|

How to View GSTR 2A on GST Portal

GSTR 2A is a return containing details of all the inward supplies, TDS and TCS. GSTR 2A is auto-populated based on the following –

- A supplier saves details or submits or files his GSTR-1 & GSTR-5 for all the B2B transaction details

- ITC distributed by ISD while submitting GSTR-6

- TDS and TCS details based on GSTR-7 & GSTR-8 filed by dealers who deducted TDS/ TCS.

- Details of the import of goods from overseas, on a bill of entry, as updated on the ICEGATE Portal of Indian Customs.

It is a read-only return and cannot be filed on the GST portal. Instead, the taxpayer can only view or download the same for every month in a financial year.

Recent Updates on GSTR-2A

Budget 2025

1st February 2025

1. Amendments in Section 34 of the CGST Act, 2017: The FM amended the Proviso to sub-section (2) to explicitly provide for the requirement of reversal of corresponding ITC in respect of a credit-note. It means if the supplier issues a credit note to reduce their tax liability, the recipient must reverse the corresponding ITC, if already availed.2. Amendments in Section 38 of the CGST Act, 2017: Section 38(1) is being amended to omit the expression "auto-generated" indicating that the ITC statement i.e. GSTR-2B may no longer be entirely system-generated. Businesses may now need to validate and reconcile invoices and ITC through the Invoice Management System (IMS) rather than relying solely on system-generated data. Also, a new clause (c) to sec 38(2) is added, allowing the government to specify additional details in the ITC statement through rules.

Should I refer to GSTR-2A or GSTR-2B?

GSTR-2A is a dynamic return. In other words, the details may get changed whenever the supplier revises invoice details through amendments in the subsequent tax periods.

Therefore, since August 2020, the CBIC has introduced the GSTR-2B return which is a monthly return auto-drafted for the inward supplies and ITC and is static in nature. It means the contents of GSTR-2B for any month remains unchanged. Accordingly, the taxpayers must refer to GSTR-2B for ITC reporting in GSTR-3B in every tax period (monthly/quarterly) instead of relying on GSTR-2A.

On the other hand, GSTR-2A holds importance in reconciling or matching ITC details across tax periods while finalising the accounts of a financial year.

However, there are certain details present only in GSTR-2A and not in GSTR-2B that may have to be referred to such as the TCS and TDS credit received.

How to view GSTR 2A?

Here is a step by step guide on how to file GSTR 2A –

Step 1 – Login to GST Portal.

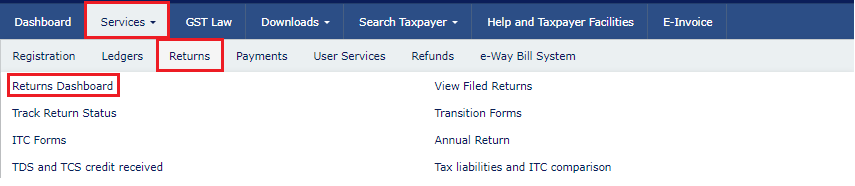

Step 2 – Go to Services. In the drop-down click on Returns > Returns Dashboard.

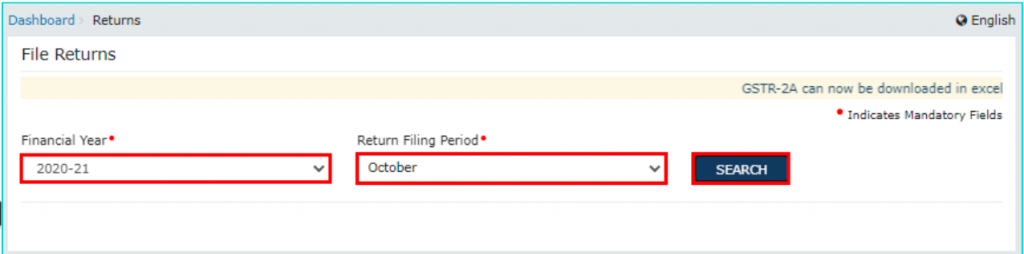

Step 3 – Select the Financial Year and the Return Filing Period from the drop-down. Click on the ‘Search’ button.

Step 4 – Click on the ‘View’ button in the tile GSTR-2A.

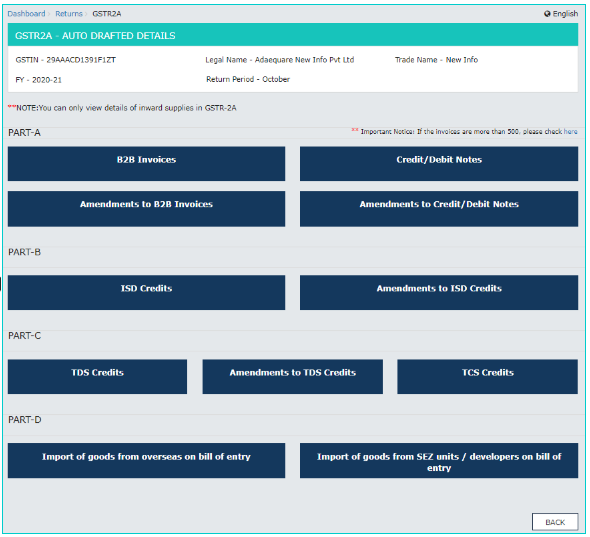

Step 5 – The GSTR2A – auto drafted details is displayed.

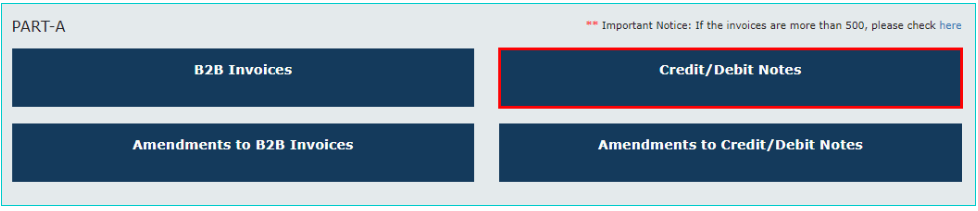

Step 6 – Under Part A, click on B2B Invoices. The details on this page will be auto-populated based on the returns filed by the suppliers.

Click on GSTIN to view the invoices uploaded by each supplier.

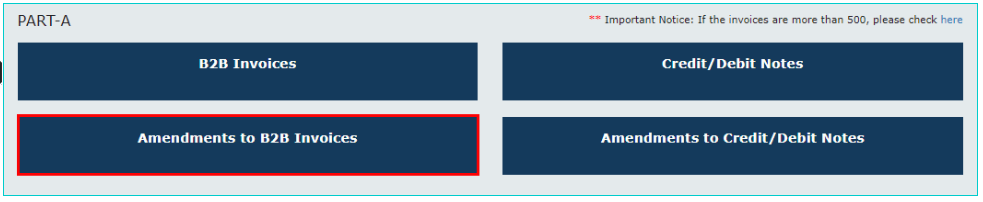

Step 7 – Under Part A – Amendments to B2B Invoices displays the invoices that have been amended by the suppliers in their GSTR 1 or GSTR 5.

Step 8 – Next is Credit/Debit Notes under Part A. This covers all the credit note or debit note added by the suppliers. Click on the tile to view GSTIN-wise details of debit/credit note.

Click on the GSTIN to view the debit/credit notes in further detail.

Step 9 – Amendments to Credit/Debit Notes is the next tile under Part A. This contains details of all the amendments made by the suppliers to the credit/debit notes. Click on the tile to see supplier wise details.

Step 10 – ISD Credits tile in Part B is the next tile. The details inside this tile are auto-populated based on the GSTR 6 filed by an Input Service Distributor. Likewise, make use of the amendment to ISD credits for any revisions.

Step 11 – TDS Credits tile under Part C of GSTR 2A will get auto-populated based on GSTR 7 filed by the dealers who deduct TDS.

Step 12 – Part C TCS Credits is the next tile. This contains details of TCS collected by dealers. The details in this section are auto-populated based on GSTR 8 filed by the TCS collector.

Step 13 – Part D will contain the details of the import of goods from overseas on bill of entry.

How to download GSTR 2A?

The taxpayer has to download the GSTR-2A if the number of invoices is more than 500 in number. One must have the GST offline tool installed on the system to be able to use this file. Here is a step-by-step guide to download the GSTR-2A.

Step 1 – Click on the ‘Download’ button on the GSTR-2A tile.

Step 2 – Click on the ‘Generate JSON file to download’ or ‘Generate an excel file to download’ button to generate data in the JSON or excel formatted file. The generated JSON file must be opened in Returns Offline Tool, available on the GST portal for download.

Step 3 – Click on the hyperlink “Click here to download JSON -File 1” once it appears.

For further understanding about GSTR-2A, read our articles:

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption