

Step 3: Click on Prepare Online

Step 4: Since you have already submitted the return, the option to 'Reset GSTR 3B' will be activated

Step 5: Click on ‘Reset GSTR 3B’

Step 6: Click on ‘Yes’ and ‘OK

Now that you have reset the return and status changed to ‘Yet to be filed’ make changes to return and submit again. Note: Details provided in the return will not be changed only status changes.

Features Of Reset GSTR-3B Option

- This option to correct /alter data can be used only before filing the GSTR-3B. Hence, once filed, GSTR-3B cannot be revised.

- The details provided in the return will not be changed; only the status will be changed.

- Remember, you can reset the return only once.

Other options / checks

- You may click 'PREVIEW' to view the entire form before submitting the return.

After reviewing, if you find errors or need to make changes, you can go to the tiles and edit the figures.

- On clicking 'INITIATE FILING', a tax summary screen pops up. Check the figures and then proceed.

Earlier scenario

Invoice-level details need not be provided in the GSTR-3B. Thus, this leaves scope for errors while computing output tax liability and Input tax credit (ITC), leading to incorrect tax paid. Any incorrect computation of tax liability would add to the taxpayer's additional compliance burden.

There was no option for making changes or corrections in the GSTR-3B once you clicked the 'SUBMIT' button. You had to proceed to file using the DSC or EVC directly. The taxpayers were, therefore, inconvenienced if they committed any errors while submitting GSTR details in the values or tax figures or omitted to furnish some information in return.

The Government has now provided a breather to taxpayers by introducing the 'RESET GSTR-3B' feature, which allows them to make a one-time correction in the tax figures posted to the Electronic Liability Ledger before making payment of tax in GSTR-3B. Therefore, these options give the taxpayer a chance to be cautioned of any errors apparent on record and make corrections.

Note: Once the taxpayer submits the return, the value of Outward supplies cannot be changed. The value of outward supplies becomes locked, and any corrections or changes intended to be made must be made while filing the GSTR-1.

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption