|

Understanding Section 31 of the CGST Act: Tax Invoices under GST

Section 31 of the CGST Act is important because tax invoices aren’t just about ticking compliance boxes. They are about ensuring your operations run smoothly—be it claiming Input Tax Credit (ITC) or maintaining transparency with your customers or clients.

Below is the detailed look of this section—without jargon, without stress. Just practical, real-world advice for Indian businesses.

What Exactly Is Section 31 of the CGST Act?

Think of Section 31 as your guidebook for issuing tax invoices. It answers essential questions like:

- When should an invoice be issued?

- What details need to go in it?

- What happens if you don’t issue an invoice?

For example: Sajini runs a boutique in Jaipur. Last year, she supplied custom lehengas to a destination wedding planner. She issued an incomplete invoice (she forgot to include the Place of Supply). It delayed the buyer’s Input Tax Credit (ITC) claims and her own payment by over two months.

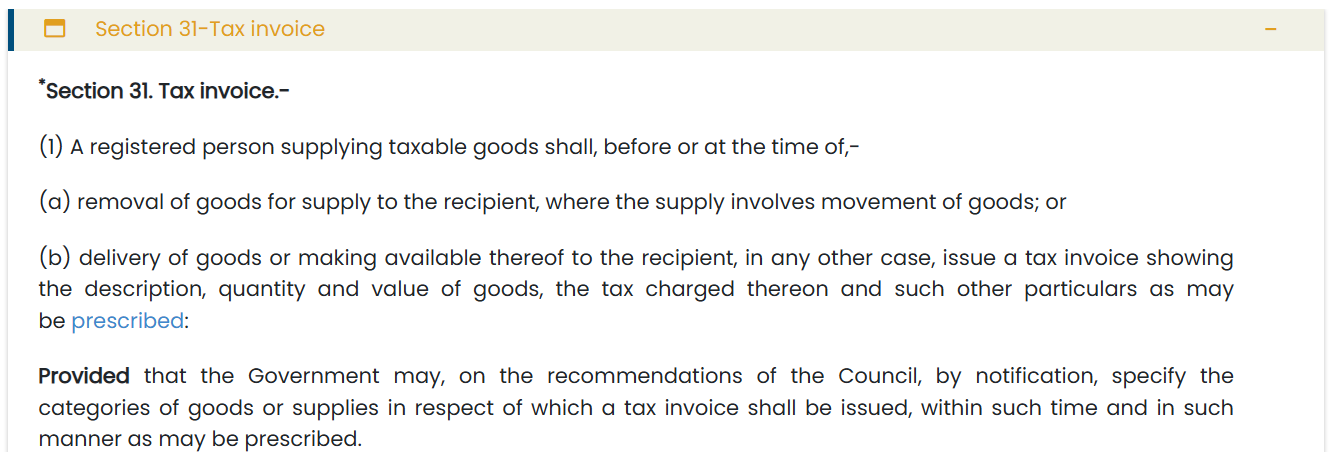

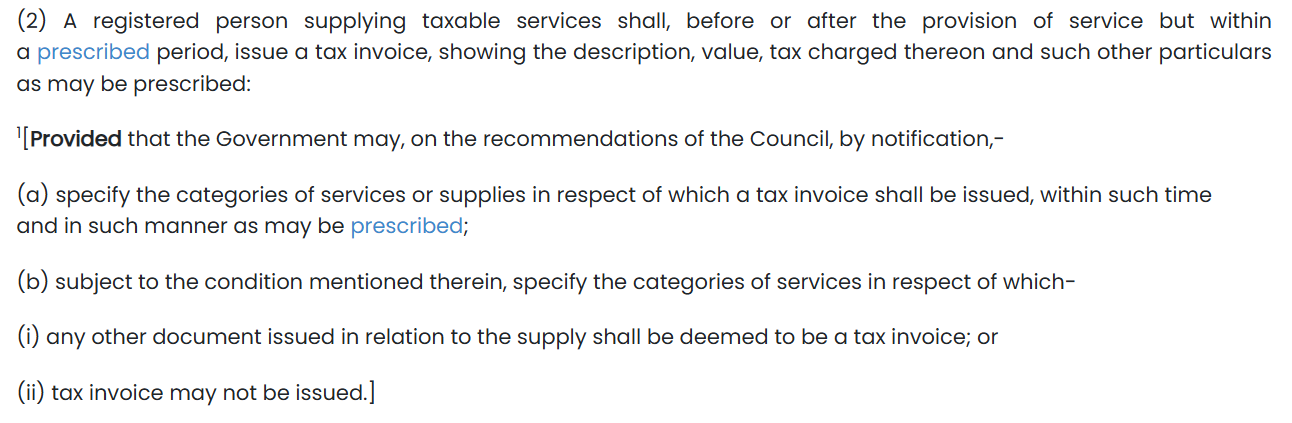

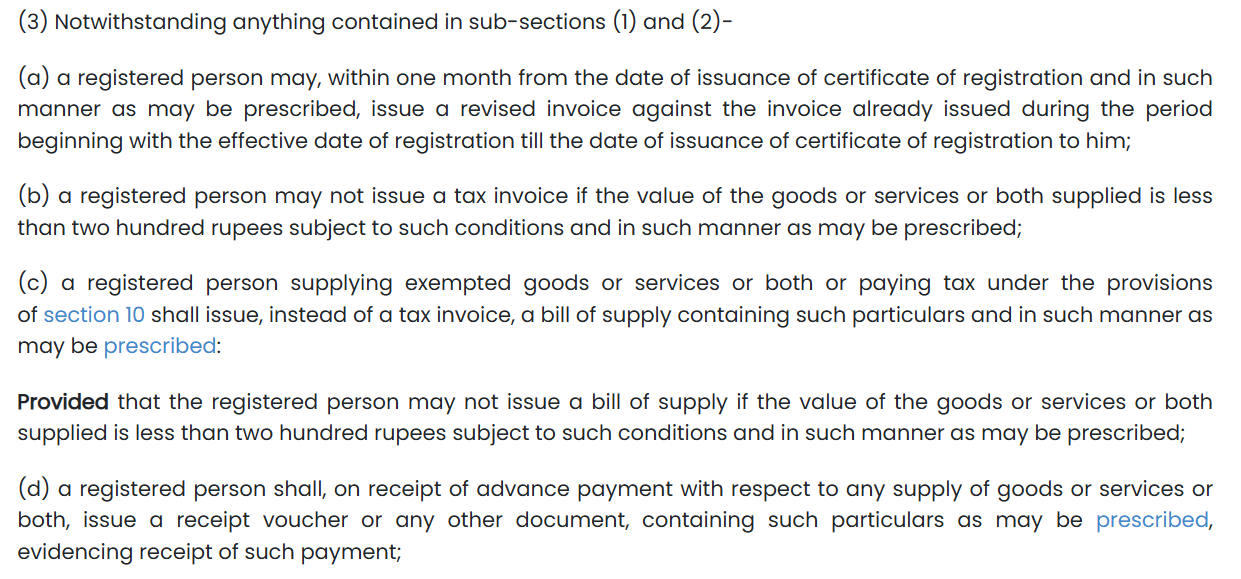

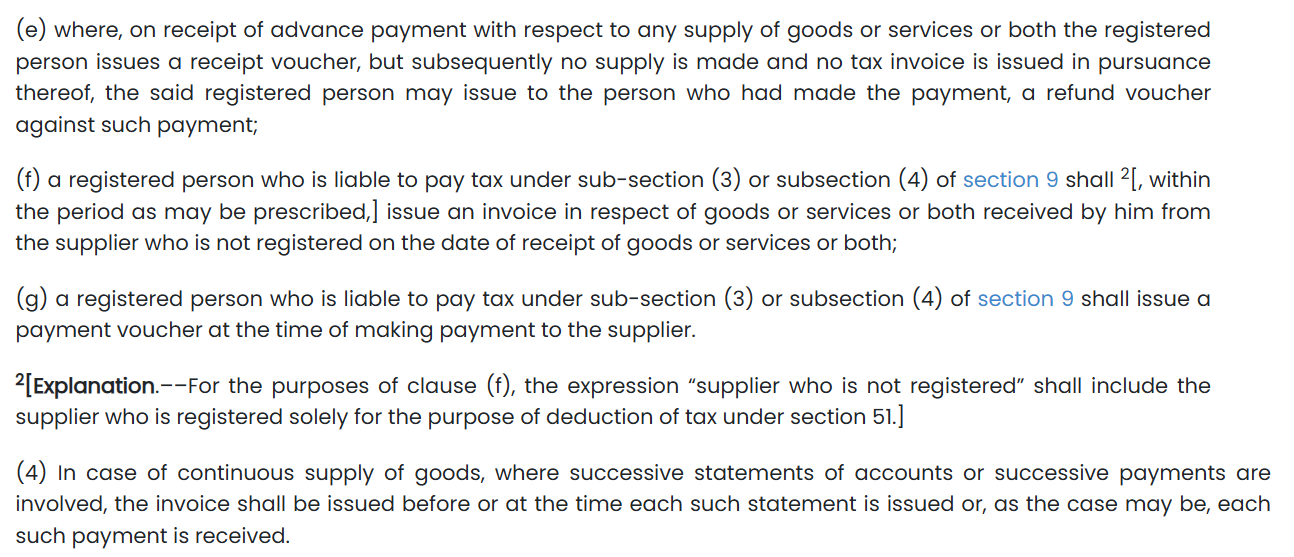

Below is an excerpt from the CGST Act Section 31-

When to Issue a Tax Invoice?

The timeline for issuing invoices depends on the nature of the transaction:

1. For Goods:

- With Physical Movement: Issue the invoice before or during delivery.

- Without Movement: Issue the invoice when goods are made available.

Example: A wholesale supplier in Mumbai dispatching 500 kg of wheat must include the invoice with the shipment.

2. For Services:

You get a little leeway—30 days from completing the service. Example: Say you’re a wedding photographer in Kerala. After delivering the final edited album, you have up to a month to send the invoice.

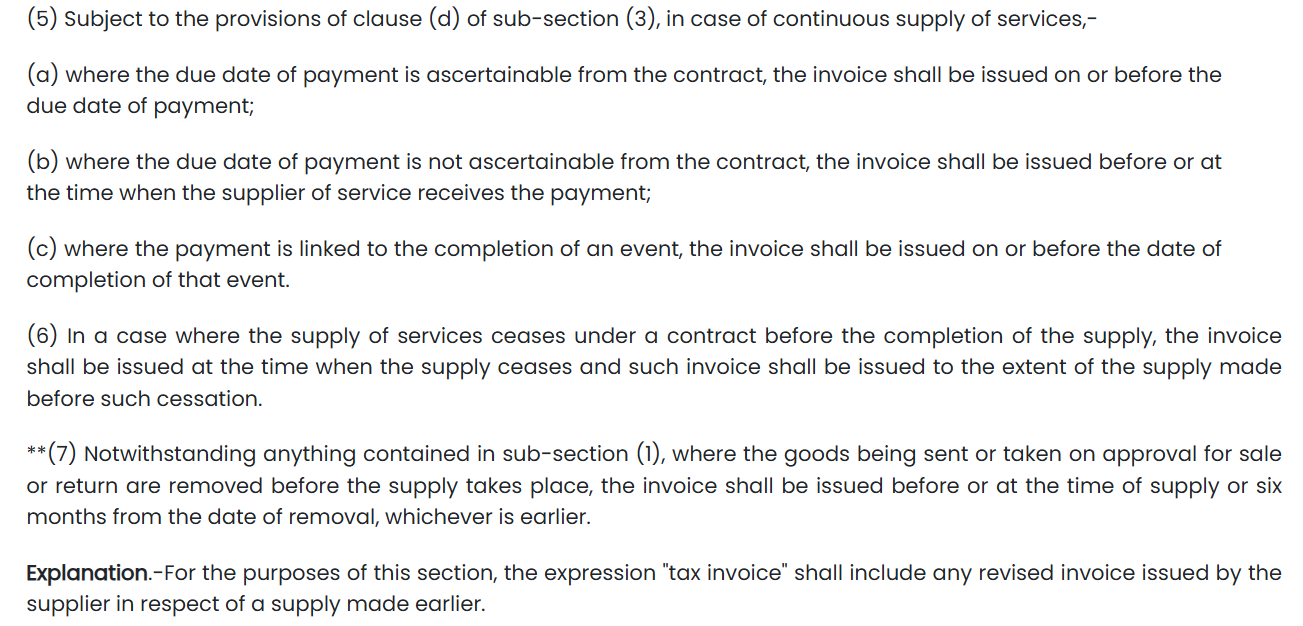

3. For Continuous Supply (Goods or Services):

Follow the terms outlined in the contract.

Example: A vendor supplying raw materials weekly to a construction firm issues invoices biweekly as per their agreement.

What should a GST-compliant Invoice include?

The invoice must include the following details:

- Seller’s Details: Name, address, GSTIN.

- Buyer’s Details: Name, address, GSTIN (if registered).

- Unique Invoice Number: Sequential and unique.

- Date of Issue: Non-negotiable.

- Description of Goods/Services: Quantity, unit price, and total value.

- Tax Breakdown: Separate CGST, SGST, and IGST amounts.

- Place of Supply: Determines applicable taxes.

- Signature: Physical or digital.

Deadlines for Issuing Tax Invoices

Here’s a quick reference for deadlines:

Type of Supply | Deadline |

Goods with physical movement | Before or at the time of dispatch |

Goods without movement | When made available |

Continuous supply of goods | As per contract terms |

Services | Within 30 days of completion |

Continuous supply of services | As per the billing cycle in the agreement |

Meeting these timelines ensures smooth operations and reduces the risk of penalties.

Breaking Down Section 31 Clause by Clause

Let’s make this straightforward:

- 31(1): General rules for issuing tax invoices.

- 31(2): Guidelines specific to goods transactions.

- 31(3): Rules for supplementary invoices, debit notes, and credit notes.

- 31(4): Special requirements for interstate supplies.

- 31(5): Conditions where a “bill of supply” can replace a tax invoice.

- 31(6): Documentation rules for exports, including export invoices.

Understanding these clauses can help you tailor your invoicing practices based on your business type.

Are There Exemptions from Issuing Invoices?

Yes, not every transaction requires a tax invoice. Here are some exceptions:

- Low-Value Transactions: If the total is under ₹200, a simplified bill works unless the buyer asks for a full invoice.

- Exempt Goods/Services: For example, fresh fruits or educational services don’t attract GST, but records are still important.

- Composition Scheme Taxpayers: Can issue a bill of supply instead.

Consequences of Non-Complaince

Ignoring Section 31 can land you in trouble.

- Monetary Penalties: ₹500 per incorrect or missed invoice may not seem like much, but it adds up.

- Delayed ITC for Buyers: If your invoice is incorrect or late, your clients might lose their ITC eligibility. This could strain your business relationships.

- Audits and Scrutiny: Persistent non-compliance increases your chances of being audited.

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption